A look at the day ahead in U.S. and global markets from Mike Dolan

Markets are betting central banks are done hiking interest rates, inflation is falling and corporate earnings are robust – and they now have just one more hurdle to clear to complete what’s set to be the best week of 2023.

The U.S. October employment report out later on Friday caps a hectic two weeks of central bank decisions, company updates and unnerving geopolitics. As the first major marker of U.S. economic strength in the final quarter of the year, the payrolls report packs a punch despite expected strike-related distortions.

Following a soft private sector jobs reading earlier in the week and a tick higher in weekly jobless claims, employment growth is expected to have slowed to some 180,000 new payrolls from 336,000 in September.

In the light of Thursday’s surge in stocks and bonds – based largely on an assumption the Federal Reserve, European Central Bank and Bank of England have now ended their rate hike campaigns – signs of a cooling labor market may be welcomed.

In advance of the release, S&P500 futures stepped back a bit from Thursday’s highs when the cash index boasted its biggest one-day gain since April by adding almost 2%. Even the small cap Russell 2000 (.RUT) jumped 2.7% in its biggest gain since June.

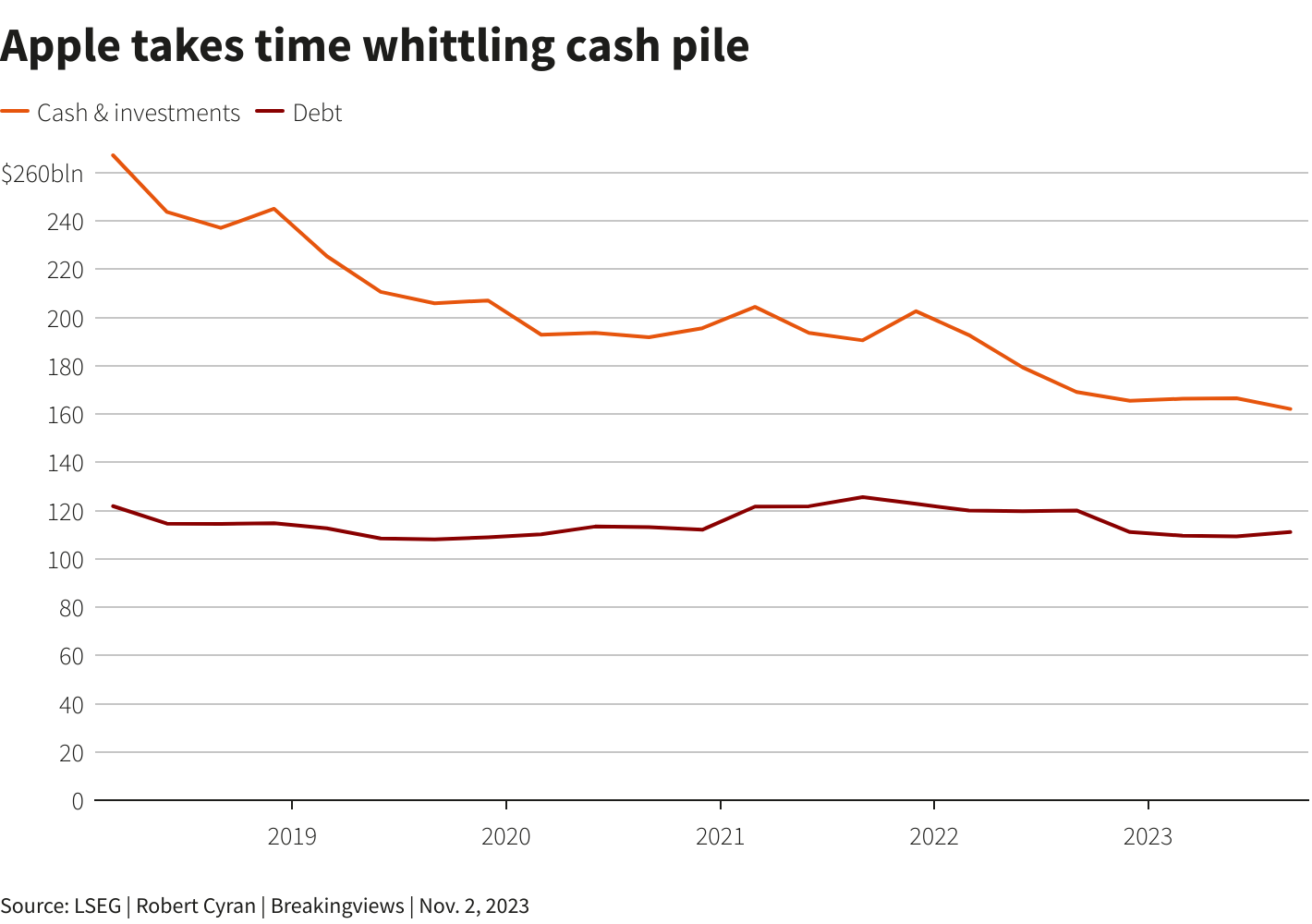

Part of the hesitancy is down to an underwhelming third quarter update from America’s most valuable firm Apple (AAPL.O), whose stock fell 3% in out-of-hours trade ahead of Friday’s open after its sales forecast for the holiday quarter missed Wall Street estimates despite a third-quarter profit beat.

And while S&P500 aggregate annual earnings growth for Q3 is tracking an impressive 5%, LSEG data shows Wall Street has downgraded fourth-quarter earnings growth estimates to 7.2%, down from 11% just before the reporting season began.

The interest rate relief this week is pervasive, however, as the Fed, ECB and BoE all paused tightening and U.S. Treasury debt sales worries ebbed somewhat.

Ten-year U.S. Treasury yields have recoiled almost 30 basis points from Wednesday’s highs to sit at 4.66% – and are on course for their biggest weekly drop since March.

