LONDON, Sept 13 (Reuters) – Whether China has become “uninvestable” or not, avoidance of the world’s second-largest economy suggests the economic and political risks there have simply become too hard to assess.

U.S. Commerce Secretary Gina Raimondo’s trip to China last month had promised some economic and trade detente between the two superpowers now at loggerheads. But it was quickly defined by her comment that more and more U.S. firms see China as “uninvestable” amid spying, fines, raids and other risks.

While bricks-and-mortar investment, supply-chain exposure and stock listings have been under a spotlight since the pandemic, portfolio flows have been balking at prospects as well.

Fear of a systemic property bust, a disappointing post-COVID economic recovery and piecemeal government supports all raise red flags over returns and performance over the near term and the yuan slide has accelerated.

But rancorous geopolitics and related bilateral investment curbs in sensitive technology and security-related sectors kick many long-term value plays or contrarian trades into touch too.

As some reflection of that, Bank of America’s global fund manager survey this week spotlighted the extent to which all those fears are translating into investment positioning.

Net allocations to China-dominated emerging market equities “collapsed” 25 percentage points over the past month to their lowest of the year – the largest monthly decline in exposure in almost seven years.

A third of respondents in the survey cited Chinese real estate as the biggest “credit event risk”, overtaking nerves about U.S. and EU commercial real estate.

