Denmark

The past few months have been turbulent ones in Danish politics. A general election was held in November 2022 after the Social Democrat government was given an ultimatum by its social liberal coalition partners. The ultimatum followed a report criticising the government for a controversial mink cull during the coronavirus pandemic.

After the election, the Social Democrats were again the biggest party and entered into negotiations to form a government.

Just before Christmas, the Social Democrats, the conservative-liberals Venstre party, and the Moderates agreed to work together as a centrist government.

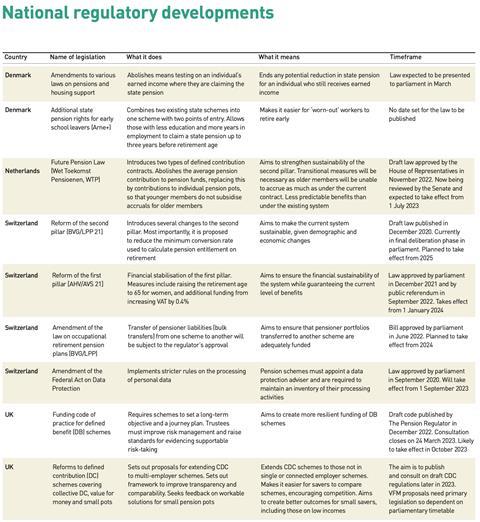

The previous government had agreed with other parties to abolish means testing for earned income – which consists of salary and income from self-employment – for individuals who were also claiming the supplementary state pension. This was to take effect from 1 January 2023.

Under the existing rules, the means-testing included not only an individual’s earned income, but their partner’s as well, potentially further reducing that individual’s state pension.

The bill abolishing means testing for a partner’s earned income was passed in June 2022, taking effect on 1 January 2023. However, because of the election campaign and subsequent government negotiations, the corresponding bill for an individual’s own income has not yet been tabled.

It is expected that this will happen in the first half of 2023.

The previous social democratic government also introduced the so-called ‘Arne’ pension, with applications opening in August 2021.

Arne is an early retirement state pension, payable to those who were early school leavers with less education and more years in employment than the average Danish worker, to make it easier for them to retire early after a strenuous working life.

It is a rights-based model with a monthly benefit of DKK14,000 (€1,880), payable for up to three years before retirement age.

However, the Arne pension has proved less popular than expected.

The main reason is that another state pension – the Senior Pension – while requiring a visit of inspection from the local authority, ensures a higher monthly benefit of at least DKK16,700.

To receive the senior pension, the individual must meet several conditions:

- Have six years or less until state pension age;

- Have worked for at least 27 hours a week for at least 20 years;

- Have a significant and permanent reduction in their ability to work, to a maximum of 15 hours per week compared with their last job.

The government plans to combine the two pension schemes into one new scheme, ‘Arne+’, with two means of entry – a rights-based model and a visitation model.

Both these models will allow the pension to be received up to three years before public pension age, at a monthly benefit level of around DKK15,000.

It is not known exactly how the new government intends to finance the pension. But it has said it will cancel the plans, presented to parliament by the former government just before the election, to tax companies on the annual change in value of rental properties worth more than DKK100m.

Germany

In September 2022, the German Federal Ministry of Labour and Social Affairs started a dialogue with stakeholders in occupational pensions with the objective of identifying ways to strengthen the sector in Germany.

The focus is on social and labour, and also tax and supervisory, law.

In addition, stakeholders have been asked for ideas on how the use of pure defined contribution (DC) schemes (reine Beitragszusage) could be enhanced.

Pure DC schemes have been possible in Germany since 2018 but are always subject to an agreement betwen social partners.

However, the first two DC schemes were only launched in late 2022. Legislative proposals following the dialogue with stakeholders are expected in 2023.

It is an open question whether there will be more pure DC schemes in 2023, or whether potential users of these DC schemes will wait for the results of the legislative process.

German Bundestag and parliamentary library: Berlin is seeking to boost supplementary pensions

In January 2023, the Federal Ministry of Finance started a similar dialogue with stakeholders (Fokusgruppe private Altersvorsorge) in relation to personal third-pillar retirement arrangements.

The group will consider the current framework of government support for personal pensions, including improving support for products with higher expected returns and potentially lower guarantees.

A report is expected to be published in summer 2023.

A national debate on early retirement has been started by German chancellor Olaf Scholz, who said last December in newspaper interviews that he wanted to create conditions for people to work longer.

