Introduction and summary

In the past few years, both the U.S. and U.K. Treasury bond markets have required central bank bailouts due to investment strategies of nonbank financial intermediaries that went wrong. In the United States, hedge fund basis trades were a significant contributor to the Treasury market interest rate spike of March 2020, which ultimately led to large Federal Reserve purchases of Treasury securities and the restart and expansion of the asset-buying apparatus that was first implemented during the global financial crisis of 2007. In 2022, U.K. private pension funds using so-called liability-driven investment strategies were forced to sell U.K. government bonds, or gilts, in order to raise cash to meet margin calls. This created a sharp decline in the gilt prices, forcing the Bank of England to buy large quantities of gilts to prevent the pension funds from engaging in fire sales.

This report examines how the United States can draw on these lessons to reduce the fire sale risk that hedge fund trading poses to the Treasury market. It explains how highly leveraged basis trades were structured and why changing market conditions forced large-scale, disruptive sales that required Federal Reserve intervention. It shows why two avenues for limiting this risk—a proposed U.S. Securities and Exchange Commission (SEC) rule on Treasury trading and changes to capital requirements for very large banks—are likely to be inadequate. It then suggests how the Federal Reserve could use its authority over fixed-income trading platforms to reduce this risk.

Glossary of key terms

Nonbank financial intermediaries (NBFIs) are financial institutions that do not have banking licenses, are not subject to banking regulation, and do not have access to central bank liquidity facilities. They manage assets, provide credit, and provide other bank-like services. Insurance companies, asset managers, and hedge funds are examples.

Basis trades are trading positions intended to profit from differences between the current cash price of Treasuries and their futures price. In 2020, several hedge funds made large, leveraged cash purchases of Treasuries for cash, and simultaneously sold futures contracts for those same Treasuries. The price differences are usually small and measured in basis points—hundredths of a percentage point. In March 2020, margin calls on futures contracts made hedge fund positions unprofitable, forcing sales of Treasuries. Large-scale basis trades have since resumed.

Gilts are interest-bearing financial obligations of the U.K. government.

Liability driven investments (LDIs) are trading positions taken by U.K. insurance companies designed to hedge interest rate and inflation risk and increase income to cover liabilities. Borrowing, collateralized by holdings of “gilts,” was used to fund derivatives positions. In September 2022, changes in the market value of gilts and derivatives led to collateral and margin calls, forcing sale of gilts to raise cash.

A central counterparty (CCP) is an institution that acts as a seller to every buyer and as a buyer to every seller for all members, insuring members against counterparty losses by taking the position of the defaulted member, netting all payment obligations of a member across all cleared contracts into one CCP payment obligation. Risks are mutualized through a guarantee fund.

The Fixed Income Clearing Corporation (FICC) is a central counterparty for U.S. government securities and mortgage-backed securities, providing trade matching, clearing, risk management, and netting of trades. It is regulated by the U.S. Securities and Exchange Commission and the Federal Reserve.

Global systemically important banks (GSIBs) are banks whose failure could pose a threat to the international financial system. These banks are identified using a set of financial indicators determined by the Basel Committee on Banking Supervision, which is composed of banking supervisors from 28 jurisdictions. Eight large U.S. banks qualify as GSIBs.

Background

The events in the United States and United Kingdom saw NBFIs using high leverage—or significant levels of debt financing—to take large positions in government bonds. In the United States, hedge fund basis trades involved cash purchases of Treasuries matched to sales of Treasuries in futures markets; their design allows them to profit from small differences between cash and futures prices.1 The cash purchases were funded in large measure through repurchase, or “repo,” agreements,2 a form of collateralized short-term borrowing, often overnight, that allows an investor to hold a large Treasury position while putting up only a small percentage of the total value from their own funds. In the current repo market, repo loans average about 98 percent of the value of Treasury securities pledged as collateral.3 This means that a Treasury buyer needs only $2 to hold $100 in Treasuries. Hence, repo-financed positions can be highly leveraged, on the order of 50-to-1.

Hedge fund futures market positions were also highly leveraged. Central counterparties in the Treasury futures markets, such as the Chicago Mercantile Exchange, require buyers and sellers to post “margin”—that is, collateral equal to a share of contract values—in order to protect the exchange against the risk of nonperformance on the contracts.4 Margins are usually a small fraction of a contract value, allowing participants to take highly leveraged positions. However, they are adjusted as market conditions change, and adverse changes can lead to collateral calls.5

