LONDON, Nov 30 (Reuters) – A big disconnect between financial markets and central banks has just got deeper, with traders ramping up their bets on interest rate cuts in the United States and Europe as evidence grows that inflationary pressures are fast abating.

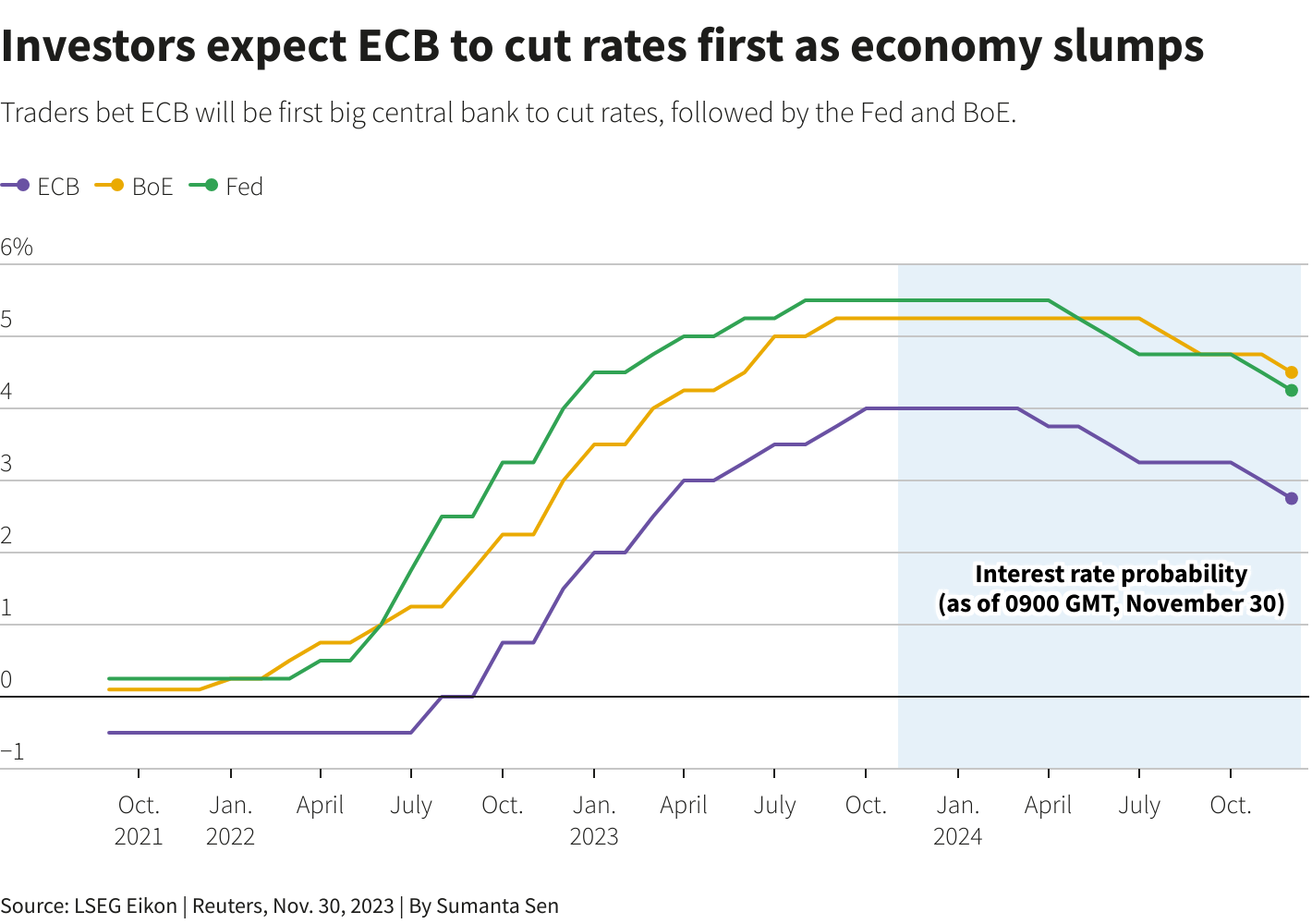

Money markets are now pricing in over 100 basis points apiece of rate cuts from the U.S. Federal Reserve and European Central Bank next year, and have this week shifted the expected timing of their first moves firmly forward into the first half of 2024.