Figures from the Federal Institute for Population Research had previously shown that many baby boomers are leaving the labour market at 63 or 64 years old, compared with the statutory retirement age, planned to rise to 67 by 2031.

The Institute said this had led to a shortage of experienced workers in the German labour market.

Scholz suggested more women could join the labour market by expanding all-day services in crèches and schools, and that better opportunities could be given to young people by investing in vocational training and further education.

The Confederation of German Employers’ Associations has since supported this view, calling for an end to incentives for early retirement.

However, members of governing coalition parties have been vociferous in attacking any plan to raise the retirement age further, or to cut pensions for those who have made higher contributions, as has also been suggested.

It looks as if the path towards any solution will be tough to navigate.

Interest rates increased sharply in 2022 and may even rise further in 2023. Providers of occupational pensions in Germany, which usually pay high guarantees, have suffered from the long-standing low interest rate environment.

Rising interest rates may have a positive effect on liabilities, but there are also potential risks based on the diminishing value of bond portfolios if rates go up.

So the further development of interest rate levels will be a major issue for occupational pensions in Germany in 2023.

In October 2021, EIOPA issued an opinion on the supervisory reporting of costs and charges of IORPs. The Federal Financial Supervisory Authority (BaFin) is now conducting a stocktaking exercise in relation to the cost situation of German IORPs.

This exercise is intended to find out whether regular cost reporting, as envisaged in EIOPA’s opinion, would be appropriate for German IORPs.

The Netherlands

After one year of preparation, 90 submitted amendments and motions, and over 100 hours of debate, the Future Pension Law (Wet Toekomst Pensioenen, or WTP) was approved by the lower house of parliament, (Tweede Kamer) on 22 December 2022.

The new law constitutes a major reform to the Dutch second pillar, formalising the change from a defined benefit (DB) to a defined contribution (DC) pension system.

It introduces two new types of collective DC contract: the so-called solidarity contract, with strong collective features including for the investment policy; and the alternative, a flexible contract more like an individual DC scheme.

The risk preference of the member population is an important starting point for the investment policy in the new pension contract.

In most cases, not only new, but also existing, accruals will be transferred to the DC system.

The new system abolishes average contributions.

At present, members pay the same premium whatever their age. This is then redistributed and used partly to cross-subsidise pension provision for the oldest members.

Under the new regime, an individual’s contributions will go directly to their own pension pot. But this means that participants who have paid for older cohorts for years and are now 45 or older will accrue less pension.

Retroactive indexation has also been introduced in anticipation of the new system.

And since last year saw unprecedently high inflation, sharp rises in interest rates, and therefore falls in the value of pension fund liabilities, many pension funds used the opportunity to put in place additional indexation.

“Due to the rise in interest rates, the required compensation burden has risen,” says Frank Driessen, CEO, Aon Wealth Solutions in the Netherlands. “This middle group [45-plus] must be compensated. The transition must be balanced for all participants and now part of that extra money is being spent on indexation, this is a concern.”

The Senate, now deliberating on the WTP, is expected to take several months to give its approval to the legislation. The expected date for the law to take effect is 1 July 2023, with a final transition date of 1 January 2027.

As a consequence, by 1 July 2024 there must be a draft agreement between the social partners on the choice of contract, transferring accrued rights to the new system and compensation.

Driessen says: “The transition to the WTP means that administrative organisations – pension administrators – and pension funds are considering their future. Smaller pension funds are wondering whether they still want to switch to the new system, or whether to place their obligations elsewhere.”

There are now just over 180 pension funds in the Netherlands, 10% less than a year ago.

Meanwhile, new mortality forecasts from Statistics Netherlands have led to an adjustment of the state pension age, which will rise from 67 years to 67 and three months from 2028. The current retirement age for second-pillar plans is 68 years.

In November 2022, the ‘parameters committee’ – which every five years publishes assumptions for investment returns that pension funds are allowed to use when setting their contribution rates – issued its latest recommendations, adjusting the average expected return on equity from 5.8% to 5.4%.

So momentous times are coming for Dutch pension funds, since a lot has to happen within a short time frame. “The big challenge will be to move to the new system in a balanced way,” says Driessen.

“Buffers will have to be distributed in such way that pensioners are compensated for missing indexation for a number of years, and actives are compensated for the abolition of the average premium. This will be the subject of discussion. Pension funds have to weigh the interests of all stakeholders carefully.”

Sweden

The Swedish financial supervisory authority Finansinspektionen (FI) has published its programme of priorities for 2023, which includes examining how the financial sector deals with high inflation, rising interest rates and an economy which is generally getting more fragile.

