The recent moves in EUR/USD have largely followed those of the dollar, with higher treasury yields propelling the greenback higher. We discussed in this article how we expect the pair to react to further upward swings in US rates. A 5.0% 10-year yield would bring EUR/USD to 1.02, by our calculations. At the same time, some idiosyncratic bearish drivers for the euro have recently started to emerge, mostly related to the deteriorating economic outlook in the eurozone.

Eurozone peripheral spreads have, so far, not been part of that set of idiosyncratic risks for the euro. Recently, though, the Italian BTP-German bund 10-year spread has jumped and briefly touched 200bp after the Italian government announced the 2023 fiscal deficit at 5.3% of GDP, up from the 4.5% April target.

In this note, we look at how the BTP-bund spread has historically impacted the euro and how this time may be different given the European Central Bank’s Transmission Protection Instrument (TPI) backstop.

The Italian budget backdrop and risks ahead

The disclosure of a few numbers from the updating note to the economic and financial document (NADEF), which sets the macro framework for the next Italian budget, did not offer big surprises with respect to what had been leaked over the past week – nor to what we had expected. According to the numbers available, the government has taken stock of a deteriorating economic environment, trimming growth forecasts and making explicit the impact of the so-called “super bonus” tax credit on current deficit and future debt.

According to the press release, the fiscal push to be funded in deficit – as proxied by the difference between the trend deficit and the planned deficit – will amount to 0.7% of GDP in 2024, a relevant but not huge amount by historical standards.

Debt stabilisation seems to be the main concern, and rightly so, given that we don’t know yet which fiscal rule will be in place starting January 2024. However, the very limited room for manoeuvre that the projected debt dynamics leave to the government represents a potential source of political risks. Firstly, within the governing alliance, as scarce resources will not allow ambitious electoral promises to be met in this budgetary round; secondly, between the Italian government and the EU Commission, should complaints on the excess of EU controls solicit pro-cyclical reactions on the EU side.

By the end of October, the Italian government must submit the draft budget to Brussels. Developments in negotiations on the reform of the stability pact may help to reduce background uncertainty and make this budget season an orderly one.

Peripheral spreads and TPI

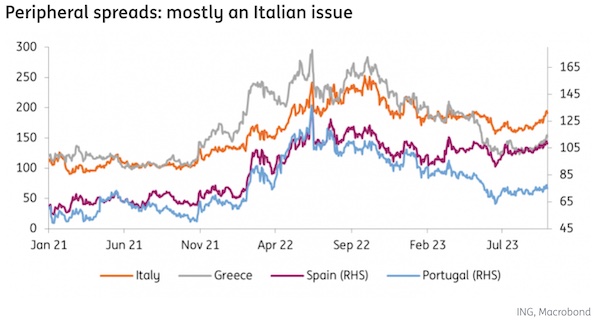

Eurozone peripheral spreads have generally declined since the introduction of the ECB’s TPI in mid-2022, although we have been observing a modest rebound in Spain and Italy’s spreads in the past weeks. As shown in the chart below (Spain’s spread on the right-hand axis), any real concern would be confined to the Italian bond market for now.

Italy’s bond market underperformance is not surprising. The country’s longstanding debt sustainability concerns are now re-emerging and being met with those surrounding Italy–EU frictions and the prospective reintroduction of the fiscal rule in 2024, as well as a worsening outlook for the Italian economy. The European Commission revised Italy’s growth forecasts to just under 1% for both 2023 and 2024.

The ECB’s hawkish narrative is undoubtedly adding pressure to peripheral spreads. Incidentally, amid discussions over accelerating the shrinking of the ECB balance sheet, officials are considering the idea of ending earlier what is effectively the ECB’s first line of defence for sovereign spreads: the flexible reinvestment of PEPP holdings.

Naturally, this puts more focus on the TPI, whose deployment is also tied to conditions including “sound and sustainable” fiscal policies. The ECB does give itself some leeway in the form of dynamically adjusting the criteria to unfolding risks and conditions – but this suggests that the bar for activating the TPI could have moved higher as the Italian government plans higher deficits.

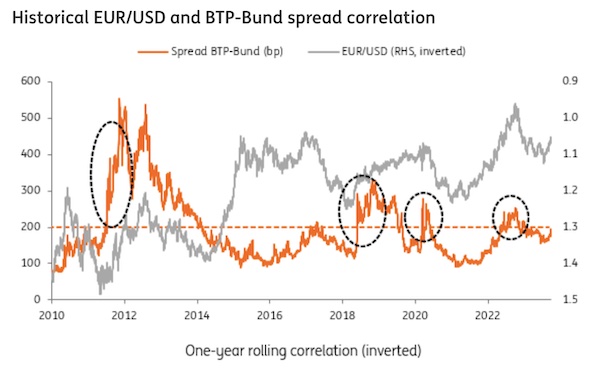

FX-BTP correlation normally picks up after Italian spread breaks 200bp

Political risk has not had an impact on the euro since the latest Italian government crisis in the summer of 2022. In that same period, the ECB introduced its TPI tool. In September, a new government secured a solid parliament majority after the elections, which contributed toward compressing the BTP-Bund spread.

