Introduction

The COVID-19 shock brought about large social and economic repercussions of various sorts. The pandemic disrupted different sectors and activities. Many effects of the pandemic have been already investigated and discussed. Others, such as the impact on the biopharmaceutical industry, are not well understood yet and deserve further attention.

In general, health shocks generate two types of effect on biopharmaceutical firms. First, these episodes increase uncertainty and fear, impacting the whole economy (including this industry) negatively. It is already documented that the COVID-19 pandemic, together with the lockdown measures implemented by authorities, generated massive uncertainty, economic disruptions and high volatility in financial markets.1–3, In fact, volatility spillovers in financial markets were more pronounced than during the 2008 crisis.4 On the other hand, health shocks also provide opportunities associated with the production of treatments for biopharmaceutical companies.5 The net result of these competing forces for biopharmaceutical firms is ambiguous.

The design and development of new drugs is a challenging and slow-paced process. The duration of this process for vaccines is on average 10 years according to the World Health Organization.6 In the case of COVID-19, the Pfizer-BioNTech and Moderna vaccines arrived to the market less than one year after the outburst of the pandemic, and have been very effective in the fight against the SARS-CoV-2 virus: they can thus be considered as a success from the point of view of public health.

Are vaccines an economic success as well for pharmaceutical companies? Public opinion sometimes seems to think so. In fact, one of the arguments put forward by some anti-vaccination groups is precisely that the main outcome of vaccination campaigns is the generation of large profits for pharmaceutical companies. A more thorough analysis, though, shows that the rate of return of vaccines is typically low, since their demand is highly uncertain and their production costs are non-linear.6 Consequently, vaccines may imply an increase in turnover in the short term but, unlike drugs of prolonged treatment or periodic use, they usually do not warrant a sustained and permanent increase of sales over time.

Our investigation intends to shed light on this issue. More in particular, the objective of this paper is to explore the impact of the COVID-19 pandemic on a sample of biopharmaceutical companies, paying special attention to the development and supply of vaccines. Because of our proximity to the pandemic, we cannot carry out an exploration of this topic with the desirable perspective yet and over the medium or long run. What we can do, however, is to perform a short run analysis by examining the performance of share prices in the stock market and assessing whether biopharmaceutical firms have registered extraordinary or abnormal returns in response to news about the unfolding of the pandemic and the development of vaccines (see Appendix 1 for the main landmarks). Following the financial literature, our exploration is grounded on the assumption that the stock market is able to gauge and forecast the business opportunities and risks potentially affecting companies, impacting share prices accordingly.

Recent studies have documented the reaction of financial markets to news about potential opportunities and risks associated to the COVID-19 pandemic. Chatjuthamar et al show that bad news (confirmed cases/deaths) affected several stock indices.7 Some authors even report that bad news about the pandemic affected to a greater extent than good news.8 Other studies analyzing the answer of different stock indices to confirmed cases, deaths and recoveries from COVID-19 suggest that prices´ elasticities indicated a recovery of stock markets throughout 2020 in response to the improvement in the survival of patients, the development of herd immunity and the expected success in the development of vaccines in the short term.9 Regarding the Chinese stock market, Xu et al find that the news about the evolution of the pandemic not only affected share prices; the market also lost sensitivity to the companies’ economic and financial disclosures in such a way that share volatility became more associated to the news about the pandemic than to information about the companies themselves.10 Other papers claim that retail investors (individual investors with direct access to investment platforms) helped flatten the negative effects on equity markets by injecting more liquidity into the system during the lockdown.11 The assessment of abnormal returns of several Asian stock indices after 20 January 2020 shows negative effects from the COVID-19 outbreak, but positive effects are also observed in certain sectors such as pharmaceutical manufacturing, perhaps because this sector was contributing to alleviate the epidemic.12 Other recent studies have also addressed the impact of the opportunities and risks of the COVID-19 pandemic on the pharmaceutical industry in specific countries.13–15

The contributions mentioned above, among others, show how the news about COVID-19 heavily affected stock markets. However, as far as we know, no study has looked at how the news about the spread of the pandemic and about the vaccine developments have impacted the stock prices of biopharmaceutical companies elaborating COVID-19 vaccines. Employing a holistic approach, we consider the effect of both categories of news (about the evolution of the COVID-19 pandemic and about the progress in the elaboration of COVID-19 vaccines) on a group of pharmaceutical and biotechnological companies.

This paper summarizes and extends the discussion and results provided in Diaz16 The empirical exercise relies on event analysis. Event analysis is a tool widely used in finance to detect short run abnormal results of some companies with regard to the market, and therefore seems a convenient technique for our exploration.

According to our results, the news about the progression of the pandemic have had a moderate impact on the stock prices of biopharmaceutical companies. Most companies do not experience abnormal returns. Moderna and Novavax, two biotechnological companies, constitute the most important exception, with large positive abnormal returns, which vanished over time. Moreover, Johnson and Johnson and Pfizer registered small positive and negative, respectively, abnormal returns over that period.

Second, as far as the information about vaccine advancements is concerned, the stock values of Pfizer, Moderna and Novavax, were positively affected by the disclosure of their Phase III findings; this effect is not present with respect to J&J (Johnson and Johnson). News about an agreement between Moderna and the EU (European Union) to deliver a large number of vaccines generated large positive share value increases for the firm. Instead, declarations from the European Medicine Agency about some vaccine developers did not impact US stock markets, according to our data.

The paper contributes to shed some light on the impact of pandemics on financial markets, which is not yet well understood.17 It also provides insights about the milestones which financial markets deem crucial for the success of vaccines. Interestingly, our findings suggest that announcements of Phase III results seem to be more crucial than approvals by regulatory agencies, which is consistent with prior results.18

The structure of the paper after the introduction is the following: Background and Hypotheses discusses the background and hypotheses of the investigation; Sample and Methodology comments on our data, sample and methodology; A First Look at the Data: The Evolution of Stock Market Prices details some descriptive statistics of the data; Event Analysis presents our model and results; Results and Discussion discusses our findings and Concluding Remarks provides some concluding remarks.

Background and Hypotheses

First, our paper is related to contributions which analyze the effect of information about research and development on the share values of pharmaceutical companies.19,20

Second, our contribution is connected to pieces of research exploring the link between COVID-19 and share values as, for example, Heyden and Heyden21 There are contributions showing that the COVID-19 pandemic, together with the lockdown measures implemented by authorities, generated massive uncertainty and volatility in financial markets.1–3 Other articles have detected irrational behavior and panic.22,23

Alam et al and Behera and Rath find positive effects of the pandemic on the stock prices of specific sectors of Australia and India, respectively.24,25 The impact of COVID-19 vaccines on stock prices, though, has been sparsely analyzed so far, although there are several papers focusing on this issue.1,26,27

Our research is connected as well to Hwang. This contribution shows that the announcements of Phase III clinical trials affects the share values of pharmaceutical and biotechnological firms.18

In this research, we combine the insights and approaches represented in these papers and apply them to the analysis of the evolution of COVID-19 and the development of COVID-19 vaccines. More in particular, we explore to what extent news associated with the expansion of the pandemic and to partial successes in the design and manufacturing of COVID-19 vaccines affect the share values of a set of biopharmaceutical firms.

Sample and Methodology

Sample

In this paper, we are primarily interested in the response of equity prices of vaccine developers. At the beginning of 2023 eleven vaccines had been granted emergency use by the World Health Organization. Five were produced by pharmaceutical or biotechnological firms listed in the NYSE or Nasdaq: Nuvaxovid (Novavax), Spikevax (Moderna), Comirnaty (Pfizer), Ad26.COV2.S (Janssen-J&J) and Vaxzevria (AstraZeneca). BioNTech started to operate in Nasdaq on October 11, 2019, hence we do not have enough data available from this company to perform our empirical exercise (see Appendix 2 for brief expositions of company histories and Appendix 3 for the dates of Emergency approvals of COVID-19 vaccines by WHO).

We focus on shares traded in two key US stock markets, the New York Stock Exchange and Nasdaq, to warrant homogeneity among the companies and markets considered. The companies listed in these markets for a long enough time frame and producing COVID-19 vaccines are Pfizer, Johnson and Johnson, Astra Zeneca, Moderna and Novavax. Johnson and Johnson undertook the production of the COVID-19 vaccine through its affiliate Janssen Pharmaceutica; since this last company is not listed in the stock exchange, we use as an approximation the stock of the parent company, Johnson and Johnson.

Moderna and Novavax are two small biotechnological companies. Their size is not irrelevant for this analysis. Biotechnological R&D is a long, complex and highly uncertain activity. Small biotechnological companies are usually very specialized and focus on a small portfolio of products. They are high risk, high reward opportunities for investment, with large potential gains if a breakthrough comes about but exposed at the same time to high probabilities of failure. This company profile may be preferred by short-term opportunistic investors with low-risk aversion. Accordingly, these firms are prone to large stock price oscillations in response to new information. In particular, events like regulatory milestones or R&D breakthroughs may entail large value fluctuations.28 Large pharmaceuticals, instead, have a wider portfolio of products, meaning that risks and returns are more diversified and that the effect of particular events is more modest.