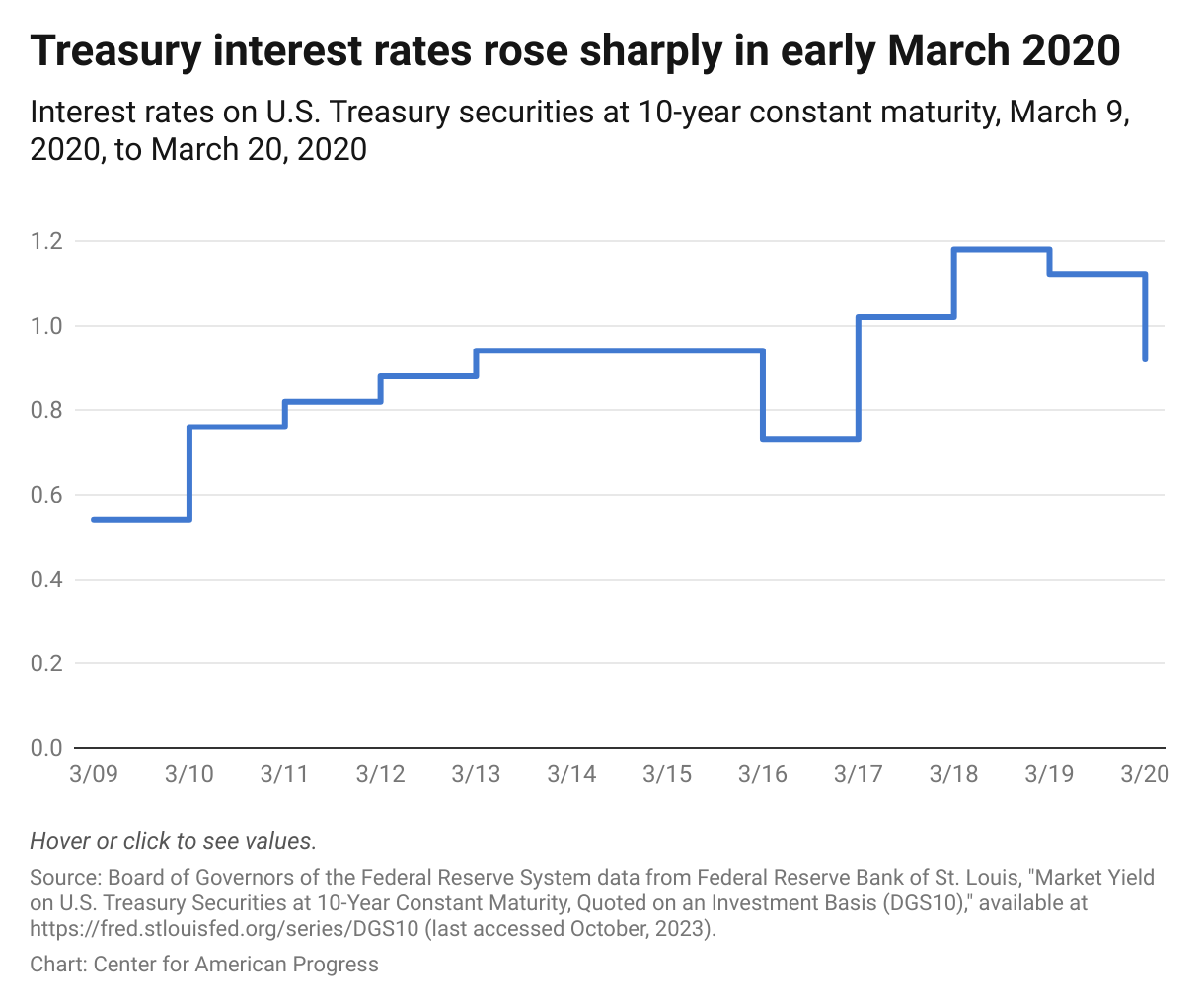

When financial markets reacted to the initial effects of the COVID-19 pandemic in March 2020, Treasury prices began to decline. The yield on the 10-year Treasury bond more than doubled between March 9 and March 18 (see Figure 1), and futures prices became more volatile. The hedge funds received margin calls on their forward contracts.6 As their positions became unprofitable, they sold an estimated $183 billion in Treasury securities in a very short period of time. This contributed substantially to a Treasury fire sale that caused a large interest rate spike. The Federal Reserve was forced to step in to limit the effects of the spike, ultimately making purchases of about $1 trillion.7

FIGURE 1

In the United Kingdom, pension funds used borrowing on gilts they owned and derivative contracts linked to interest rates to make leveraged investments.8 These LDI strategies were intended to increase pension funds’ return on assets and could have done so if interest rates had declined or held steady. However, in September 2022, when gilt rates began to rise, the funds experienced collateral calls on borrowing and margin calls on their derivatives positions and were forced to sell gilts to raise the needed cash.9 Their sales were large enough to lower gilt prices, raising rates and thereby increasing margin calls, which provoked additional sales.