Historically, markets have become exponentially sensitive to the BTP-Bund spread when it crosses the 200bp mark. That is also the threshold that normally coincides with a pick-up of the correlation between Italian spreads and the euro. In the chart below, we see how that correlation has played out with EUR/USD – although on many occasions it was EUR/CHF that showed higher sensitivity to Italian politics, as the franc often emerged as the preferred safe-haven currency when European risks flared up.

Why it could be different this time

There are two arguments that suggest the euro’s sensitivity to Italian bonds could be lower this time. The first is that the euro is already cheap and will struggle to price in more risk premium; the second is that the TPI backstop will limit the spillover into FX.

Political risks – just like geopolitical risks and energy-related shocks – impact the euro by making it trade at lower levels than its typical short-term drivers (rates and equities) would suggest. In other words, generating a risk premium compared to its short-term fair value.

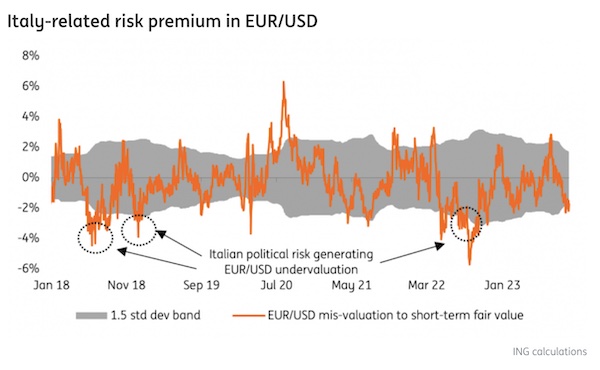

EUR/USD has suffered from intense selling pressure of late. Part of this was due to the selloff in US bonds – which has made the USD real rate even more attractive – but our estimates show that the pair is already trading at a 1.8-2.0% discount to its fair value. We believe this is primarily due to the worsening of the eurozone’s growth outlook and the risk of stagflation.

At the same time, we can note from the chart above that without having to go back to the extreme events of 2011, the past five years already saw three instances (twice in 2018, once in 2022) of Italian political risk generating a EUR/USD undervaluation larger than 2.0%. This time, the Italian government is not at risk of losing a majority, but the potential for rising friction with the EU following the reintroduction of fiscal rules may at least see that EUR/USD risk premium being kept in place. In other words, if there are more limited downside risks, the room for a rebound is also quite restricted.

When it comes to TPI, the tool has been put on the backburner by investors since peripheral spreads have been rather tight, leaving one key question for investors: would TPI be deployed in any instance of dangerously widening spreads (also if caused by political turmoil), or only if the bond selloff is induced by ECB tightening? The swift ECB reaction to Italian spreads widening in 2022 may, for now, deter excessive bearish speculation and limit the spillover on the euro. However, should the BTP-Bund spread reach structurally higher levels and Italy–EU relations deteriorate over the fiscal rule, we could see TPI conditionality becoming the centre of the discussion in an already divided Governing Council.

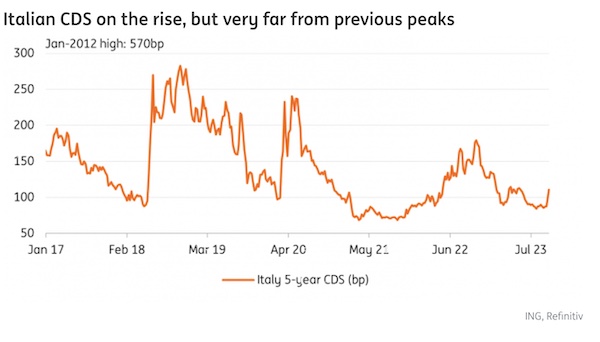

Ultimately, whether the Italian government will be willing to tolerate a high BTP-Bund spread to have more fiscal room will be key – especially if debt sustainability concerns should rise again. We have already observed a rise in Italian CDS in the past week, although still far from the levels seen in other political crises or during the Covid-19 pandemic.

Our view on the euro

EUR/USD is enjoying a relief rally to 1.0600 at the time of writing, primarily thanks to USD-negative quarter-end flows. Domestic news and the overall environment continue to point to EUR/USD weakness, and our rates team sees more upside risks for back-end UST yields, which could pave the way for a further short-term depreciation in EUR/USD.

Should we see a material deterioration in the Italian bond market – and barring a swift reaction by the ECB to calm investors – EUR/USD downside risks would extend to the 1.00/1.02 area in an environment where US bonds remain under pressure on the back of solid US data and the Federal Reserve remains hawkish.

The Swiss franc has typically been a beneficiary of stress in the euro area and EUR/CHF usually has a negative correlation with meaningful widening in the BTP-Bund spread. During periods of deflation, Swiss authorities would typically intervene to buy FX and prevent the Swiss franc from appreciating too much. However, in today’s inflationary world, the Swiss National Bank is now actively using the Swiss franc as a monetary policy tool and is selling FX to manage the Swiss franc stronger. The SNB just announced a cut to its balance sheet by CHF 40 billion in the second quarter by selling FX – an acceleration from the 32 billion seen in the first quarter.

Presumably, if stress in the euro area created more natural demand for the Swiss franc, the SNB would sell less FX. Yet, the main message here is that EUR/CHF is a very managed pair, and while problems in the euro area stress could hasten a return to 0.9500, the SNB could easily switch back to buying FX to keep EUR/CHF under control.

Source: ING

{kind=link}