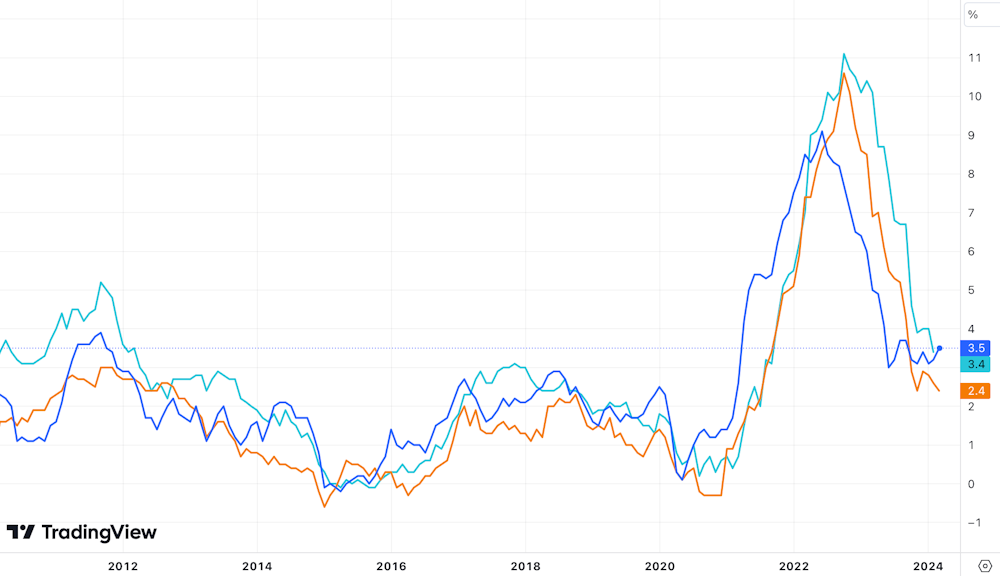

The 0.4% rise in US consumer prices in March didn’t look like headline news. It was the same as the February increase, and the year-on-year rise of 3.5% is still sharply down from 5% a year ago.

All the same, this modest uptick in annual inflation from 3.2% in February has cast doubt on whether the US central bank, the Federal Reserve, can afford to cut headline interest rates as fast as it has been signalling. To further complicate matters, a gap has opened up between the US inflation rate and that of other regions, notably the EU.

US inflation vs EU and UK

Trading View

Financial markets’ instant reaction was bearish. They dumped stocks while buying EU government bonds, in expectation of a boost from the European Central Bank cutting its rates sooner. They also bought the US dollar, anticipating it will strengthen when European rates come down. But how is this likely to play out?

Can they all be right?

The US economy has returned to steady expansion after the COVID-19 pandemic disruption of 2020-22, while Europe is struggling to achieve any growth. This helps to explain the difference in the inflation figures.

The strength of the US economy was already putting pressure on the Fed to cut less quickly. A higher interest rate helps to stop strong demand straining supply chains and making prices rise too fast. The quickening of consumer-price inflation gives the Fed an added incentive to be hawkish on rates – to convince businesses and households that it will keep monetary conditions tight until inflation falls back to the 2% target.

The interest rates on advance purchases of US debt (the “Fed futures” market) show that a majority of traders now expect the Fed will not drop its interest rate from the current level (of 5.25% to 5.5%) to below 5% until December. A week ago, most thought this would have happened by September.

The trouble is that an extended period of higher rates could be very damaging because there’s so much debt in the system. In particular, last year’s wobbles in the US banking sector, and wider concerns about institutional investors exposed to a slump in commercial real estate, are strong incentives to reduce credit costs before too long.

Consequently, few believe the US headline interest rate will still be at present levels a year from now. Yet the longer that inflation endures, the more the pressure to delay further rate cuts. Most Americans now believe inflation will stay around 3% for the next year, an expectation echoed in markets for assets viewed as protecting against inflation (such as gold and cryptocurrencies).

