Traders work on the floor of the New York Stock Exchange (NYSE) in New York City, U.S., September 26, 2023. REUTERS/Brendan McDermid/File Photo Acquire Licensing Rights

A look at the day ahead in U.S. and global markets from Mike Dolan

As Americans take a quick peek at markets on Friday before resuming a long Thanksgiving weekend, the takeaway will be sustained stock gains, punchier bond yields and a deepening underperformance of Chinese equities.

U.S. financial markets re-open after Thanksgiving for a truncated “Black Friday” trading session, where there will likely be as much focus on demand on High Street as Wall St.

But subdued market volatility, that saw the VIX “fear index” (.VIX) clock a post-pandemic closing low on Wednesday at just 12.75, was helped by signs of some calming of geopolitical tensions. A four-day ceasefire between Israel and Hamas appeared to be holding shakily on Friday with no major reports of attacks, although both sides were accused of violations.

Oil prices, which had lunged sharply lower again over the past two days amid a chaotic postponement of this weekend’s OPEC+ meeting, held steady on Friday and U.S. crude hovered just above $76 per barrel.

But with seasonal retail now in focus for many stock and economy watchers, S&P500 futures were higher ahead of the open and look set to extend gains to their highest in almost four months – and potentially on course for their best month in three years.

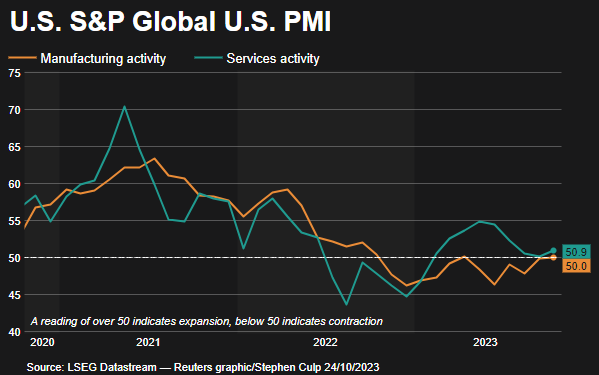

Better-than-forecast flash European business readings for November, released on Thursday, tee up equivalent surveys later in the day for the United States and may be contributing to a back-up in bond yields.

With some $148 billion of new 2-, 5- and 7-year Treasury notes up for auction next week, benchmark 10-year yields were about 5 basis points higher at 4.48% ahead of Friday’s shortened session. The dollar index (.DXY) remained under wraps, however, and edged lower.

But with most overseas stocks steady to higher, perhaps the most eye-catching moves involved the relentless drain on Chinese stocks (.CSI300) – which recorded their lowest close in almost a month and are now underperforming the MSCI all-country index (.MIWD00000PUS) by almost 20% for 2023 to date.

With data showing plunging foreign direct investment into the world’s second-largest economy this year, Friday saw overseas investors selling another net 6.2 billion yuan ($859.79 million) of Chinese shares via the Stock Connect – the biggest daily outflow in more than one month.

The decline marked yet another investor shrug at reports of further official moves to shore up China’s ailing property sector.

The Hang Seng Mainland Properties Index (.HSMPI) dropped 2.2% even after Bloomberg News reported on Thursday that Beijing might allow banks to offer unsecured short-term loans to qualified property developers for the first time.

Tension ahead of next year’s Taiwan elections didn’t help. Taiwan opposition parties, which seek closer China ties, registered separate presidential candidates on Friday after a dramatic split, potentially easing the way for the ruling party, which has defied Beijing’s pressure, to stay in power.

U.S. chip giant Nvidia has told customers in China it is delaying the launch of a new artificial intelligence chip it designed to comply with U.S. export rules until the first quarter of next year, according to Reuters sources.

In Europe, data showed Germany’s economy shrank slightly in the third quarter, confirming an initial estimate of a 0.1% fall. Finance Minister Christian Lindner is set to propose a supplementary budget for this year, which includes the suspension of limits on new borrowing after a budgetary crisis caused by a court ruling last week.

Dutch party leaders met on Friday for the first time since anti-Islam populist Geert Wilders won Wednesday’s elections to begin the difficult and lengthy process of building a coalition.

In banking, Britain’s Barclays (BARC.L) is working on plans to save up to 1 billion pounds ($1.25 billion) – which could involve cutting as many as 2,000 jobs, mainly in the British bank’s back office.

Key developments that should provide more direction to U.S. markets later on Friday:

* U.S. flash Nov business surveys from S&PGlobal

* European Central Bank vice president Luis de Guindos and Bank of Spain governor Pablo Hernandez de Cos speak

* U.S. corporate earnings: HWorld

By Mike Dolan, editing by Nick Macfie <a href=”mailto:[email protected]” target=”_blank”>[email protected]</a>. Twitter: @reutersMikeD

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

{kind=link}