Traders work on the floor of the New York Stock Exchange (NYSE) in New York City, U.S., September 26, 2023. REUTERS/Brendan McDermid/File Photo Acquire Licensing Rights

NEW YORK, Oct 11 (Reuters) – Technical and seasonal indicators that investors use to gauge the U.S. stock market’s health show it may be time to buy, though upcoming inflation data and the third-quarter earnings season could still throw Wall Street a curveball.

The S&P 500 has slid about 5% since reaching its late-July high, but so far this month the benchmark index has rebounded. Technical analysts see a case for the rally to continue, pointing to indicators showing stocks may be oversold and historical evidence showing year-end is typically a strong period for equities.

There remain plenty of reasons for caution. Some analysts are concerned that a small group of megacap stocks has led the S&P 500’s gains this year, muddying the case for a sustained rally in the broader market.

Investors are also worried about the Federal Reserve interest rate trajectory, which could be influenced by Thursday’s U.S. consumer price report. Another wild card could be third-quarter earnings season which kicks off on Friday and should help show whether companies can justify valuations that have swelled this year.

“The preponderance of evidence supports the case for a year end rally,” said Ed Clissold, chief U.S. strategist at Ned Davis Research. However, he said, “it remains to be seen if the market has begun a multi-month topping process.”

Analysts were encouraged by the positive reaction from stocks in the face of both a surge in monthly jobs that raised concerns about a still too-hot economy, and the deadly attacks in the Middle East.

The S&P 500’s ability to rise in the aftermath of those events “leads me to believe that a lot of negative information had been priced into the market,” Clissold said.

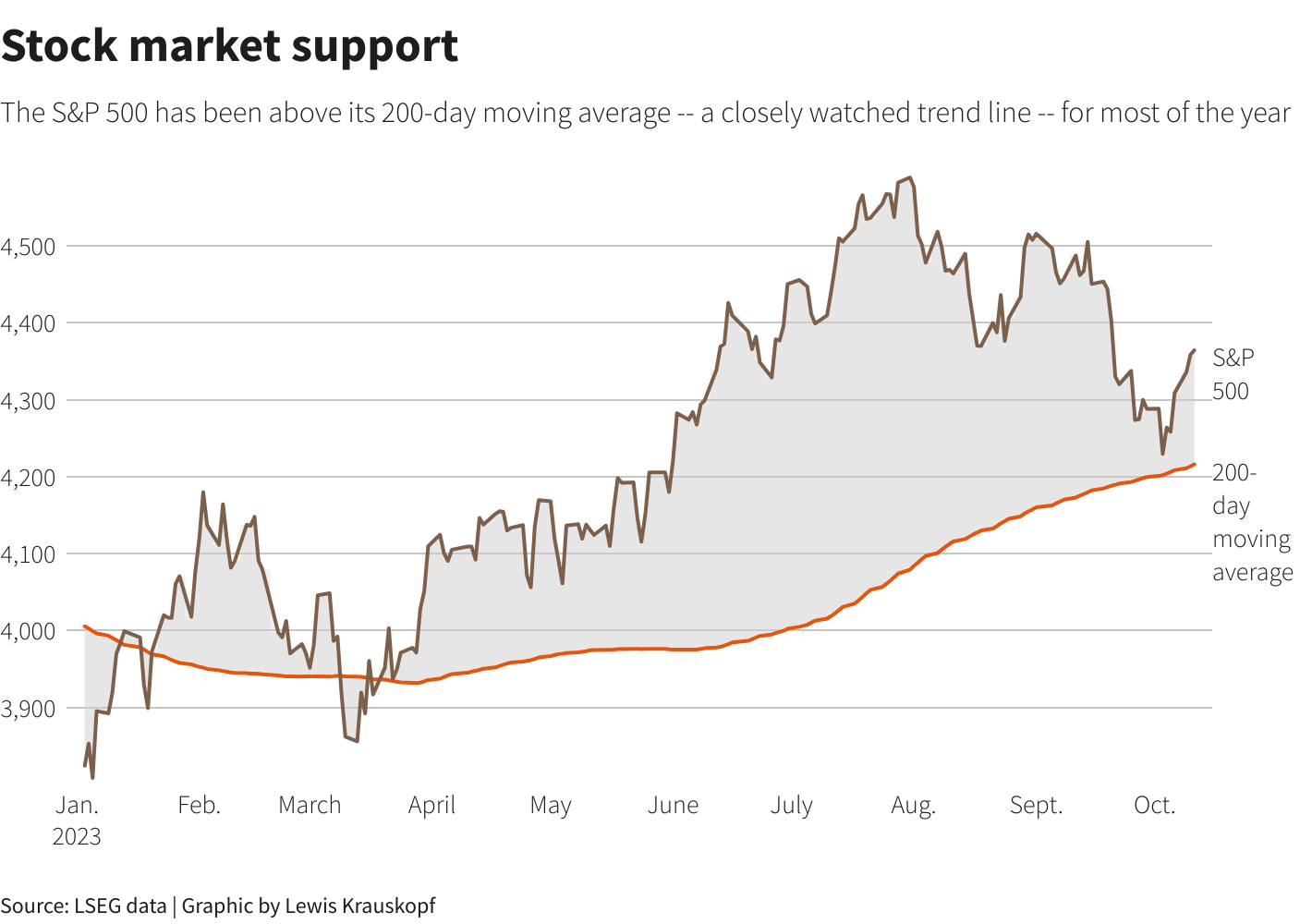

One positive sign is that the S&P 500 has remained above the closely watched 200-day moving average, a trend line that can act as support. The S&P 500 was last about 3.5% above its 200-day moving average.