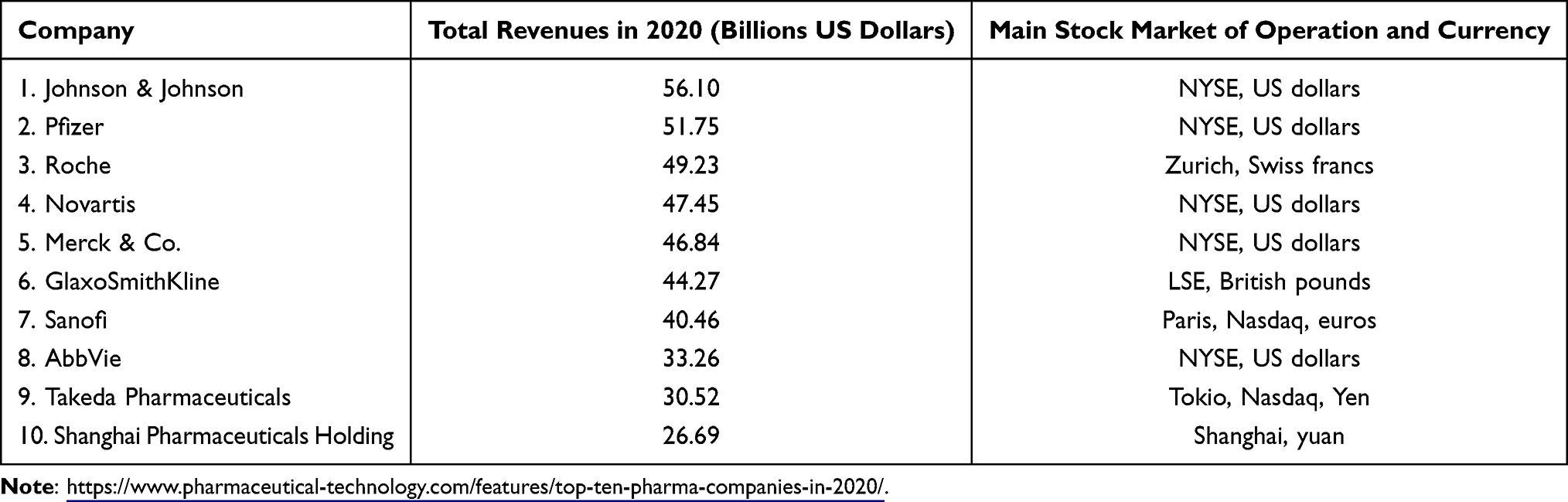

Johnson and Johnson and Pfizer belong to the Top Ten pharmaceutical firms when ranked by total revenues of 2020, the year of the beginning of the pandemic (see Table 1). We include in our sample other companies from the Top Ten list that had not engaged in COVID-19 vaccines at that time (Novartis, Merck & Co., Sanofi and AbbVie) to compare their performance with the vaccine developers. Therefore, our sample encompasses the following nine firms: Pfizer, Johnson and Johnson, Astra Zeneca, Moderna, Novavax, Novartis, Merck & Co., Sanofi and AbbVie).

|

Table 1 Top ten Pharmaceutical Companies by Revenues in 2020 |

Our baseline study works with stock price data from June 6, 2019 to December 31, 2021 although the set of events we consider finishes in April 2021.

Method

Event analysis explores the reaction of stock markets to news. A key concept in this technique is abnormal returns (AR) or excess returns associated with company shares; abnormal returns are brought about by the active demand from potential investors driven by sound expectations about the evolution of the company. The computation of abnormal returns is typically performed considering an index from the stock market as benchmark and suggest that a particular firm outperforms the rest of the market.

Define the return of firm j in time t as

Where Pjt is the share price for firm j in t.

The abnormal returns (AR) for the firm j in time t is the difference between the actual return for j in time t and the expected or predicted return for that date (Equation 2):

Where  is the abnormal return,

is the abnormal return,  is the actual return and

is the actual return and  is the expected or predicted return for firm j in time t.

is the expected or predicted return for firm j in time t.

In turn, the expected or predicted return is estimated over the estimation window assuming a particular model. In the baseline case, this particular model is the market or Single Index Model29,30 whereby

Where Rmt is the return of the index in t. The parameter βj stands for the correlation between the return of the market and the return of firm j in t; αj is the intercept. Equation (3) is estimated by Ordinary Least Squares (OLS) over the estimation window. We take the New York Stock Exchange (NYSE) Composite Index as the return for the market in our empirical application.

The Single Index Model is the most widely accepted model.31 It is used also by Alcaide et al and Zhang26,27 It assumes a risk-free rate invariant over time; this hypothesis does not appear as a serious concern in this research because the risk-free rate impacts both the share price of the companies and the index analogously. Nonetheless, we have performed the estimations assuming alternative models, as it will be discussed in the subsection on robustness below.

If we aggregate over an event window, defined as the time (in days) between t1 and t2, we get an expression for the CAAR or cumulative aggregate abnormal return over the event window:

For t1<t2.

A First Look at the Data: The Evolution of Stock Market Prices

Figure 1 shows the behaviour of the shares prices of the companies in our sample and the New York Stock Exchange Composite Index (NYSE) between June 6, 2019 and December 31, 2021. The NYSE exhibited an increasing trend between June 2019 and the beginning of the pandemic. It fell dramatically on March 18, 2020. Afterwards the NYSE started to grow gradually, peaking around the end of 2021.

|

Figure 1 Evolution of the NYSE Composite and company share prices and the NYSE Composite, June 6, 2019- December 31, 2021. Note: Closing values in all cases. |

The firms in our sample registered different behaviors with respect to the NYSE index. We can distinguish three main categories of companies. There is a first group of firms displaying high correlation with the NYSE: Pfizer, Astra Zeneca, J&J, Sanofi and AbbVie.

Two other companies, Moderna and Novavax, exhibit large volatility, with pronounced humps around mid-2021 and decreases afterwards which entailed remarkable changes in the price of the stock. Before the pandemic the stock of Moderna was slightly below 20 dollars whereas at the end of 2021 it reached 253.98 dollars. Novavax was traded at 5 dollars before the pandemic and at 143.07 on December 21, 2021.

Finally, Merck and Novartis exhibit a lower correlation with the index over the time period considered.