Election-year inflation dangers

An especially fraught presidential election race also limits the Fed’s manoeuvring room. The White House has pitched its 2024-25 federal budget as helping to subdue inflation, by lowering working families’ living costs and forcing companies to pass-on cost savings.

But while Joe Biden aims to spend US$7.3 trillion (£5.8 trillion) in pursuit of his plans, congressional opponents are likely to block many of the tax increases intended to pay for them.

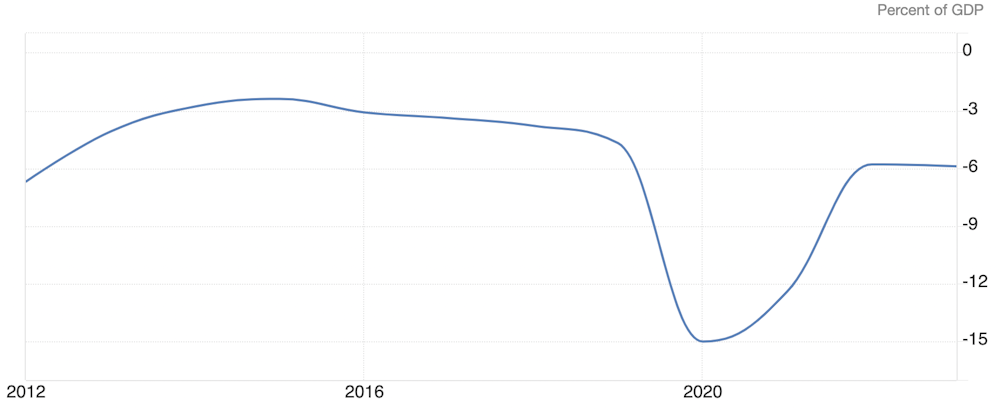

That’s likely to mean a continued widening of the US federal deficit, injecting more demand and keeping up inflationary pressure. That pressure could be worsened by the punitive tariffs that Republicans want to impose on cheap imports, to which many Democrats are sympathetic. An increasingly bipartisan push for tighter border controls would also raise US inflation risk, by stemming the inflow of cheap labour that has kept unskilled wages down.

US federal deficit

Trading Economics

The case for cutting anyway

Despite these caveats, financial markets could well still be proved wrong about the speed of US rate cuts. Besides the private-sector debt concerns, one additional potential justification for cutting sooner actually relates to inflation. While central banks respect the conventional wisdom that higher interest rates reduce inflation, they cannot disregard evidence that the effect may be reversed if rates are kept high for too long.

When businesses expect interest rates to stay high, they raise prices to compensate, especially if heavier debt repayments spur employees to ask for more pay. Notably, the rising cost of mortgages in the US was one of the factors in March’s inflation surprise. The Fed can best tackle this by maintaining the assurance of lower interest rates, so that accommodation costs can fall.

Meanwhile, China is grappling with falling prices, which can do even worse damage than an inflation overshoot. There is still a possibility of China trying to escape this situation by flooding the world with cheap goods, and energy costs falling sharply when the Russia-Ukraine war ends. This would leave central banks in Europe and America concerned to stop their inflation falling too far, by cutting rates faster than the market currently expects.

EPA

The Fed must finally factor in the global downside of holding firm while other central banks’ interest rates fall. This would deal a double blow to the many countries, and non-US companies, that have borrowed in US dollars to finance their expansion plans. They would pay relatively more on their dollar debt, while their local currency revenues would buy fewer dollars, since the dollar strengthens as US interest rates move relatively higher.

The dollar’s global reach means that if the Fed doesn’t let headline rates fall, it could exacerbate a global slowdown. That would rebound against American producers, especially those now reliant on Europe, Latin America and Asia as major export markets. So when the ECB cuts rates, the Fed can be still expected to follow, even if it means US inflation remaining above target into 2025. This could mean another boost to stock prices, fresh incentives to borrow more money, and greater instability for the years ahead.

{kind=link}