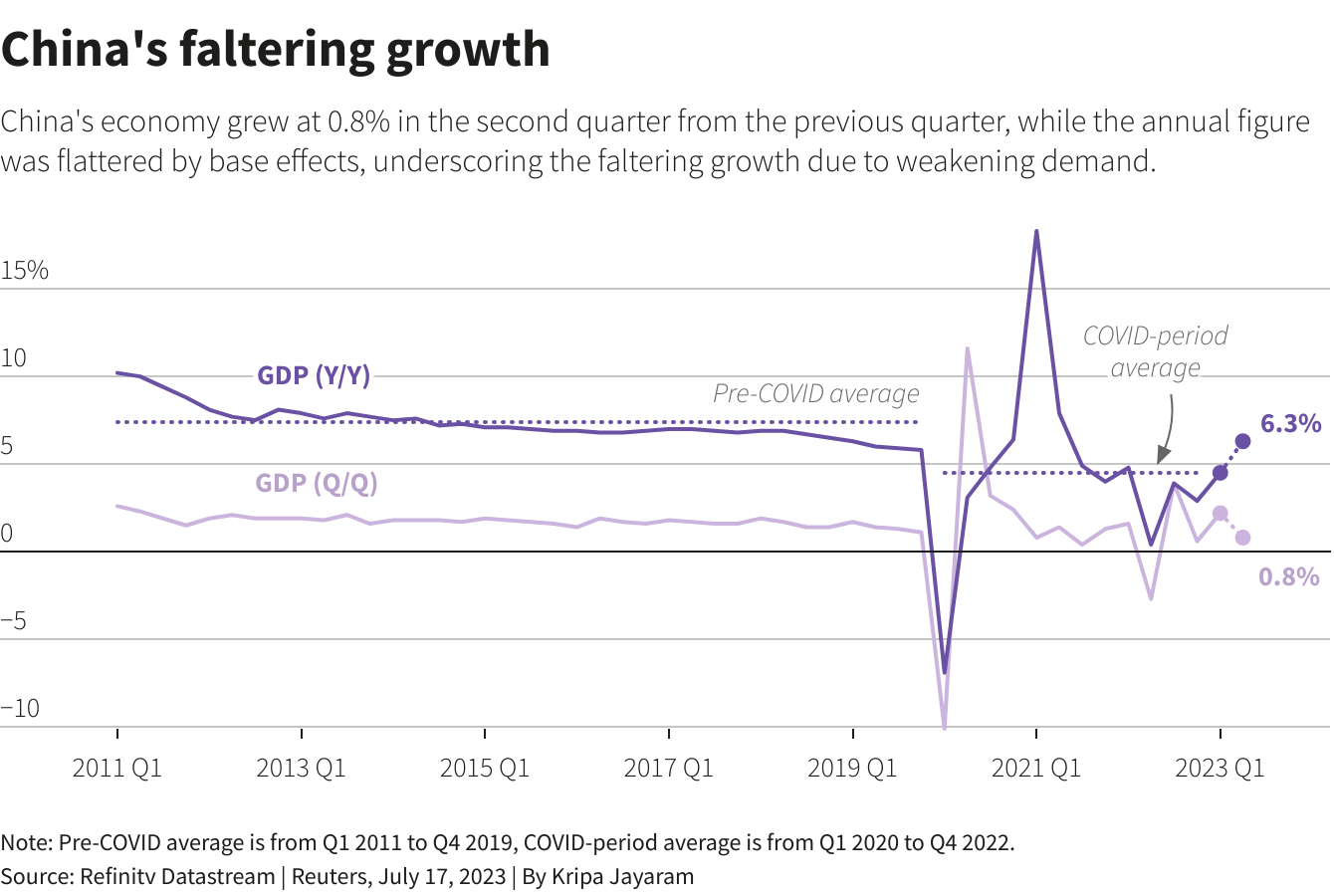

And none of the 222 funds polled expected China economic growth to be any higher next year than this – mirroring a recent Reuters survey of domestic and overseas banks and investors.

Perhaps most significantly, the dour China-led emerging markets outlook was independent of an improving global growth picture overall – with a rise in exposure to U.S. equity this month the biggest in the survey’s history and the first net overweight position since August 2022.

The net shift from emerging markets to Wall St was also the largest in the 20-plus years of the poll.

As these sorts of surveys go, there’s an awful lot in there that could spell “peak gloom”. Investment skews of this scale are often good contrarian indicators.

Indeed, shorting China equities was deemed the second “most crowded trade” behind long exposure to supercharged Big Tech stocks.

“THE RISK IS BAD”

But the problem seems far more than just cyclical ebb and flow and embeds aspects of the thick political fog and investment shift that unfolded after the emerging markets collapse in the late 1990s.

Back then, a surge in political and currency risk around Asia and other developing markets saw visibility disappear. U.S. money fled home to a domestic emerging market in Silicon Valley – and was partly responsible for fuelling the dot.com bubble that burst in 2000.

China was only a bit player in the investment world at the time, of course. Now it’s a challenger to U.S. economic heft – unlike any of the emerging economies in the fray 25 years ago.

But the degree to which recent seismic geopolitical risks have changed the basic risk calculus is a parallel.

Asset managers and financiers everywhere have registered their discomfort pretty openly.

JPMorgan boss Jamie Dimon said this week that his takeaway from a trip he made to China this year for the first time in four years was “highly cautious”, adding that the risk-reward from JPMorgan’s own business there had deteriorated. “The risk is bad,” he said.

Jay Clayton, former chair of the U.S. securities regulator, told lawmakers on Tuesday that big U.S. public companies should start disclosing their exposure to China as part of a pilot program to allow investors and policymakers to see potential risks.

“If it’s demonstrated to investors the level of risk has increased, they will pull back,” he said.

Last week, Norway’s $1.4 trillion sovereign wealth fund, one of the world’s biggest investors, said it was closing its only office in China – even though it said it would continue to invest in the country.

Earlier this month CPP Investments, Canada’s biggest pension fund, became the latest Canadian investor to downscale operations in Hong Kong and step back from deals in China. The Ontario Teachers’ Pension Plan closed down its China equities investment team in April and Caisse de dépôt et placement du Québec was reported to be closing its Shanghai office this year.

To be sure, the battle for western investors’ hearts and minds is not all one sided.

China’s securities regulator said last week it held meetings with domestic and overseas investors including Temasek, Bridgewater and Blackrock to ease relations and lift confidence.

And Jenny Johnson, chief executive at Franklin Templeton, said this week the gloom was overhyped. “You’re probably not going to time it exactly right…but when it gets right it is going to be a rubber band back up.”

Willem Sels, chief investment officer at HSBC Private Banking and Wealth, remains neutral on the China market even though he said there were eye-catching picks in the internet sector, tourism, domestic services, gaming and electric vehicles for whenever an earnings upturn emerges.

“The only thing we’re missing is the catalyst for a quick upside,” he said, preferring for now U.S. stocks, the dollar and hedge funds over the next 3-to-6 months and favouring longer-term themes in the likes of India and Indonesia.

But with U.S. presidential elections due next year, appetite in Washington to resolve the political tension may be low.

According to a Reuters/Ipsos survey last month, bipartisan majorities of Americans favor more tariffs on Chinese goods and believe the United States needs to step up preparations for military threats from the country.

Even if the economy turns, political catalysts for a return to China may be slow in coming.

The opinions expressed here are those of the author, a columnist for Reuters

Reporting by Mike Dolan; Editing by Sharon Singleton

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.