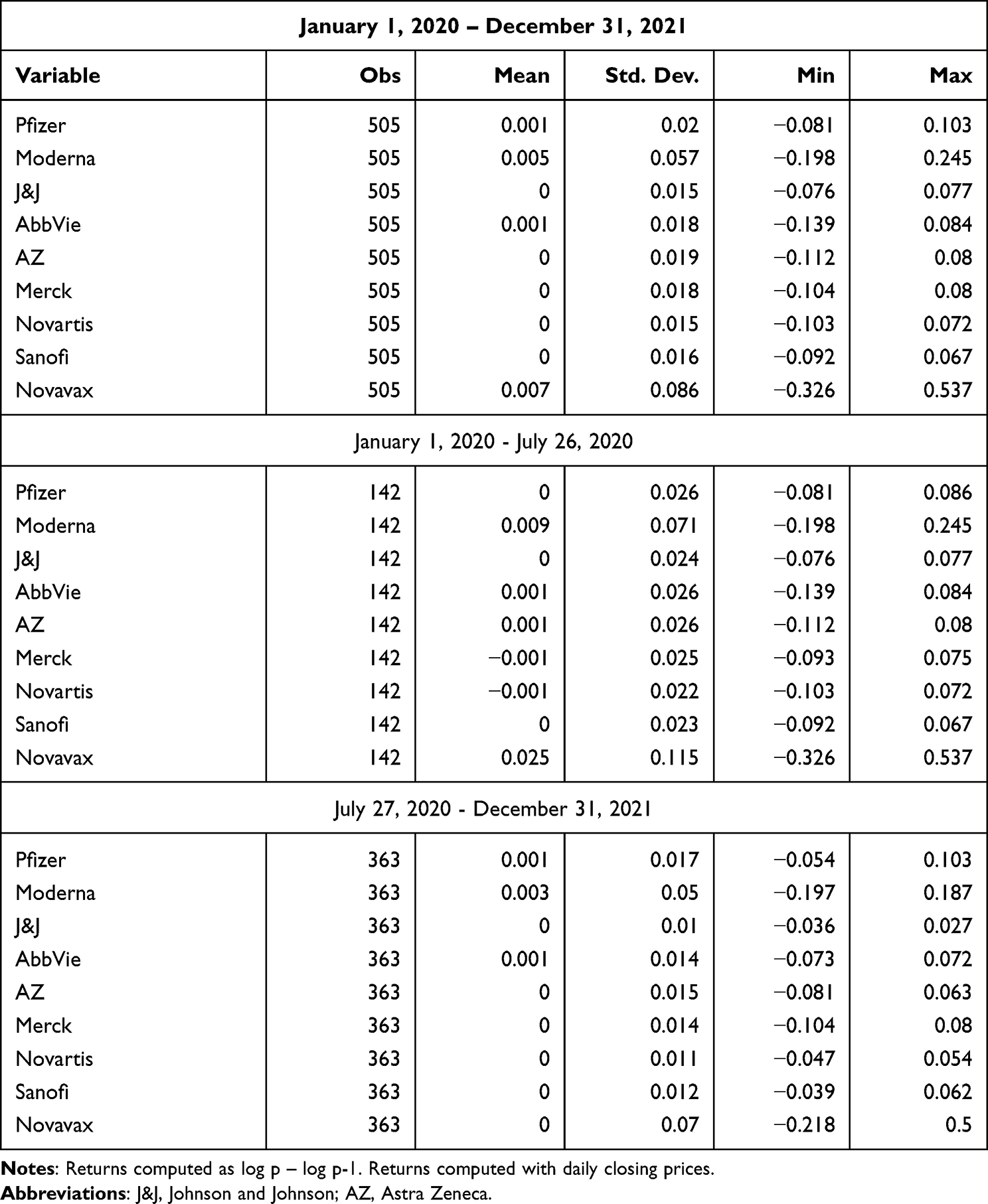

Table 2 summarizes some descriptive statistics for company returns. Pfizer, Moderna, Novavax and AbbVie have positive returns over the whole period, while the largest volatility (measured by the standard deviation) corresponds to Novavax and Moderna (0.057 and 0.086, respectively). Moreover, volatility is larger in the first subperiod for all companies, which is consistent with the financial turmoil brought about by the expansion of the pandemic.

|

Table 2 Descriptive Statistics, Company Returns |

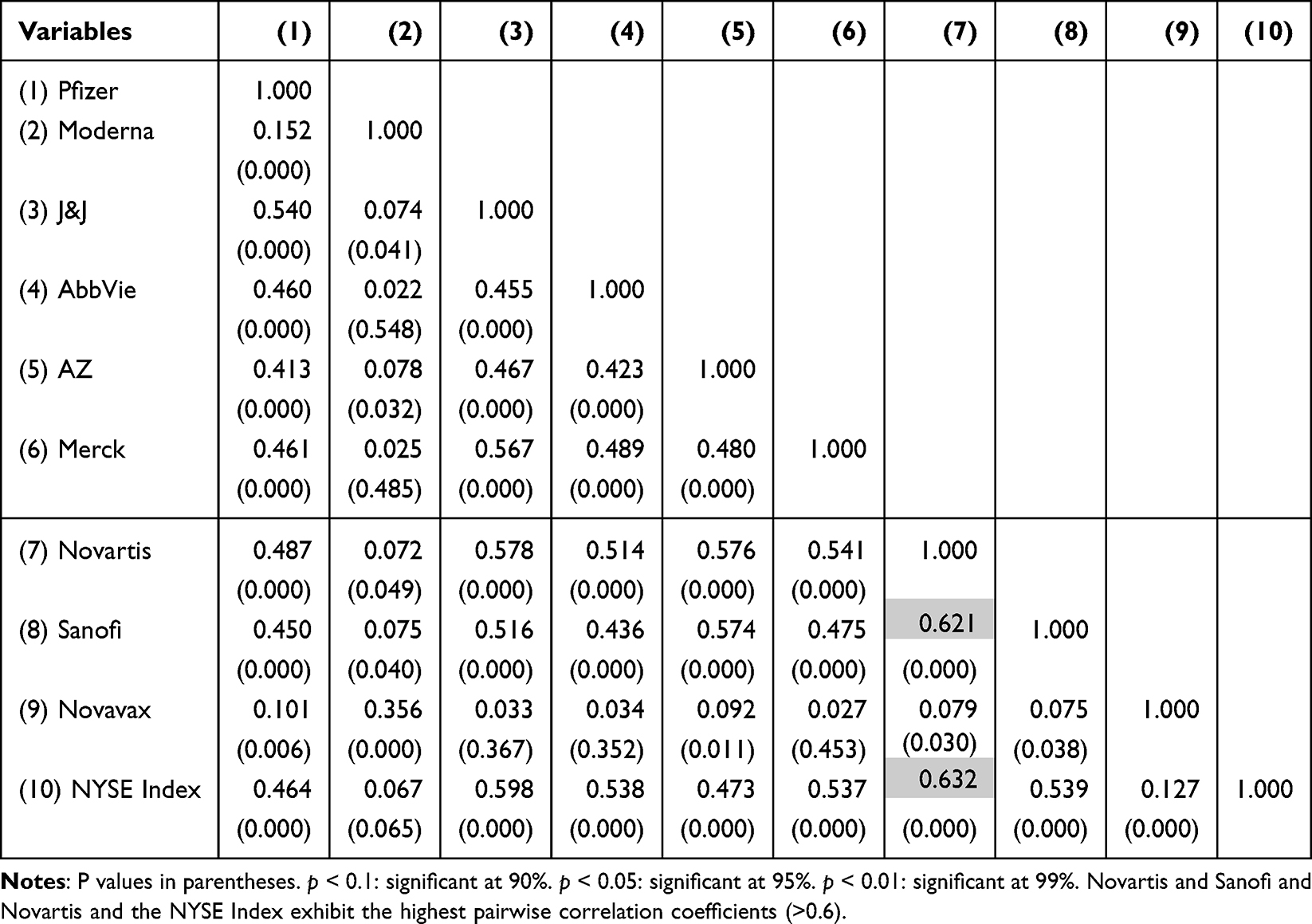

Table 3 displays pairwise correlations among companies. All correlations are positive. Novartis and Sanofi and Novartis and the NYSE register the largest (significant) correlations, higher than 0.6. In addition, there is a significant and high correlation (0.5) between the following pairs, organized by columns: (1) Pfizer with J&J; (3) J&J with Merck, Novartis, Sanofi and NYSE; (4) AbbVie with Novartis and NYSE; (5) Astra Zeneca with Novartis and Sanofi; (6) Merck with Novartis and NYSE; (8) Sanofi with NYSE. Moderate correlations, between 0.3 and 0.5, are observed for most of the other pairs. Moderna and Novavax register a pairwise correlation coefficient of 0.356; their correlation with the rest of the companies is very low, suggesting again different performances of the two small biotechnological firms and the more consolidated companies.

|

Table 3 PairwiseCorrelations, Company Returns |

Event Analysis

Model Specification

Nine biopharmaceutical companies listed in the NYSE or Nasdaq are considered in this paper for the event analysis. Six of them belong to the Top Ten by revenues in 2020 (Table 1); the other three are vaccine developers Moderna, Novavax and Astra Zeneca. The rationale for the focus on firms listed in the NYSE or Nasdaq is to avoid the potential heterogeneity associated with specific characteristics of other markets or countries. We concentrate for this research in the US financial markets because US is the main market of operation for four firms in our sample: Pfizer, Moderna, J&J and Novavax. We capture the behavior of the stock market as proxied by the New York Stock Exchange Composite. We work with daily closing prices.

We cover two main kinds of events, defining in turn two subperiods: the first covers the outburst and spread of the pandemic and the corresponding news and comprises the first five months of COVID-19. The second focuses on the last stages in the development of vaccines, from July 2020 to April 2021 (negotiations between governments and vaccine developers started, while vaccine elaboration was still in progress).

We set time-symmetric, short event windows (−3,3), starting three days in advance and ending three days after the event. Short windows is the standard practice when working with events causing high volatility.32 Moreover, small windows help isolate and distinguish different causes of price variations. In addition, new information usually reflects into prices very quickly, and this feature was indeed especially pronounced in the case of COVID-19 vaccines.

The estimation window goes from June 6, 2019 to one month before the event.

The evolution of the economic and geopolitical scenario in the recent past has been complex. Particularly because of the surge in inflation and the conflict between Russia and Ukraine. These could be considered potential confounding factors for our analysis. We think, however, that the effects of both phenomena start to materialize after the end of the time horizon we consider.

