The American labor movement brought us Labor Day, the weekend, employer-sponsored health coverage, and the right to retire. In the late 1800s, industrialization had dramatically increased the lifespan of citizens in nations where it took root, like America. Suddenly workers were living a lot longer than 30 or 40 years, and many needed support after hard physical jobs took a toll over decades. Labor Day and retirement might not seem linked, but they’re both part of the long history of workers’ rights activism.

Since early days of retirement planning, setting up employees for retirement has been especially effective when it involves partnership and mutual contribution from the employee and employer. To mark Labor Day, we want to chronicle the history of retirement planning in America, and show how it’s evolved to the modern employer-sponsored system that many Americans use to save for retirement.

Early History

After the Civil War, America’s economy shifted from rural and agrarian to urban and commercial. Industries like banking, railroads, and manufacturing drove the economy, with small businesses leading the way.1 The first corporate pension in the U.S. was established by the American Express Company in 1875. At Amex, to qualify for a pension you had to be over the age of 60, have been employed there for at least 20 years, and have been recommended for retirement by a manager, with that retirement approved by the board of directors.2

However, the Baltimore and Ohio railroad came up with a different solution in 1880, the first retirement plan that drew from both employee salaries and employer contributions to build the retiree’s savings.3 The distinction between a pension and other types of retirement plans became more clear; pensions were doled out by the company at-will, while the retirement plan gave the individual a stake in the game. The foundation for the 401(k) was being laid almost 100 years before the first one would be offered by an employer.

In the case of many pensions, it wasn’t just the amount that was inflexible, it was also the retirement date. The enforcement of mandatory retirement became more common as the 20th century boomed. As a younger workforce became necessary, many business owners were uncomfortable simply turning loyal older employees out into the street. By 1926, more than 200 private pension plans helped cushion the transition out of the workforce for older employees. In the early 1920s, 84% of railroad workers were covered by defined benefit plans that their employers could alter or terminate at any time. It wasn’t until the Great Depression, when such cuts were necessary, that it became clear a more supportive system might be needed to keep the elderly and retired out of poverty.4

Great Depression and Social Security

Between 1900 and 1930, the average lifespan increased by 10 years, the biggest single-generation leap in history.5 When the stock market crashed in 1929, there were more people alive than ever before to feel the effects as unemployment rose to 25%.6 Many states took individual action to try and provide some kind of social welfare support, but it wasn’t until President Franklin D. Roosevelt took office in 1932 that the conversation shifted from one of regional charity to one of federally-structured retiree contribution.

The Social Security Act passed in 1935 set up the framework of our modern Social Security system: American workers would pay tax out of every check to contribute to a fund, and in their old age, receive an income from the fund. “We have tried to frame a law which will give some measure of protection to the average citizen and to his family against the loss of a job and against poverty-ridden old age,” said President Roosevelt upon signing the Act into law. Today, concerns about the future of the fund after a surplus is expended have many questioning the role of social security in their retirement planning.

WWII and Pensions

Just when the public and private sectors had sorted out how to take care of older retirees, America became involved in World War II and the effort of every single able-bodied citizen was needed. In 1940, only 12% of jobs offered a pension, but by the end of the war in 1945, that had risen to 17%. As millions of young people returned from the front and needed employment, pensions were one key way for employers to attract the best talent returning to the workforce. Pensions gave incentives to workers to spend their whole career with one company, while providing the added benefit of ensuring they would stay self-sufficient into old age, and this system persisted for decades.7 However, just like with the invention of Social Security, other social and economic changes lay on the horizon that would further change the American retirement system.