These events show that even large, deep government bond markets—where assets are not subject to credit risk—can be destabilized when nonbank financial intermediaries’ strategies go wrong and produce fire sales. In both instances, NFBIs were forced to sell assets because lenders were making margin calls affecting leveraged positions. This is distinct from the financial crisis of 2007, when losses on mortgage-backed securities threatened the solvency of major banks and other financial institutions. Nonetheless, the impacts on both government bond markets were severe, forcing the Federal Reserve and the Bank of England to intervene to limit shocks to bond prices and threats to financial stability.10

It is important to note that both the Federal Reserve and the Bank for International Settlements recently have pointed to evidence indicating that leveraged hedge fund basis trades in Treasuries have returned to 2020 levels.11

NBFIs such as hedge funds are a potential source of large-scale market disruption that requires a solution

Nonbank financial institutions pose a fire sale risk to the Treasury market, as they use leverage to take very large positions that they can be forced to unwind rapidly when financial market conditions change. This risk can be mitigated if the Federal Reserve limits hedge fund leverage—for example, by using its Dodd-Frank authority over the central counterparties when large volumes of Treasuries are traded.

Although the Federal Reserve and the Bank of England dealt with fire sales and accompanying interest rate spikes by stepping in to buy their respective government debt, interventions such as these are undesirable. Repeatedly acting as a buyer of last resort for NBFIs—which are not required to meet any of the leverage, liquidity, or other regulatory standards applied to banks—will have the effect of increasing their risk-taking, as NBFIs will know that if things go bad, the public sector will help limit their losses. They will be given something equivalent to bank access to the Federal Reserve discount window, without any of the prudential regulation that reduces the need for banks to access it. This is moral hazard on steroids.

There is, however, a way to reduce the likelihood of fires sales of Treasuries by highly leveraged NFBIs such as hedge funds, and it can be achieved through a combination of existing Securities and Exchange Commission and Federal Reserve authorities. Some of the groundwork has already been laid by a proposed SEC rule.12 Among other things, this rule would require members of clearinghouses to clear all their secondary trades in Treasuries through those clearinghouses. Many broker-dealers currently clear at least some of their Treasury trades through the Fixed Income Clearing Corporation. If the rule were adopted, broker-dealer and interdealer brokers who use FICC would clear all their Treasury trades through FICC.

Requiring central clearing for Treasury trades could help limit fire sales by increasing the capacity of market participants to buy Treasuries. Use of a central counterparty would allow for netting of repo borrowing and lending, since the CCP becomes the counterparty for all trades. When, as in the case of bank broker-dealers, lending counts against leverage requirements, netting can allow for greater ability to buy.

The effect of netting can be substantial. By one recent estimate, the netting of primary dealer repo lending and borrowing on FICC increases dealer capacity by about 20 percent.13 However, it is not clear how much buying capacity would actually be increased by the central clearing requirement. Broker-dealers held $268 billion in Treasury debt in the second quarter of 2020, a historical peak value.14 (see Figure 2) If this amount were increased by one-fifth, it would increase capacity by approximately $54 billion. This is real money, but far from the $1 trillion that the Federal Reserve needed to deal with the 2020 fire sale. Moreover, banks already use FICC to clear Treasury trades, and increases in capacity will depend on how much business will now be shifted to the platform for clearing.

FIGURE 2

A potentially more consequential effect of clearing requirements is that all users would have to meet CCP risk requirements. These include both capital requirements for members and margin rules for trades. These conditions are designed to protect the clearinghouse in the event that a member defaults on obligations to a counterparty. This kind of risk mitigation is important, since problems at an important CCP can interfere with market functioning.

However, while these risk management conditions help preserve the functioning of FICC, they do not effectively mitigate the financial instability risk created by NBFIs such as hedge funds. Many hedge funds have access to central clearing via their relationships with prime brokerages located in banks. Members of FICC “sponsor” clients’ clearing, giving sponsored hedge funds access to other FICC members as repo counterparties. FICC is protected from direct loss by the “Sponsoring Member guarantees.”15 But the Treasury market, which is central to the operation of the world financial system, is not protected from fire sales by hedge funds, as the events in March 2020 illustrate.

The Federal Reserve ought to use its Dodd-Frank authority to mitigate hedge fund risks to the market for Treasuries

CCP risk management standards that take into account the stability risks of funding highly leveraged NBFIs could help prevent such events. The SEC does not appear to have the independent authority to require FICC or other CCPs to adopt such standards. However, FICC is a subsidiary of the Depository Trust and Clearing Corporation, which has been designated as a systemically important financial market utility by the Financial Stability Oversight Council. Under Sections 805(a) and 805(b) of the Dodd-Frank Act Wall Street Reform and Consumer Protection Act, the Federal Reserve may prescribe risk management standards for such utilities in order to promote financial stability.16 An obvious application of that authority would be a limitation on the leverage of hedge fund users of FICC, which could be achieved via capital requirements.