A deep analysis of these factors is outside the scope of this paper, but some considerations may be useful. In 2021, the economic activity in most countries recovered from the dip caused by the pandemic. In parallel, inflation started to increase because of supply disruptions and rises in the price of energy. Appendix 4 shows the behaviour of quarterly GDP growth and inflation for US, the European Union and the OECD. This supply shock, together with the restrictive monetary policies implemented by central banks, brought about a deceleration in the economy. In our view, though, the effects of this deceleration come about after the end of our time span. Quarterly growth rates for the US in 2021 were 1.54%, 1.71%, 0.66% and 1.70%. In the first half of 2022, though, the US economy experienced a brief contraction: growth was −0.41% in Q1-2022 and −0.14% in Q2-2022. In the second half of 2022 GDP growth was again positive. As far as the UE is regarded, growth was positive throughout 2021 and the first three quarters of 2022, although it fell somehow from Q4-2021 onwards. Finally, deceleration for the whole 0ECD started in the first quarter of 2022. Hence it seems reasonable to assume that the activity slowdown took place outside the time span covered for our paper, which ends in April 2021.

The conflict between Russia and Ukraine, although latent since 2014, officially exploded on February 24, 2022. It is true that the invasion had probably started several months before (the specific date is unclear); nonetheless, it seems far enough from our time horizon, which ends in April 2021, to significantly impact our analysis.

COVID-19 Announcements

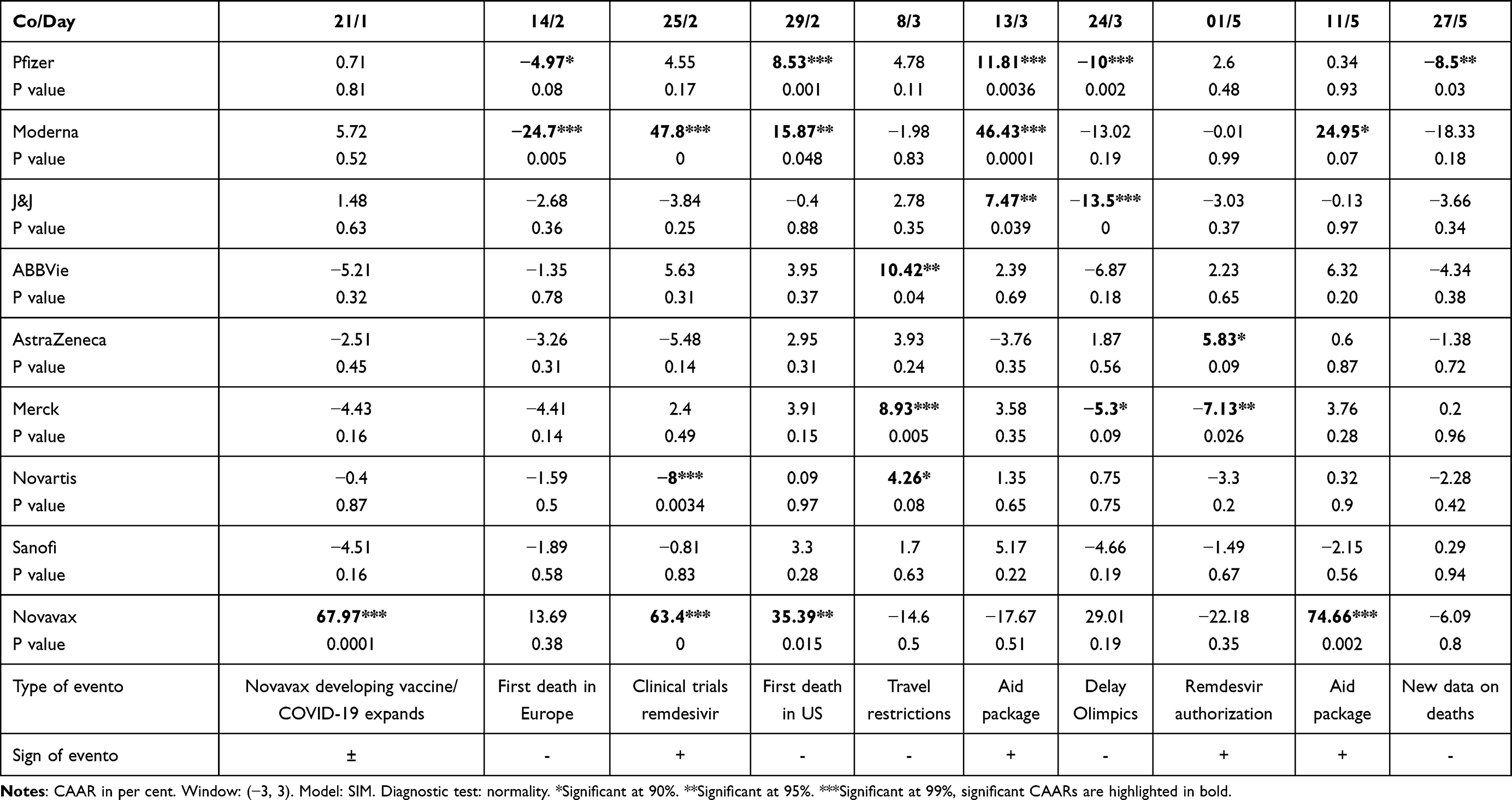

We work with 10 relevant events happening in the first months of the pandemic, associated with announcements about the pandemic. Five events are positive because they mean progress against the pandemic (like a potential vaccine, a treatment for COVID-19 and public aid packages). Six events are negative as they convey information about the expansion of COVID-19. One day comprises a favorable and an unfavorable event. CAARs for each event are in Table 4.

|

Table 4 CAARs, Biopharmaceutical Companies, January–June 2020 |

The date of events about COVID-19 announcements are as follows (see Appendix 1):

- Events 1 and 2: January 20, 2020, WHO report; January 21, 2020, Novavax announces vaccine.

- Event 3: February 14, 2020, first death in Europe.

- Event 4: February 25, 2020, clinical trials of remdesivir start.

- Event 5: February 29, 2020, first COVID-19 death in US.

- Event 6: March 8, 2020, travel restrictions in Italy.

- Event 7: March 13, 2020, aid package.

- Event 8: March 24, 2020, delay in Olympics announced.

- Event 9: May 1, 2020, FDA authorizes remdesivir.

- Event 10: May 11, 2020, aid package.

- Event 11: May 27, 2020, data on deaths.

The last row in Table 4 indicates the sign of the event, positive if the expected impact is an increase in the demand of shares and therefore a higher CAAR and negative otherwise. The announcement by Novavax about the development of a COVID-19 vaccine in January 20 is received by the market with a large positive CAAR. Instead, news about the first death in Europe attributed to COVID-19 brings about negative CAARs for Pfizer and Moderna. Information about the start of clinical trials with remdesivir and the first death in US soil bring about substantial CAARs for Novavax and Moderna, and there is also some positive reaction for Pfizer in the last case. The aid package disclosed on March 13 generates abnormal positive returns for Pfizer, Moderna and, to a lesser extent, J&J. A second aid package announced in May 11 entails positive CAARS again for Moderna and Novavax.

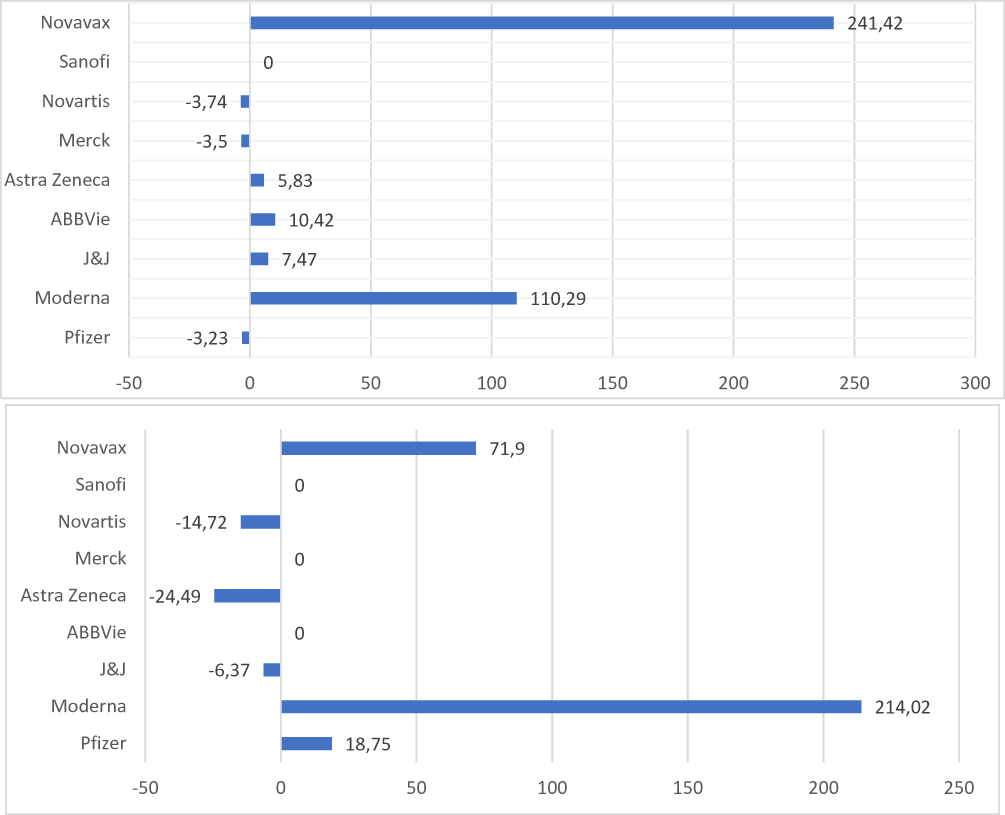

Figure 2 summarizes visually the information condensed in Table 4 and Table 5 by showing the sum of CAARs for every company (only significant CAARs are represented). Novavax and Moderna enjoy the biggest positive CAARs (241.42% and 110.29%). There are also small positive CAARs for Astra Zeneca, AbbVie and J&J and small negative abnormal return for Novartis, Merck and Pfizer.