U.S. Treasury (.MOVE) and equity market (.BIX) volatility gauges have subsided to their lowest levels since early last month.

What’s more, other incoming economic numbers underlined a reason for renewed market optimism after a torrid few months.

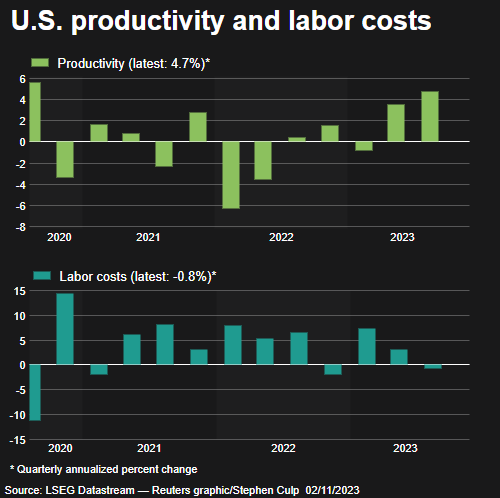

Labor Department statistics showed worker productivity grew faster than forecast in Q3 as labor costs declined — recording its quickest pace in three years. If sustained, that should help the Fed’s efforts to bring inflation back to target and may also reflect investment in technology and artificial intelligence.

Elsewhere, Chinese stocks (.CSI300) also caught a bid at last after a survey showed services activity improved slightly last month, even though new orders rose at their slowest in 10 months and employment stagnated.

U.S. service sector readings are also due later on Friday.

The dollar held steady (.DXY) ahead of the payrolls release.

With U.S. Secretary of State Antony Blinken in Isreal seeking a pause in the Gaza war as Israeli troops surround Gaza City, investors will likely keep a wary eye on the conflict there as the weekend nears.

And the crypto world may well take a deep breath after FTX founder Sam Bankman-Fried was late Thursday found guilty of stealing from customers of his now-bankrupt cryptocurrency exchange in one of the biggest financial frauds on record.

Key developments that should provide more direction to U.S. markets later on Friday:

* U.S. Oct employment report, ISM and S&P Global Oct U.S. service sector surveys; Canada Oct employment report

* U.S. corporate earnings: Eversource Energy, Sempra, Cardinal Health, Dominion Energy, Gartner, Church & Dwight, AMC, Liberty Media, Icahn Enterprises, Silvercrest

* Federal Reserve Vice Chair for Supervision Michael Barr, Minneapolis Fed President Neel Kashkari speak; Bank of England chief economist Huw Pill speaks

* U.S. Secretary of State Antony Blinken visits Israel

By Mike Dolan, editing by Emelia Sithole-Matarise

<a href=”mailto:mike.dolan@thomsonreuters.com” target=”_blank”>mike.dolan@thomsonreuters.com</a>. Twitter: @reutersMikeD

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

{kind=link}