It’s not hard to see why traders are ready to leave behind the most aggressive rate-hiking cycle in decades.

Euro zone inflation tumbled far more than expected in November, data on Thursday showed, a challenge to the ECB’s narrative of stubborn price growth.

In the United States, the Fed’s preferred inflation measure, the core PCE price index, eased in October.

For much of this year central banks have successfully pushed back against rate cut bets.

But this week’s price action suggests that task could get harder as investors question whether the mantra of higher rates for longer can hold if inflation keeps easing quickly.

“Is the Fed going to pivot from their hawkish statements that they are adamantly focused on inflation and need to kill it?” said Nate Thooft, global CIO for the multi-asset solutions team for Manulife Investment Management.

“I believe the Fed will act rationally and begin to cut rates by the end of next year, but we can’t rule out the scenario that the Fed is not going to cut rates and just let the ramifications of recession do what they do.”

SHIFT NEARING

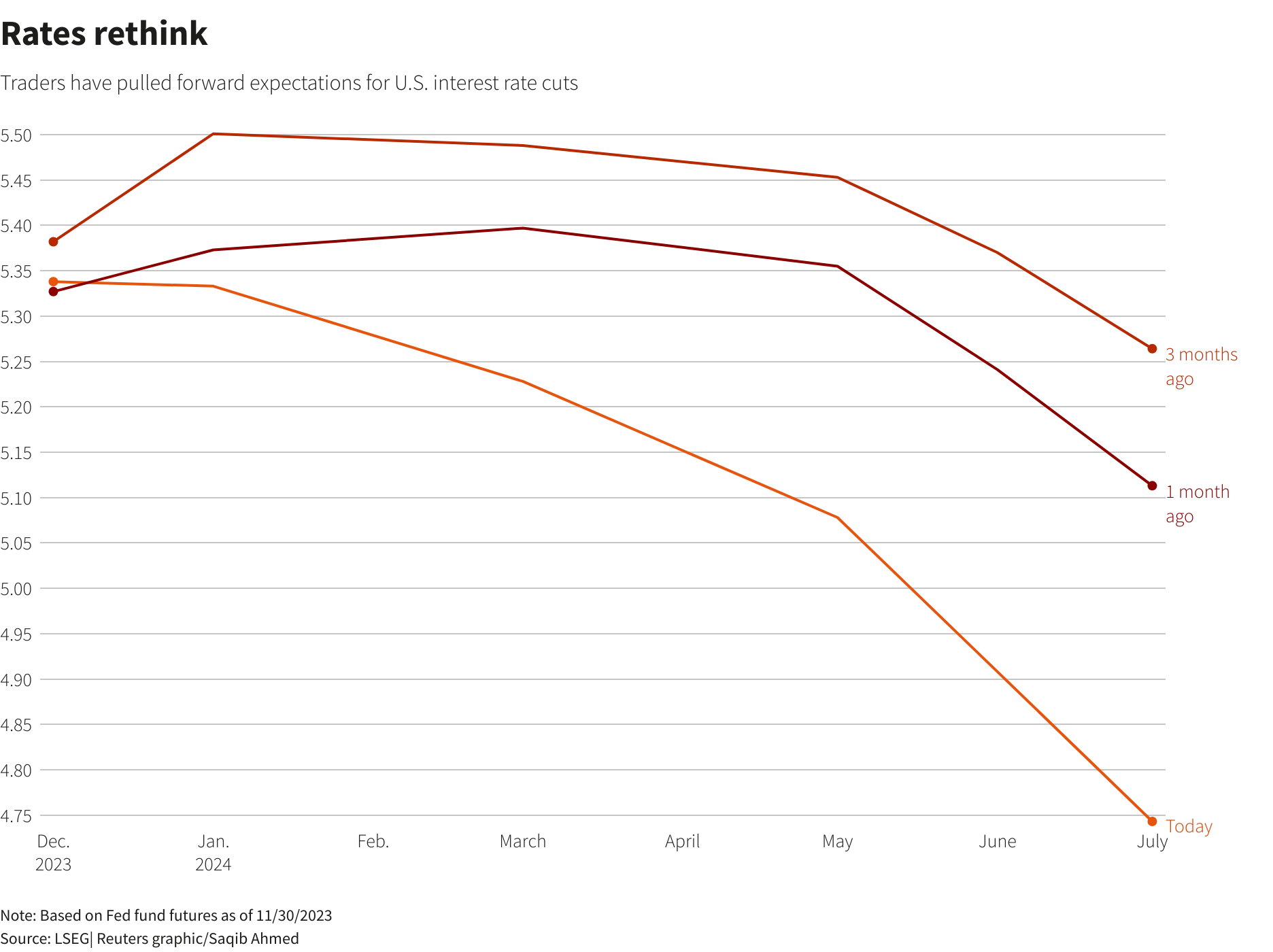

Markets now fully price in a 25 basis point U.S. rate cut in May, having seen a 65% chance earlier this week. Just a few weeks ago, a first cut was seen in June.

Bets for a March cut have also shot up, with traders pricing in nearly a 50% chance, versus 35% earlier this week.

That creates a headache for policymakers, as the speed of the bond and stock rally prompted by those changed expectations loosens the financing conditions they have been trying to tighten by raising rates.

U.S. Treasury yields are down more than 50 bps in November, the biggest monthly fall in over a decade.

A Goldman Sachs U.S. financial conditions index has eased 90 bps over the last month to its loosest since early September.

The bank has in the past shown a 100-bps loosening boosts growth by one percentage point in the coming year.