|

Table 5 CAARs, Biopharmaceutical Companies, November 2020-April 2021 |

|

Figure 2 Net abnormal results by companies and subperiods (%). Top panel: First subperiod. COVID-19 pandemic announcements. Bottom panel: Second subperiod. COVID-19 vaccines announcements. Notes: Net abnormal results (in per cent) are computed as the sum of the CAAR displayed in Table 4 and Table 5. Only significant CAARs are considered. |

Positive CAARs are linked both to favorable news and unfavorable news. Aid measures, though, seem to generate positive CAARs.

The impact of COVID-19 news on the stock values of biopharmaceutical companies was thus moderate and lower than one could imagine on a priori grounds, despite the large volatility in the US stock market at that time.2 The exceptions are Novavax and Moderna. These firms were able to convey optimistic expectations to financial markets, creating a favorable sentiment and attracting investment. Pfizer, instead, was probably damaged by the negative market sentiment already detected.1

COVID-19 Vaccines Announcements

In this subsection, we discuss the effects of some announcements related to the development of COVID-19 vaccines. We focus mainly on positive events because share prices are more correlated with development progress than with negative episodes.18

The date of the events about COVID-19 vaccines we consider are as follows:

- Event 1. November 9, 2020. Phase III results of Pfizer are announced.

- Event 2. November 16, 2020. Phase III results of Moderna are announced.

- Event 3. November 25, 2020. Announcement of a deal between Moderna and the European Commission for the purchase of vaccines.

- Event 4. December 11, 2020. FDA approval, Pfizer.

- Event 4. December 18, 2020. FDA approval, Moderna.

- Event 5. January 6, 2021. Moderna vaccine approved in the European Union (EU).

- Event 6. January 29, 2021. Phase III results for J&J and Novavax.

- Event 7. February 27, 2021. FDA approves J&J.

- Event 8. March 19, 2021. Embolic episodes in the AstraZeneca vaccine.

- Event 9, April 7, 2021. Clots are reported to be uncommon side effects of the AstraZeneca vaccine.

Table 5 details the CAARs for these event windows.

On November 9 Pfizer announced that, according to Phase III clinical trials, the effectiveness of its vaccine was 90%. On that date and over most of the following days the Pfizer stock started to register positive CAARs, that were gradually larger and became significant on November 25, 27 and 28. These CAARs, in any event, were moderate in size. Meanwhile, Moderna disclosed a 94.1% efficacy of its candidate on November 16. It seems, however, that these excellent results were anticipated by the market some days in advance, because the Moderna stock registered a positive and significant CAAR of 28.5% already on November 11. On November 24 Moderna closed a deal with the European Union to provide 160 million doses of its vaccine. CAARs for the company were large, positive and significant between November 23 (showing again some anticipation from the market) and November 28. It is feasible that the agreement Moderna-EU was strongly welcomed by the market because of the sound results of Phase III (announced several days in advance), which greatly increased the chances for a successful Moderna vaccine.

The Pfizer vaccine received the emergency approval from the FDA on December 11; the company experienced a negative, moderate and significant CAAR on that day. Our hypothesis here is that this piece of news had been already anticipated by the market and translated into positive and significant CAARs some days in advance at the end of November and the beginning of December. Likewise, FDA granted an emergency approval to Moderna on December 18; the company registered a negative (but not significant) CAAR that day because this information was already discounted.

It is interesting to notice that we do not observe in the market any behavior suggesting that investors disagreed with the simplified and expedited procedures followed by the FDA to provide emergency authorizations to vaccines, despite the substantial reduction implied in the time-to-market for these products if compared with historical trends. Rather, it seems that investors supported the public authorities’ strategy of providing a swift and strong answer to the pandemic.

Phase III results were disclosed for J&J and Novavax on January 29; that same day the European Medicines agency approved the Astra Zeneca vaccine. The CAARs on those dates for J&J and Astra Zeneca were negative (and significant for Astra Zeneca). The Phase III results for J&J vaccine, although encouraging, were inferior to those of Pfizer and Moderna. It is possible that this fact restrained the demand for the J&J stocks. Novavax, instead, registered a very large positive and significant CAAR of 72%. The emergency approval of the J&J vaccine on February 27 did not have any impact on its stock price, either. On March 19 some adverse effects of the Astra Zeneca vaccine were reported, without any noticeable effect on the market in the form of a significant CAAR. There were no effects, either, from an announcement by the European Medicines Agency explaining that these side effects were rare.

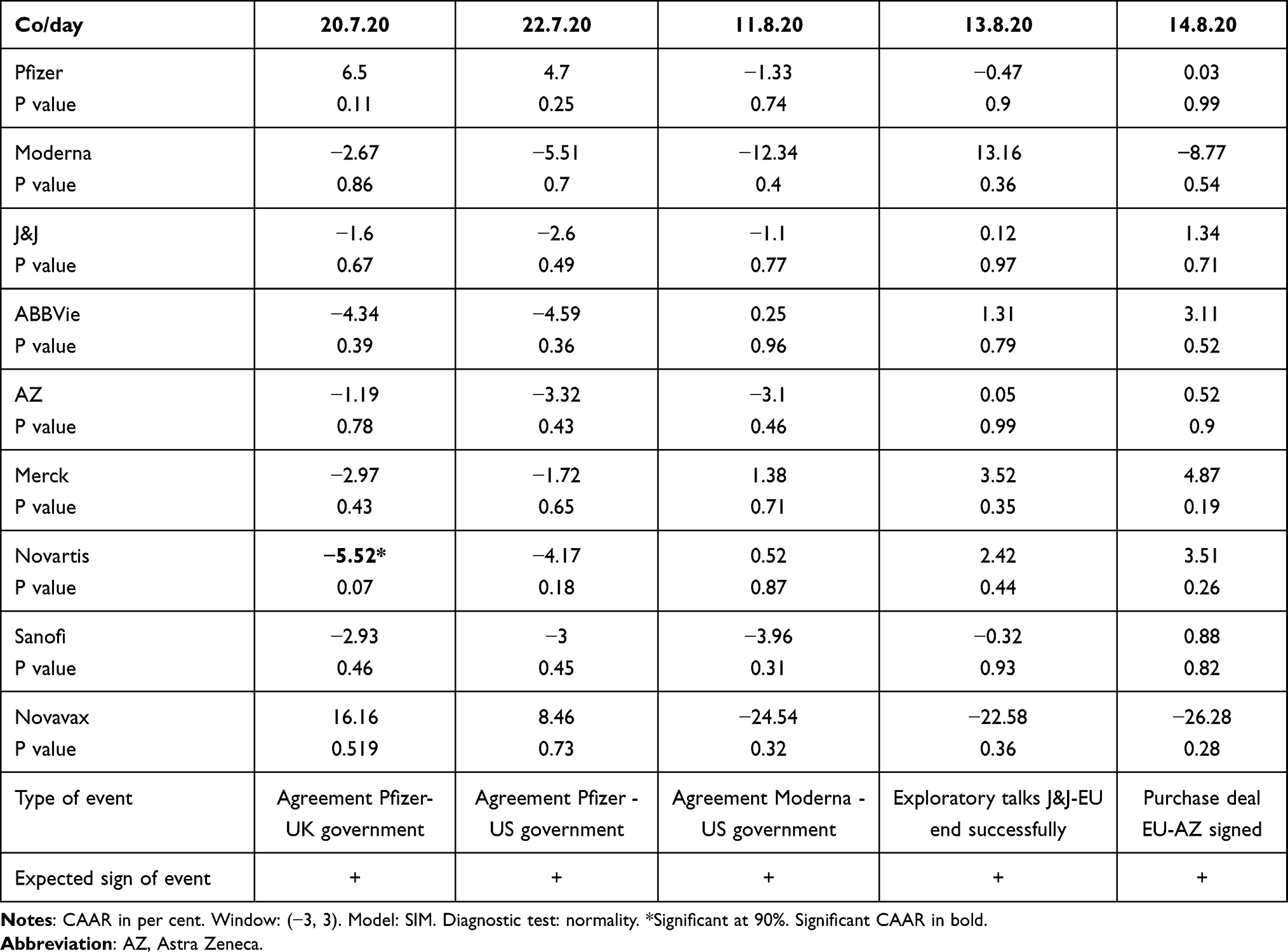

The large impact of the deal between Moderna and the EU around November 25 suggests the convenience of testing the impact of other similar deals between national authorities (or supranational, in the case of the European Union) and vaccine developers. Within the framework of the fight against the pandemic, many governments designed and implemented strategies to ensure the availability of vaccines. Two prominent cases in this regard are US and the EU. In both cases, the authorities tried to increase the probabilities of success of several vaccine projects by helping finance the upfront costs of these undertakings through purchase agreements which entailed down payments to vaccine developers. Moreover, governments built a diversified portfolio of vaccines by negotiating deals with several developers in parallel. These conversations started rather early, during Spring-Summer of 2020, when clinical trials for vaccines were still in progress.

