Last autumn, 10-year gilt yields spiked over 4.5%, triggering a fallout amongst some pensions and contributing to the downfall of former Prime Minister Liz Truss and Chancellor of the Exchequer Kwasi Kwarteng, as commentators we follow blamed the duo’s pro-growth agenda of modest tax cuts for gilts’ jump.[i] Yields fell, we saw replacement Prime Minister Rishi Sunak and Chancellor Jeremy Hunt receive wide praise in financial coverage we follow for trying to rein in the deficit, and everyone seemingly moved on.[ii] So much so that now, with 10-year gilt yields now back above their October 2022 high, publications we follow haven’t reported on it much at all—nor have they called for the government’s ouster.[iii] We see a couple of timeless investment lessons here.

First, in our view, high interest rates alone didn’t cause last autumn’s pension earthquake. Back then, when long-term rates rose, it created a problem for pension funds using a tactic called liability driven investments (LDI). We have a more detailed synopsis here for those who would like a full refresh, but this is a tool funds use to (ideally) match long-term returns to long-term liabilities, and it involves using leverage. When long rates rose and gilt prices fell, several funds got hit with margin calls, i.e., demands to pay down loans or add collateral. To meet them, they turned to the easiest, most liquid source of cash: selling gilts. These forced sales further hit bond prices, which forced more sales until the Bank of England stepped in with emergency pension funding and bond-buying programmes.[iv] These helped bridge the gap until markets calmed, leaving a national debate about LDI and pension regulations in their wake. This culminated in new guidance, issued this April, mandating stress tests and higher liquidity buffers.[v]

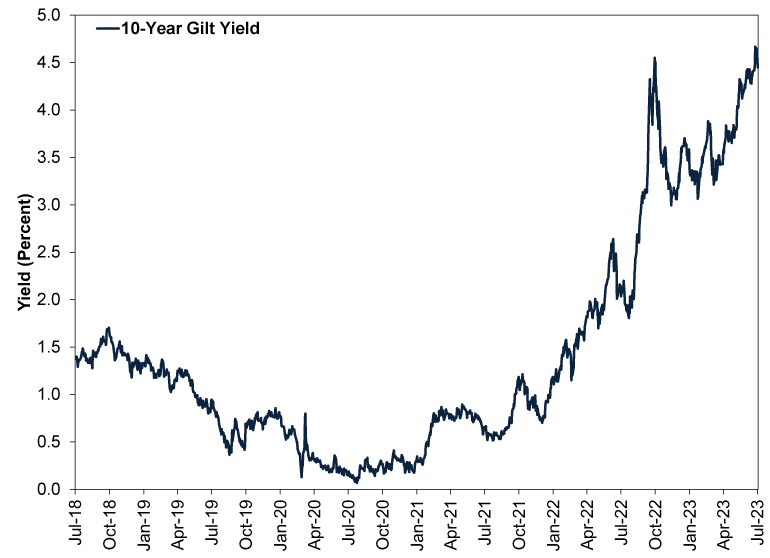

Those buffers may be one reason 10-year yields’ trip back north of 4.5% hasn’t triggered a fresh crisis—if not because of the new guidance, then because several funds reportedly built larger cushions proactively once last autumn’s events died down. We suspect gilt yields’ slower rise this time also plays a role. Exhibit 1 shows the 10-year yield’s movement over the past five years. Where last autumn’s jump was a twin spike, the latest ascent has been more gradual, likely giving funds time to adjust their portfolios as needed to prevent margin calls. Usually, we find it is markets’ rate of change, rather than their direction or cumulative move, that catches traders and fund managers off guard. This is likely one reason why our research finds there is no set level of interest rates (or any other market) that is inherently problematic. Time is a friend, in our view.

Exhibit 1: A Year in the Life of 10-Year Gilt Yields

Source: FactSet, as of 10/7/2023. 10-year gilt yield, 7/7/2018 – 7/7/2023.

Which brings us to Lesson Two: No political leader or policy suite has a pre-set market impact, according to our research. When yields fell as Sunak and Hunt took office, commentators we follow portrayed it as a foregone conclusion that this was a big market vote of confidence in the new leadership.[vi] Abandoning a modest tax cut agenda was supposedly the right thing to do: Fiscal probity would tame inflation (broadly rising prices across the economy) and lower interest rates would work hand in hand with lower deficits to restore the world’s confidence in the UK.

Sunak and Hunt fulfilled those austerity predictions with continued stealth tax hikes and some investment tax increases at this year’s Budget.[vii] We italicise austerity because this Budget—like former Chancellor George Osborne’s past austerity budgets—preserved spending increases. However, it was the antithesis of Trussonomics’ focus on unleashing investment and the private sector by putting more money back in the people’s hands. But inflation has been more stubborn than many commentators we follow projected, pumping long-term gilt yields back up and teeing up higher household bills as mortgage payments reset at higher rates.[viii] In other words, the very thing the proverbial grey-suited types were trying to stave off when they ran out Truss and Kwarteng. It appears the Bank of England’s rate hikes and global market factors were a much bigger influence on UK long rates than local political factors and deficit chatter.

In our view, this is a shining counterpoint against what we have observed is a widespread, perpetual temptation to presume Politician X will have Y effect on markets. Those presumptions are virtually always based on political biases, which are widely known and therefore pre-priced by stocks. Markets are typically excellent at doing what the crowd doesn’t expect. In our view, acknowledging this tendency is a key part of navigating political developments correctly.

Now for some parting good news: With inflationary forces easing and monetary policy institutions globally appearing much closer to the end of their tightening cycles than the beginning, the upward pressure on long rates in the UK, US and Europe looks likely to wane. Our research suggests this isn’t a direct stock market driver—contrary to what many seemingly argue these days. But in the UK at least we think it should help salve some of the concerns that have weighed on sentiment during the correction UK stocks have endured in price terms since their last high in mid-February.[ix] We have found turning points are impossible to predict or identify in real time, but as false worries gradually fade, we think UK stocks are likely to resume their climb up the proverbial wall of worry—with tailwinds from what we think are positive forces globally.

[i] Source: FactSet, as of 12/7/2023. Statement based on 10-year gilt yield on 12/10/2022.

[ii] Ibid. Statement based on 10-year gilt yield, 13/10/2022 – 24/11/2022.

[iii] Ibid. Statement based on 10-year gilt yield on 10/7/2023.

[iv] “Pension Fund Panic Led to Bank of England’s Emergency Intervention: Here’s What You Need To Know,” Elliot Smith, CNBC, 29/9/2022.

[v] “UK’s Pensions Regulator, FCA Set Out New LDI Guidance,” Rachel Fixsen, IPE, 24/4/2023.

[vi] Source: FactSet, as of 12/7/2023. Statement based on 10-year gilt yield, 25/10/2022 – 1/11/2022.

[vii] “Jeremy Hunt’s ‘Stealth’ Income Tax Rise: Here’s How It Will Affect You,” Zoe Wood, The Guardian, 18/3/2023.

[viii] Source: FactSet, as of 12/7/2023. Statement based on the UK Consumer Price Index including owner-occupiers’ housing costs and 10-year gilt yield, 24/11/2022 – 10/7/2023.

[ix] Source: FactSet, as of 12/7/2023. MSCI United Kingdom Investible Market Index price return in GBP, 20/2/2023 – 10/7/2023. A correction is a sentiment-driven decline of around -10% to -20%.

{kind=link}