But for many, the fast fall in inflation means central bankers may shift closer to market thinking, as they did in 2021-2022 when investors challenged their “transitory” inflation view as price pressures surged.

Comments this week from U.S. Federal Reserve policymaker Christopher Waller, a hawkish and influential Fed voice, that he was increasingly confident inflation would return to its 2% target, has fuelled rate-cut bets.

In early November, Bank of England chief economist Huw Pill said mid-2024 might be time for cuts, a view also expressed by Greek central banker Yannis Stournaras.

“There are now committee members in all three (banks) willing to talk about rate cuts next year,” said Chris Jeffery, head of rates and inflation strategy at LGIM.

“Previously we’d had a stone wall of: higher for longer Table Mountain, rates need to stay in restrictive territory.”

Some analysts, like Deutsche Bank‘s, are forecasting even swifter cuts than markets.

“Central banks will probably pivot quicker than people think, and probably harder, and inflation (trends) basically give them the opportunity to do that,” said Dario Perkins, managing director of global macro at TS Lombard.

Traders now fully price a 25 bps ECB rate cut in April. In late October, they expected a first cut in July.

Thursday’s data showed euro zone inflation dropped to 2.4% in November from 2.9% in October, nearing the ECB’s 2% target.

Simon Harvey, head of FX analysis at Monex Europe, said recent weak data suggested that euro area monetary policy is too tight and has induced a recession.

“The ECB should begin to ease policy as soon as April 2024, with risks that a more sinister downturn in growth could warrant a rate cut as soon as March,” he said.

Reporting by Yoruk Bahceli in Amsterdam, Naomi Rovnick and Harry Roberston in London, and Davide Barbuscia and Ira Iosebasvili; additional reporting by Saqib Iqbal Ahmed; Writing by Dhara Ranasinghe; Editing by Catherine Evans

Our Standards: The Thomson Reuters Trust Principles.