During the period of low interest rates, Swedish life insurance and occupational pension undertakings reallocated assets from interest-bearing securities to higher risk assets like equities.

Finansinspektionen: priorities for 2023 include dealing with financial fragility

FI says that higher interest rates will, however, have a positive effect on long-term liabilities (technical provisions) for traditional life/occupational pension insurance from a solvency standpoint.

Meanwhile, it is also prioritising the protection of basic payment services in the event of cyber attacks, and will be reviewing the way in which financial companies are engaged in preventing and handling these attacks.

During 2023, FI will also continue to make sustainability a part of its ongoing supervision, examining how institutions integrate sustainability into their corporate governance and risk management.

The results will be used as a basis for supervisory dialogue and qualitative assessment of the institutions’ risk level with regards to sustainability.

FI also believes that the pensions sector can fill an important role in the transition to a sustainable economy. This function entails identifying, measuring and pricing opportunities and risks related to the transition.

At the end of 2022, FI published its roadmap for sustainable finance, as well as its strategy to prevent greenwashing.

The latter in particular reflects FI’s priority of working to reduce the risk of greenwashing in the pensions sector and financial industry generally, both through preventive measures and supervisory activities.

One way to achieve this will be by implementing new rules and maintaining a dialogue and communication with the industry, improving access to sustainability-related information and following up on information provided, in conjunction with financial advice.

FI will also prioritise work in international collaboration to prevent greenwashing.

During the past two years, the right to transfer unit-linked and occupational pensions to a new provider has undergone legislative changes, and the Swedish government has commissioned FI to assess how this is working for individual occupational pensions.

The first change, effective in April 2021, imposed a cap on the fee an insurer can charge for transferrable policies. This was followed in July 2022 by measures which enhanced transfer rights to unit-linked policies sold before 2007.

FI has now been commissioned to assess the occurrence of transfers of individual occupational pension policies in recent years, and to investigate the legal and practical challenges that hinder such transfers.

The European Commission has called for EIOPA’s technical advice on the evaluation and review of the IORP II Directive, in accordance with Article 62 of the Directive.

EIOPA has now published a paper for public consultation and FI is encouraging Swedish stakeholders to engage in this consultation.

The Swedish occupational market differs from other countries because around 90% of Swedish employees are covered by occupational pension arrangements resulting from collective agreements, so FI believes it is important that stakeholders keep this in mind when responding.

EIOPA’s technical advice is to be delivered to the commission by 1 October 2023.

Switzerland

The finishing line is now in sight for several pieces of legislation which have been years in the pipeline.

The draft law to reform the second pillar (BVG/LPP 21) was published in December 2020 and is currently in the final consultation phase in parliament.

The changes are aimed at making the current system sustainable, the most important being a proposed reduction in the minimum conversion rate used to calculate pension entitlement on retirement. In addition, the reform intends improving insurance coverage for individuals working part time or for multiple employers.

However, the two parliamentary chambers have different ideas as to what details should look like and are trying to find a compromise.

“It’s clear for everybody that the conversion rate will have to be reduced from 6.8% to 6.0%” says Simon Heim, head of Swiss Life’s employee benefits legal practice. “But the transitional measures for those who are close to retirement are subject to disagreements. Another point of disagreement is the so-called coordination deduction, which is used to define the pensionable salary.”

Under current law, roughly the first CHF25,000 (€25,379) of annual salary is not insured under the second pillar (co-ordination deduction), because this part is covered by the first pillar. Legislators want to substantially reduce the uninsured part.

This means significantly higher second pillar contributions, especially for lower incomes, but correspondingly higher pensions later on.

However, Heim is optimistic that parliament will find consensus on both matters in the spring session, which ended in March.

Whatever the act finally looks like, trade unions have already announced a public referendum, so the public will have the final say.

According to Heim, the outcome of a referendum is uncertain, since the public have already previously voted twice against a reduction of the minimum conversion rate.

The changes are planned to take effect from 2025.

The law to achieve financial stabilisation of the first pillar (AHV/AVS 21) was approved by parliament in December 2021 and by a public referendum held in September 2022. Measures include raising the retirement age for women to 65 (which will also apply to occupational schemes), and other provisions to encourage people to stay longer in work.

The new act creates additional funding for the first pillar by raising the rate of VAT by 0.4%.

Its provisions will take effect from 1 January 2024.