Modern Retirement Planning

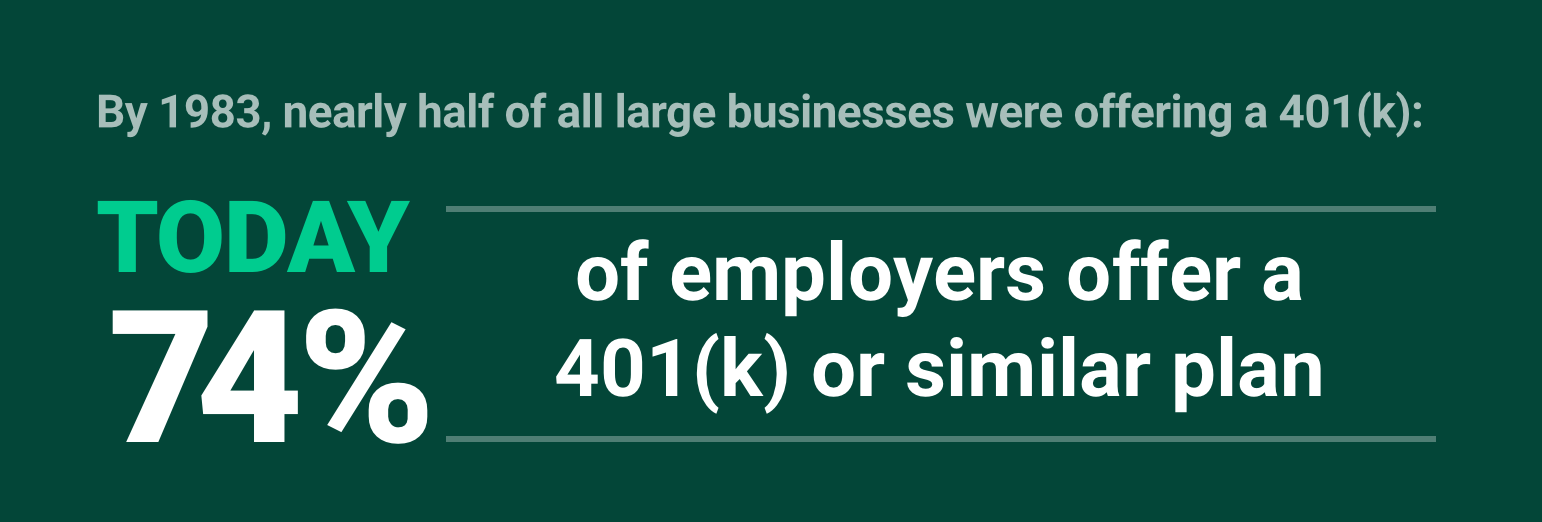

The Revenue Act of 1978 officially established Internal Revenue Code (IRC) Sec. 401(k), which ruled that employees would not be taxed on the portion of their income that they chose to defer into retirement funds. Many employers had simply been sponsoring programs to help employees save after their taxes, but this option allowed the employer to lower their taxable income, while the employee got to save more money today to invest and grow. By 1983, surveys showed that nearly half of all large businesses were offering a 401(k) plan, or at least considering one. Some even added 401(k) options to profit sharing and stock bonus plans, or added an employer match option to incentivize saving.8

An average person who entered retirement in 2010 or later can expect to receive $180,000 or more in Medicare benefits during the course of their retirement, though the same worker likely only contributed around $60,000 in taxes to the program during their career.9

A study by Towers Watson reveals that one impact of this innovative financial product is the almost total disappearance of the pension plan. Their study found that from 1998 to 2013, the number of Fortune 500 companies offering traditional defined benefit plans dropped 86%, from 251 to only 34. In the battle of pension vs 401(k) savings, today’s economy tends toward the 401(k). This puts employees in the driver’s seat of their own future, but can also mean many face retirement unprepared if they don’t plan adequately. Today, one-in-three Americans has no retirement savings—42% of Millennials (18 to 34), 30% of Gen-X’ers (35 to 54), and 29% of Baby Boomers (55 and over).10

Recent pieces of legislation have tried to address this problem through plan features like automatic enrollment, where newly-eligible employees are automatically enrolled in the company 401(k) unless they formally opt out.11 Initiatives like these can often help employees overcome the gap between their actual ability to save and their perceived ability to save. Ted Benna is credited with conceiving of the idea for an employer match program, and when asked about the impact of the 401(k), he pointed to the increase in household thrift as one of the most positive results of these plans.12 However, if an employee is to be truly successful in making the most of their right to retire, it requires long-term planning and accountability to their goals.

While the ability to budget and save is a personal journey for each employee, today’s business owners can support them on this path by partnering with a 401(k) provider that offers financial planning support and a variety of investment options to help them reach their personal goals for retirement. Today’s Americans planning for retirement need financial education.13 Once employees see the impact small savings can have on their future, we find they’re suddenly engaged with the journey to a peaceful and well-funded retirement.

1http://www.thenexthill.com/a-brief-history-of-retirement-part-2.htm

2https://www.thebalance.com/the-history-of-the-pension-plan-2894374

3http://www.seattletimes.com/nation-world/a-brief-history-of-retirement-its-a-modern-idea/

4http://www.thenexthill.com/a-brief-history-of-retirement-part-3.htm

5https://www.infoplease.com/us/mortality/life-expectancy-age-1850-2011

6http://www.history.com/topics/great-depression

7http://www.huffingtonpost.com/don-mcnay/why-the-decrease-in-union_b_5740160.html

8https://www.ebri.org/pdf/publications/facts/0205fact.a.pdf

9https://www.fool.com/retirement/2016/06/05/heres-how-much-the-average-senior-will-receive-in.aspx

10http://time.com/money/4258451/retirement-savings-survey/

11https://www.ebri.org/pdf/publications/facts/0205fact.a.pdf

12https://www.marketplace.org/2013/06/13/sustainability/consumed/father-modern-401k-says-it-fails-many-americans

13http://www.politico.com/agenda/story/2016/08/americas-worsening-retirement-problem-000190

{kind=link}