Table 6 details some results from the exploration of this issue. The table details the outcomes of five events, comprising agreements between Pfizer and the UK government, Pfizer and the US government, Moderna and the US government; J&J and the EU (in this case the event is that exploratory conversations end successfully, rather than an agreement in itself) and the EU and Astra Zeneca. Pfizer registers positive CAARS on the dates of approval of agreements with UK and US, but they are non-significant. The CAAR for Moderna on the day of the agreement of the deal with the US government is negative but non-significant. J&J and Astra Zeneca experience positive CAARs on the dates of agreements with the EU, but they are not significant either. We have analyzed other deals between authorities and vaccine developers without remarkable results. Summing up, there is some evidence suggesting that stock markets have welcomed these deals with positive demand for their assets (except in the case of Moderna). Abnormal returns, however, associated with these events are modest and not significant at conventional levels.

|

Table 6 CAARs, Biopharmaceutical Companies, Events Related to Government Purchase Agreements (July–August 2020) |

Figure 2, second panel, summarizes the aggregate effects of events associated with vaccine developments. According to Figure 2, Novavax profited from both sets of events, but much more during the first period. In the second period, the stock only got a positive CAAR once, when results from its own vaccine were announced. Moderna also profited in both periods, but more in the second. Pfizer registered a positive impact of 18.75% in the second period. J&J experienced a slightly negative effect in the second period and a net effect of 0. The impact for Astra Zeneca was −20%. The rest of the companies underwent virtually no impact.

Robustness

We have checked the robustness of these results along several dimensions. The first of these dimensions is the estimation window. Our baseline exploration employs an estimation window starting on June 6, 2019. We have redone the estimations with a longer estimation window, which starts five months in advance, at the beginning of 2019 (January 2 because there was no stock market activity on January 1). Results are shown in Appendix 5, in Table A5.a for the events related with the COVID-19 expansion and in Table A5.b for events linked to the vaccines development. Results are very similar to those obtained with the initial estimation window. The main difference is that Moderna and Novavax get with this procedure slightly larger CAARs than before.

Second, we have redone the empirical exercise models assuming alternative models to estimate the expected returns in Equation (2) above.33

One of these models is the Market Adjusted Model. This model obtains the predicted return by means of the equation

Another widely used model is the Constant Expected Return Model or Historical Mean Model.34 Under this specification, the expected return is given by the historical mean return over the estimation window.

Results under these alternative specifications are detailed in Table A6 in Appendix 6 for the COVID-19 expansion announcements and in Table A7 in Appendix 7 for news about vaccine developments.

The fundamental messages from the baseline specification carry over when alternative models are employed. The main difference concerns the approval of the Pfizer COVID-19 vaccine. Under the baseline model the Pfizer stock suffered on that date a negative CAAR of 8.5%, significant at the 95% level. Under the alternatives, the CAAR on that date is positive, of 9% according to the MAM model and of 8.25% according to HMM, although in this last case the estimated CAAR is only marginally significant (p. value of 0.108). Anyway, it seems more plausible for Pfizer to have experienced a positive than a negative CAAR on the date of approval of the vaccine.

Finally, we detail in Table A8 in Appendix 8 the betas corresponding to the estimations from the baseline model for the COVID-19 expansion events. They have been estimated by two procedures, OLS and Huber robust regression (this last procedure is used to minimize the impact of potential outliers, following a common practice in recent literature). Both sets of results are displayed in panels a and b, respectively, of Table A8. Two features of this exercise stand out. First, most of the firms in our sample exhibit average beta coefficients less than 1, implying that their stock is less volatile than the market. Exceptions are Moderna and Novavax, with 1.13 and 1.16, respectively, according to the Huber estimation in panel b of table. This is consistent with their relatively small size, which attracts investors looking for high returns and willing to take more risk. The beta coefficient for AbbVie is 1 according to OLS, but slightly less than 1 (0.92) when the robust regression is estimated.

Second, the correlation coefficient among both sets of estimators is quite high for all firms (excluding Novavax) and equal to 0.972. When Novavax is included in the computation, the pairwise correlation coefficient drops to 0.538. This suggests that outliers are only a potential concern in the case of Novavax. Finally, our estimated beta coefficients are consistent with those obtained from financial information websites and from other contributions, thus lending countenance to our findings.35

Results and Discussion

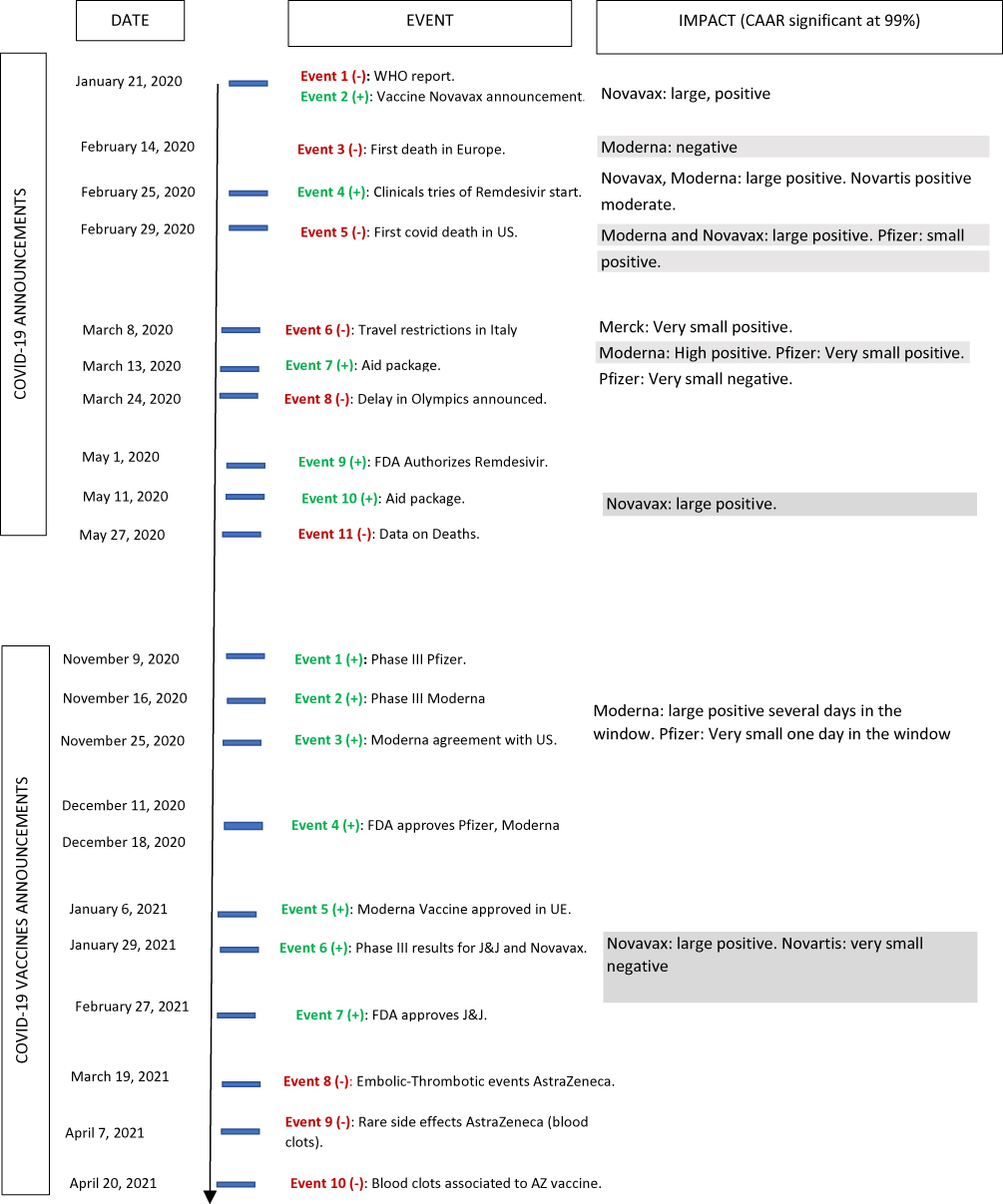

Figure 3 summarizes the findings from our event analysis. As Figure 3 conveys, our results imply that the reaction of the stock markets to news about the pandemic or the vaccines is mainly restricted to Moderna and Novavax and, to a smaller degree, Pfizer.