The amendment to the law on occupational retirement plans (BVG/LPP), covering the transfer of pensioner liabilities (bulk transfers) from one scheme to another, aims to ensure that pensioner portfolios are adequately funded.

Such transfers will now have to be approved by the regulator.

Parliament passed the law in June 2022. It is now up to the Federal Council (the executive body of the federal government) to specify the technical details in an ordinance.

The new provisions are expected to take effect from 1 January 2024.

Although Switzerland is not in the EU, compatibility of Swiss data protection law with the

General Data Protection Regulation (GDPR) is required in order to ensure that the free movement of data with the EU can be maintained so that Swiss companies do not lose competitiveness.

The relevant amendments to the Federal Law on Data Protection were approved by parliament in September 2020, since when the Federal Council has been preparing the technical details in form of an ordinance.

Most Swiss pension funds already have high data protection standards, but they will now have to appoint a data protection adviser and formalise documentation.

The changes take effect on 1 September 2023.

UK

The UK pensions sector has been buffeted this year by a welter of new rules and consultations affecting second pillar schemes.

The Pension Regulator’s (TPR) draft funding code of practice for defined benefit (DB) schemes, published last December, requires schemes to set a long-term objective and a journey plan to get there.

It is expected that schemes will reduce reliance on their sponsoring employer as they reach maturity. The code will require trustees to improve risk management and raise the bar for evidencing supportable risk-taking.

The consultation closed on 24 March and the final regulations and code are currently planned to come into force in October 2023.

A number of initiatives were prompted by last September’s spike in Gilt yields after the short-lived Truss government’s mini-budget, leading to margin calls on some liability-driven investing (LDI) portfolios and the risk of forced sales of Gilts at disastrously low prices.

Last October, the Parliamentary Work and Pensions Select Committee launched an inquiry to learn lessons from the debacle.

The inquiry is focusing on the impact of the volatility in Gilt yields on DB schemes with LDI strategies and their regulation and governance.

The committee said it also intends to launch a further inquiry into DB schemes.

Meanwhile, the Bank of England has since said it will propose a framework for LDI funds, setting out what well-managed leverage requires, with the intention of ensuring resilience in terms of liquidity. This had not been published by the time this publication went to press.

It would then be up to regulators to consider implementing any rules.

The introduction of collective defined contribution (CDC) schemes in the UK last year was a landmark moment for UK pensions.

Altered landscape: UK pensions are undergoing some fundamental changes

The Department for Work and Pensions (DWP) has now launched a consultation to extend the framework beyond single and connected employer schemes, and explore what new types of multi-employer CDC schemes should look like and how to maximise their benefit for savers.

Feedback from stakeholders has already suggested that a reasonable first step might be for multi-employer CDC schemes to operate

as whole-life schemes, providing accumulation and decumulation on a collective basis in one package, under the regulatory oversight of TPR.

It is also seeking views on the role of CDC in decumulation, particularly the potential for CDC decumulation-only products.

The CDC consultation is part of a package of measures to help address the pension inequality gap which has risen since the decline of DB and the emergence of DC schemes. These measures include a consultation on a new value for money (VFM) framework, to improve transparency, comparability and competition between DC schemes.

The framework will require pension schemes to disclose key metrics and service standards, shifting focus from a dominant consideration of costs only.

There is also a call for evidence on ‘small pots’, which can create extra costs and inefficiencies.

The investigation is focused on two large-scale automated consolidation solutions – a default consolidator model and pot follows member – and will seek feedback on workable solutions, enabling better outcomes for savers. All these consultations closed on 27 March 2023. The DWP aims to consult on draft regulations for CDC schemes later this year.

Many proposals in the VFM require primary legislation; the timing would therefore depend on the parliamentary timetable.

Meanwhile, new rules on illiquid investments are expected to take effect from April 2023. These will require schemes to provide transparency to savers over their approach to illiquid assets, and disclose information on their overall investment asset allocations.

They will also enable trustees to exempt performance-based fees from their charge cap calculations, where they feel it is in their members’ best interests.

Both measures are intended to stimulate investment in illiquid assets by DC pension schemes.

In his Spring Budget, the chancellor of the exchequer, Jeremy Hunt, announced plans to incentivise DC pension funds to invest in domestic UK growth equity, including a so-called ‘Long-term Investment for Technology and Science’ initiative.

The government is also to consult on requiring Local Government Pension Scheme (LGPS) funds to channel further investment towards illiquid assets.

The chancellor also pointed towards further consolidation of assets within the LGPS sector – including a smaller number of pools of above £50bn.

{kind=link}