Adam Turnquist, chief technical strategist for LPL Financial, pointed out that the index remained above the 200-day moving average while more than one-fifth of the index’s stocks were in an oversold status, in which relative strength readings indicate a positive price correction could be coming.

Those two factors have occurred together only 14 times since 1990. In 12 of those times the S&P 500 was higher six months later, Turnquist said.

Stocks have tended to perform well at year end — with November and December logging the second and third-biggest average S&P 500 monthly gains — though this year the trends may portend even more favorably.

In the 14 instances when the S&P 500 has gained at least 10% through July and then declined in August, as it did this year, the index has increased every time over the last four months of the year, according to Ned Davis Research. The average gain in those instances has been 10%.

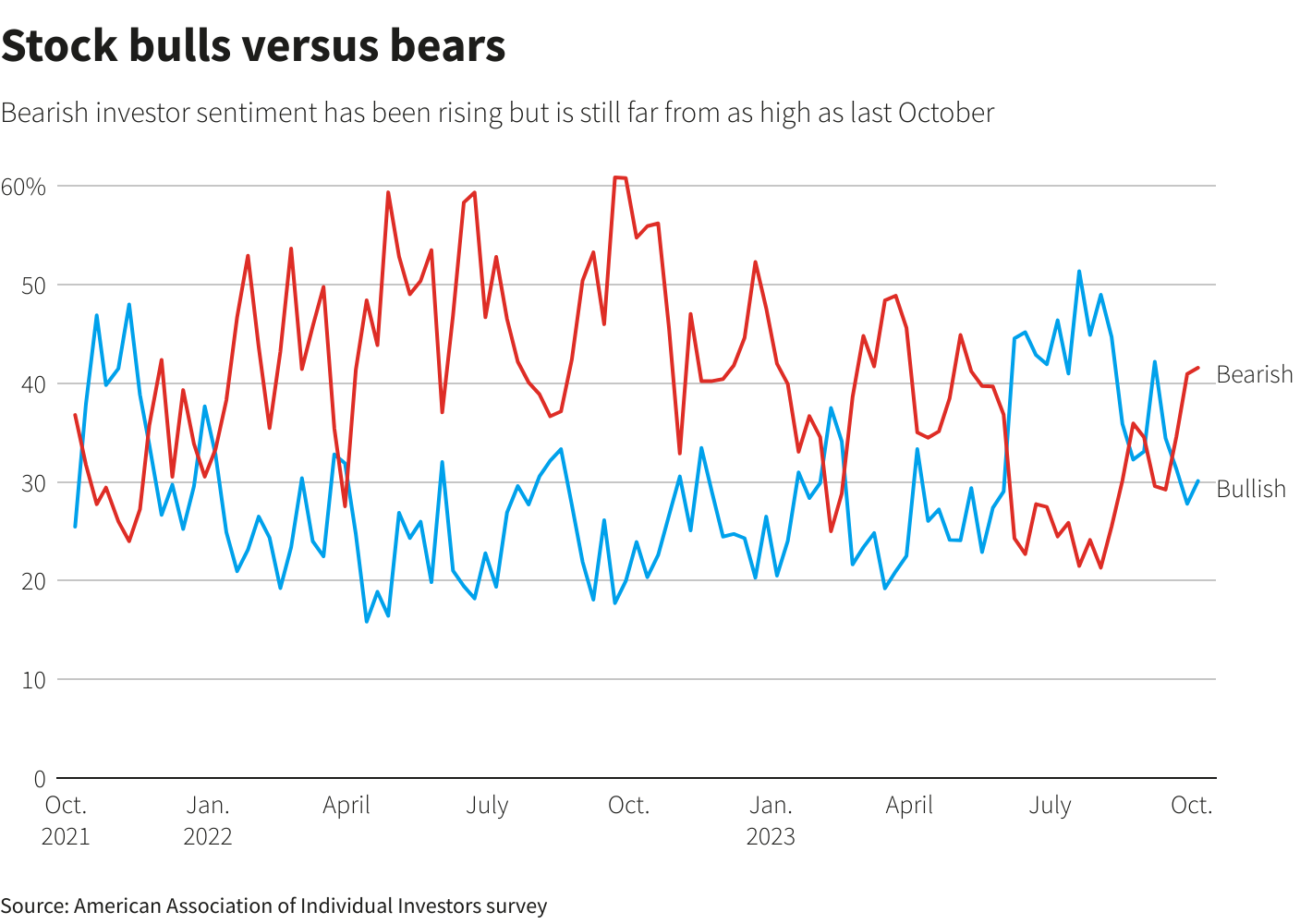

Market sentiment has turned more negative with the latest stock slide, with 41.6% of investors bearish and 30.1% bullish in the latest American Association of Individual Investors (AAII) weekly survey.

But rising bearish sentiment often works as a contrary indicator for stocks, suggesting plenty of investors are on the sidelines who could buy on positive developments.

Yet the picture is not as clear cut as last year, when a brutal market selloff saw stocks fall to a nearly two-year low in mid-October. That was followed by a 28% rally in the S&P 500 through late July of this year.

Indicators such as the AAII do not yet suggest the pessimistic sentiment is “excessive”, which would be more clear if the spread between bulls and bears was wider, according to Willie Delwiche, investment strategist at Hi Mount Research.

For example, bearish sentiment stood at 56% in the AAII survey last October.

Further, notes Delwiche, stock market breadth has been weak. The combined weekly number of new 52-week lows on the NYSE and Nasdaq has topped the amount of new 52-week highs for nine straight weeks, he said.

Even if the market rebounds in the near term, Delwiche said, “if you don’t have that regime shift where you get back to more stocks making new highs than new lows, then it’s an oversold bounce that doesn’t go anywhere.”

Reporting by Lewis Krauskopf; Editing by Ira Iosebashvili and David Gregorio

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}