|

Figure 3 Summary of findings of Event Analysis for COVID-19 announcements and COVID-19 vaccines announcements. Notes: Events conveying bad news are highlighted in red, while those entailing good news are highlighted in green. |

Studies about the pharmaceutical sectors in other countries, such as India13 or Vietnam14 suggest some negative reactions associated to event 1 (publishing of the WHO report). The news linked to event 8 (delay of the Olympics) had also a negative impact in the markets of a group of countries. The extrapolation of these results should be made with caution, though, because the samples are different (the whole pharmaceutical sector in the first case versus a sample made up of COVID-19 vaccines developers and some other companies in our investigation). Similar reactions to this type of COVID-19 news were observed for stock prices in other industries.7,8,10 Phuong attributes the negative market sentiment to supply hurdles affecting key raw materials;14 Yu et al suggest that risk contagion in capital markets is associated with interruptions and difficulties in international trade.4 These circumstances did not disrupt the production of COVID-19 vaccines, however, whose dependence from raw materials is small.

Likewise, Varma et al and Liu et al find abnormal returns linked to the lockdown for a sample of pharmaceutical companies, which may be associated with the positive expectations that the development of vaccines generated in the short term.9,12,15 We only found a very small reaction for Merck because of mobility restrictions around our event 6 of the first subperiod. Sun et al argue that the pandemic generated a negative feeling of anxiety associated with uncertainty, which induced massive volatility of stock returns for companies of different sectors and idiosyncrasies.36 Nonetheless, studies on the pharmaceutical sector, including ours, suggest that the reaction to COVID-19 announcements maybe weaker for this industry.37 This may be due to the fact that at the beginning of the pandemic pharmaceutical companies could be perceived as a safe investment.36 All the above confirms that the stock market reaction to the events was not as intense as one might expect.

As discussed above, the large impact of news on Moderna and Novavax may be related to the fact of their being smaller companies and operating with a less diversified portfolio, which implies a larger exposition to the outcomes of vaccine development projects. It is also possible that they have attracted investment looking for a combination of high returns/high risk assets. Larger companies exhibited more diversified activity, and therefore the positive news about COVID-19 vaccines were interpreted with less euphoria and even with caution.

As Table 5 conveys, several events associated with the main COVID-19 vaccine announcements had some positive impact on Pfizer and a considerable positive effect on Moderna. These events are the end of Phase III trials, the FDA authorization and the agreement between Moderna and EU for the deliverance of a large number of vaccine doses.

The approval of the Moderna vaccine for the EU on January 6, 2021, did not impact Moderna, according to Table 5. The same happened regarding the FDA approval of the J&J vaccine of February 2021. On January 29 J&J and Novavax announced the end of their Phase III trials. This had no effect on J&J, although Astra Zeneca, a competitor, registered a negative CAAR of 7.68%. However, it prompted a positive and significant CAAR of almost 72% in Novavax. Finally, in March 19 the European regulatory agency announced that the Astra Zeneca vaccine caused embolic effects; on April 7, though, a committee from this agency concluded that these effects were regarded as rare. None of them impacted the Astra Zeneca vaccine significantly, probably because this firm attracted less interest from investors since its vaccine was not marketed in the US.

We did not find comparable studies regarding the impact of COVID-19 vaccine announcements on the share price of vaccine developers, and therefore we cannot discuss our results in the light of other contributions.

Several policy implications follow from this analysis. First, our results suggest that the markets have approved the swift and coordinated strategy from national and supranational authorities to fight the pandemic. This strategy has translated into different set of measures: financial support for vaccine developers, construction of a diversified vaccine portfolio with sufficient stock to handle the vaccination of high percentages of the population, simplification of the procedures necessary to obtain approvals from regulatory agencies, among others. It is feasible to reduce and streamline procedures and protocols when it is urgent, after a careful consideration of potential benefits and risks.38 Furthermore, these lines of action have been reinforced by financial markets by channeling additional funds to promising projects.

Second, some groups have been quite successful over the past three years expanding anti-vaccination claims (amplified by social networks);39 they have questioned the efficacy of vaccines often arguing that vaccines are mainly a source of huge profits by pharmaceuticals. It is beyond the scope of this paper to discuss whether COVID-19 vaccines are effective or not. What our findings suggest, though, is that the design and production of these remedies does not entail automatically large and sustainable gains for the developers, according to the behaviour of the stock prices of pharmaceutical companies over the recent past. These insights may be useful for policymakers, national health systems and organizations when striving to build trust in health policies, in particular when promoting vaccination campaigns among citizens.

Third, our results suggest that financial markets correctly evaluate information about pharmaceutical advances in the medium run. Analysts and investors can recognize those firms with more solid results. They are particularly sensitive to Phase III results (as already stressed by the literature) and to main agreements between producers and with public institutions. Hence some companies may experience large increases in stock prices. These effects are larger in the case of small firms, which can be seen as high profit, high risk, investments and hence more prone to short-term opportunistic behaviour. Ultimately though the market corrects these high expectations if they do not materialize in a reasonable span of time, as the case of Novavax shows. In parallel, investors keep an open mind toward small companies if they are successful and sustain these efforts with a surge in the demand for their stocks, as the example of Moderna suggests. Policymakers should try to warrant the sound operation of financial markets, hence the importance of economic considerations in order to address health alert situations, such as that produced by COVID-19.

It is not easy to envisage future trends for the COVID-19 vaccine developers analyzed in the paper. So far the FDA has approved the Pfizer, Moderna and J&J vaccines (but not the Astra Zeneca) and provided an emergency use authorization for Novavax in July 22. The European Medicines Agency has issued standard marketing authorizations for the Pfizer, J&J, Moderna and Astra Zeneca vaccines, whereas Novavax has received a conditional marketing authorization. The Johnson and Johnson COVID-19 vaccine does not seem to have been very successful in achieving a large market share in US or in the European Union.

Forecasts suggest that the demand for COVID-19 vaccines will decrease during next years. The gradual reduction in the demand for the COVID-19 vaccines, together with the traditional complexities associated with the vaccine sector (difficult scalability, non-linear production costs, uncertain demand, among others), suggest that it is not easy to identify large winners from this drug. A full analysis of the total profits generated by the COVID vaccines for drug developers is outside the scope of this paper, but may be an interesting topic for further research. Our research provides a preliminary and partial exploration of this topic. Hence further analysis striving to shed light on this issue will be welcomed.

Concluding Remarks

This paper analyses the reaction of the US stock market to different sets of news about the COVID-19 pandemic and vaccine development. Our results suggest that, except for Novavax and Moderna, biopharmaceutical firms did not register large abnormal results due to announcements related to the expansion of the pandemic in its first five months.

Regarding news related to the development of vaccines, we find that positive news about Phase III results impacted somehow the share prices of Pfizer, Moderna and Novavax; this effect was not detected for Johnson and Johnson. News about the order of 80 billion doses of vaccine made to Moderna by the EU entailed big positive CAARs for Moderna. Communications from the European Medicine Agency, instead, have not affected US stock markets.

The clear winner from the COVID-19 pandemic in terms of abnormal positive returns has been Moderna. Novavax was also able to generate high expectations and attract investors at the beginning of the pandemic, when the firm announced a preliminary engagement with the COVID-19 vaccine, but real advancements came too late, probably because of the lack of previous expertise with the manufacture of this product; as a consequence, gains in the share value gradually vanished. Pfizer has also experienced an increase in their share values, although more moderate.

These results may also be useful for financial institutions, funds and company managers from biopharmaceutical firms. Announcements related to successful Phase III clinical trials associated with biopharmaceutical products seem to increase the interest of investors in the shares of the company, driving up the price. In contrast, promising projects which do not materialize into sales in a reasonable time span may attract investors for a while but eventually shareholders look for alternatives in other companies.

Acknowledgments

This paper is based on a thesis published in http://e-spacio.uned.es/fez/view/tesisuned:ED-Pg-EcoyEmp-Rfdiaz on March 21, 2023.

Disclosure

The authors report no conflicts of interest in this work.