While, on average, the hedge fund industry has a leverage ratio in the high single digits—approximately eight—the industry has become highly concentrated.17 In the second quarter of 2019, for example, the 25 largest hedge funds accounted for 50 percent of borrowing, although they had less than 14 percent of net assets.18 So large hedge funds may, at times, have leverage ratios in the high 20s. This is substantially higher than the average leverage of global systemically important banks, which is about 17.19 Moreover, hedge funds lack supervision, access to insured deposits, and access to the Federal Reserve as lender of last resort. Clearly, this is a source of fire sale risk, which, at scale, threatens the normal functioning of the Treasury market and overall financial stability.

Therefore, in exercising its Section 805 authority, the Federal Reserve may determine that any hedge fund taking positions in the Treasury market via FICC—whether as a member or a sponsored member—must meet stricter leverage requirements than those that apply to banks. For banks, broker-dealers, and other entities covered by federal financial regulations, FICC risk management standards default to regulator capital requirements, in that they trust that regulator-imposed leverage and risk-based capital requirements ensure that the banks will be able to meet their obligations and not threaten the operation of FICC.20 But this does not address the financial stability risks hedge funds create.

Imposing leverage limits on hedge funds would reduce their ability to take large, leveraged, risky positions in Treasuries. Unless these funds raised substantially more equity, this also would reduce the role of hedge funds as buyers of Treasuries in normal market conditions. But since hedge funds have proved to be a source of large-scale market disruption, and could be so again, this seems like a reasonable trade-off.

Section 805 requires that any such standards be determined in consultation with the Securities and Exchange Commission and the Financial Stability Oversight Council, since stability regulation needs careful design. However, given the importance of limiting shocks to the Treasury market, effective collaboration should not be difficult to achieve.

Allowing GSIBs to increase their leverage is unlikely to make the market for Treasuries less vulnerable

Limiting hedge fund leverage would not completely resolve the Treasury fire sale problem. Even if leverage is limited, NBFIs can still engage in massive selling. Bond funds, for example, sold Treasuries in 2020 in order to meet cash redemption for their shareholders, not because the funds themselves were leveraged.21 Moreover, there is concern that the expansion of outstanding Treasury debt, which is nearly four times its 2008 value, has outpaced broker-dealer buying capacity.22

This decline in the broker-dealer share of Treasury holding has prompted proposals designed to increase it. In practice, private sector “balance sheet expansion” amounts to relaxing requirements that apply to GSIBs. U.S. banking regulations require that GSIBs meet a supplementary leverage requirement (SLR), which counts GSIB reserves held at the Federal Reserve and Treasury holdings as assets that must be counted when calculating banks’ equity-to-asset ratios. Eliminating them from SLRs thus would allow additional asset purchases. The hope is that the eight U.S. GSIBs—which account for about half of all bank Treasury holdings—would use some of their expanded buying capacity on Treasuries.23

While it is true that the GSIBs may expand their Treasury holdings, they also may not. Although they are all primary dealers with a business agreement to act as market makers for Treasuries, they could easily allocate much of any freed-up buying capacity to other assets.24 In fact, data from a recent natural experiment suggest that holding Treasuries may not be a priority. From April 2020 to March 2021, Treasury securities and bank reserves were excluded from SLR calculations, providing balance sheet expansion. However, there was no noticeable effect on Treasury intermediation by the six largest Treasury dealers, which are subsidiaries of GSIB bank holding companies.25 At the next fire sale, there is no guarantee that GSIBs’ capacity to act as buyers would be meaningfully increased by a continued exclusion of Treasuries from SLRs.

On the contrary, removing reserves or Treasury holdings from leverage requirements would make GSIBs less able to absorb losses during the next big financial shock. The fact that they emerged from the 2020 financial shock intact was in substantial measure because of the scale of Federal Reserve intervention. The Fed set up a huge array of asset-buying facilities that included Treasuries, corporate bonds, bank loans, and some exchange-traded funds—essentially guaranteeing much of the financial system, as in the financial crisis of 2007.26 If Treasuries, which have market risk, and reserves are excluded from leverage calculations, there should be compensating increases in leverage requirements to cover other assets.27

See also

Conclusion

As events in the U.S. Treasury markets and the U.K. gilts market have demonstrated, NBFIs pursuing complex, leveraged financial strategies can disrupt very important financial markets. The recent SEC proposal to require clearing of Treasury trades should itself be leveraged by the Federal Reserve, whose authority over systemically important financial market utilities can be used to limit the leverage of hedge funds and other NBFIs who are now important players in the Treasury market. This would mitigate the fire sale risk these entities pose in the Treasury market.

{kind=link}