References

1. Piñeiro-Chousa J, Lopez-Cabarcos MA, Quiñoá-Piñeiro L, Pérez Pico A. US biopharmaceutical companies’ stock market reaction to the COVID-19 pandemic. Understanding the concept of the ‘paradoxical spiral’ from a sustainability perspective. Technol Forecast Soc Change. 2022;175:121365. doi:10.1016/j.techfore.2021.121365

2. Baker SR, Bloom N, Davis SJ, Kost KJ, Sammon MC. The unprecedented stock market impact of COVID-19. National Bureau of Economic Research Working Paper Series; 2020:26945.

3. Zaremba A, Kizys R, Aharon DY, Demir E. Infected markets: novel coronavirus, government interventions, and stock return volatility around the globe. Finance Res Lett. 2020;35:101597. doi:10.1016/j.frl.2020.101597

4. Yu H, Chu W, Ding YA, Zhao X. Risk contagion of global stock markets under COVID‐19: a network connectedness method. Accoun Finance. 2021;61(4):5745–5782. doi:10.1111/acfi.12775

5. Donadelli M, Kizys R, Riedel M. Dangerous infectious diseases: bad news for main street, good news for Wall street? J Financial Markets. 2017;35:84–103. doi:10.1016/j.finmar.2016.12.003

6. World Health Organization. Global Vaccine Market Report. Geneva: World Health Organization; 2022.

7. Chatjuthamard P, Jindahra P, Sarajoti P, Treepongkaruna S. The effect of COVID‐19 on the global stock market. Accoun Finance. 2021;61(3):4923–4953. doi:10.1111/acfi.12838

8. Baek S, Lee KY. The risk transmission of COVID-19 in the US stock market. Appl Econ. 2021;53(17):1976–1990. doi:10.1080/00036846.2020.1854668

9. Cao KH, Li Q, Liu Y, Woo CK. Covid-19’s adverse effects on a stock market index. Appl Econ Lett. 2021;28(14):1157–1161. doi:10.1080/13504851.2020.1803481

10. Xu L, Chen J, Zhang X, Zhao J. COVID‐19, public attention and the stock market. Accoun Finance. 2021;61(3):4741–4756. doi:10.1111/acfi.12734

11. Ozik G, Sadka R, Shen S. Flattening the illiquidity curve: retail trading during the COVID-19 lockdown. J Financial Quant Anal. 2021;56(7):2356–2388. doi:10.1017/S0022109021000387

12. Liu H, Wang Y, He D, Wang C. Short term response of Chinese stock markets to the outbreak of COVID-19. Appl Econ. 2020;52(53):5859–5872. doi:10.1080/00036846.2020.1776837

13. Mittal S, Sharma D. The impact of COVID-19 on stock returns of the Indian healthcare and pharmaceutical sector. Australas Account Bus Finance J. 2021;15(1):5–21. doi:10.14453/aabfj.v15i1.2

14. Phuong LCM. How COVID-19 affects the share price of Vietnam’s pharmaceutical industry: event study method. Entrepreneurship Sustain Issues. 2021;8(4):250. doi:10.9770/jesi.2021.8.4(14)

15. Varma Y, Venkataramani R, Kayal P, Maiti M. Short-term impact of COVID-19 on Indian stock market. J Risk Finance Manage. 2021;14(11):558. doi:10.3390/jrfm14110558

16. Díaz RF. El sector farmacéutico: eficiencia, rentabilidad y COVID-19 [Dissertation]. Madrid: Universidad Nacional de Educación a Distancia; 2023.

17. Goodell JW. COVID-19 and finance: agendas for future research. Finance Res Lett. 2020;35:101512. doi:10.1016/j.frl.2020.101512

18. Hwang TJ. Stock market returns and clinical trial results of investigational compounds: an event study analysis of large biopharmaceutical companies. PLoS One. 2013;8(8):e71966. doi:10.1371/journal.pone.0071966

19. Perez-Rodríguez JV, Valcárcel BG. Do product innovation and news about the R&D process produce large price changes and overreaction? The case of pharmaceutical stock prices. Appl Econ. 2012;44(17):2217–2229. doi:10.1080/00036846.2011.562172

20. De Schrijver J. Analysis of stock market reactions to FDA and EMEA announcements [dissertation]. Ghent: Ghent University; 2013.

21. Heyden KJ, Heyden T. Market reactions to the arrival and containment of COVID-19: an event study. Finance Res Lett. 2021;38:101745. doi:10.1016/j.frl.2020.101745

22. Ichev R, Marinč M. Stock prices and geographic proximity of information: evidence from the Ebola outbreak. Int Rev Financial Anal. 2018;56:153–166. doi:10.1016/j.irfa.2017.12.004

23. Haroon O, Rizvi SAR. COVID-19: media coverage and financial markets behavior—a sectoral inquiry. J Behav Exp Finance. 2020;27:100343. doi:10.1016/j.jbef.2020.100343

24. Alam MM, Wei H, Wahid AN. COVID‐19 outbreak and sectoral performance of the Australian stock market: an event study analysis. Aust Econ Pap. 2021;60(3):482–495. doi:10.1111/1467-8454.12215

25. Behera C, Rath BN. The COVID-19 pandemic and Indian pharmaceutical companies: an event study analysis. Bulletin Monet Econ Banking. 2021;24:1–14. doi:10.21098/bemp.v24i0.1483

26. Alcaide González MA, De la Poza Plaza E, Guadalajara Olmeda N. How has the announcement of the Covid-19 pandemic and vaccine impacted the market? Econ Res Ekon Istraz. 2022;35(1):5615–5631. doi:10.1080/1331677X.2022.2033129

27. Zhang LC. Event study: the influence of COVID-19 research and development news on pharmaceutical and biotech companies. Working Paper. Ann Arbor: University of Michigan; 2021.

28. Casault S, Groen AJ, Linton JD. Improving value assessment of high-risk, high-reward biotechnology research: the role of ‘thick tails’. N Biotechnol. 2014;31(2):172–178. doi:10.1016/j.nbt.2013.12.001

29. Brenner M. The sensitivity of the efficient market hypothesis to alternative specifications of the market model. J Finance. 1979;34(4):915–929. doi:10.1111/j.1540-6261.1979.tb03444.x

30. Sorokina N, Booth DE, Thornton JH Jr. Robust methods in event studies: empirical evidence and theoretical implications. J Data Sci. 2013;11:575–606. doi:10.6339/JDS.2013.11(3).1166

31. Armitage S. Event study methods and evidence on their performance. J Eco Survey. 1995;9(1):25–52. doi:10.1111/j.1467-6419.1995.tb00109.x

32. Yahoo finance. Homepage on the Internet; 2023. Available from: https://www.yahoo.com/author/yahoo-finance/.

33. Kothari SP, Warner JB. Econometrics of event studies. In: Espen Eckbo B, editor. Handbook of Empirical Corporate Finance. Amsterdam: Elsevier; 2007:3–36.

34. Brown SJ, Warner JB. Using daily stock returns: the case of event studies. J Financial Eco. 1985;14(1):3–31. doi:10.1016/0304-405X(85)90042-X

35. Theodossiou AK, Theodossiou P, Yaari U. Beta estimation with stock return outliers: the case of US pharmaceutical companies. SSRN Electro J. 2009. doi:10.2139/ssrn.1410371

36. Sun Y, Wu M, Zeng X, Peng Z. The impact of COVID-19 on the Chinese stock market: sentimental or substantial? Finance Res Lett. 2021;38:101838. doi:10.1016/j.frl.2020.101838

37. He P, Sun Y, Zhang Y, Li T. COVID–19’s impact on stock prices across different sectors—An event study based on the Chinese stock market. Emerg Mark Finance Trade. 2020;56(10):2198–2212. doi:10.1080/1540496X.2020.1785865

38. Kesselheim AS, Darrow JJ, Kulldorff M, et al. An overview of vaccine development, approval, and regulation, with implications for COVID-19: analysis reviews the food and drug administration’s critical vaccine approval role with implications for COVID-19 vaccinesHealth. Affairs. 2021;40(1):25–32.

39. Wouters OJ, Shadlen KC, Salcher-Konrad M, et al. Challenges in ensuring global access to COVID-19 vaccines: production, affordability, allocation, and deployment. Lancet. 2021;397(10278):1023–1034. doi:10.1016/S0140-6736(21)00306-8

40. OECD. Data; 2023. Available from: https://data.oecd.org/.

41. Tinari S, Riva C. Covid-19: whatever happened to the Novavax vaccine? BMJ. 2021;375. doi:10.1136/bmj.n2965

42. Pharmaceutical Technology. homepage on the the internet. Available from: https://www.pharmaceutical-technology.com/features/top-ten-pharma-companies-in-2020/.

43. World Health Organization (WHO). Coronavirus disease (COVID-19): vaccines; 2022b. Available from: https://www.who.int/news-room/questions-and-answers/item/coronavirus-disease-(covid-19)-vaccines.

{kind=link}