With rising interest rates and the associated uptick in Pension Risk Transfer markets worldwide, a large volume of pension liabilities now find themselves on insurance balance sheets, requiring immunisation and liability matching. The need for high quality, longer duration, predictable cashflows is a structural phenomenon driving a substantial increase in demand for longer duration instruments. Whilst the US Treasury issuance will have to increase to finance deficits, and with that increase it will create more longer duration bond investments, the options for insurers around the world to match assets with liabilities using investment grade corporate bonds, is increasingly likely to become more limited. At higher interest rates, corporations, particularly those with cash, are less likely to want to lock in longer term rates. Indeed, long-term fixed income issuance declined 34.2% from June 2022 to June 2023. The trend is likely to persist over the secular horizon in a world of higher interest rates. As such, illiquid assets will need to be a larger component to deliver attractive returns with a good match for long-dated liabilities.

Take the UK as an example. According to Moody’s, UK life insurers’ combined illiquid investments have doubled since 2017, reflecting the insurer’s search for yield. Debt that qualifies for Solvency II Matching Adjustment is particularly attractive, as it confers regulatory, valuation and capital benefits.

The phenomenon, however, is much more widespread than the UK, and the same demand for long duration debt with predictable cashflows for yield, asset liability management and regulatory benefit exists under most risk-based capital regimes around the world: Bermuda (Scenario-Based Approach), Canada (solvency balance sheet through IFRS 17 valuation), Hong Kong (Matching Adjustment), Singapore (Matching Adjustment)… and counting, with the continued introduction of risk-based regimes across the world, including the International Capital Standards in many countries.

All of this will drive up competition for high-quality illiquid assets and as such, now is a prudent time to assess a wider array of options in liability matching.

Schroders Capital, the private markets investment division of Schroders, has made $2.5 billion of real estate loans in the United States.1 We are active both in the real estate private debt as well as the debt securities, a factor which gives us a good overview of what is happening across real estate markets.

Operating at every stage of real estate financing from land acquisition finance, through construction and development financing and bridging loans, to permanent loans on fully leased properties. Operating across the spectrum and by being relevant to borrowers through the investment lifecycle we build strong relationships with them: this in turn helps us source good quality loans.

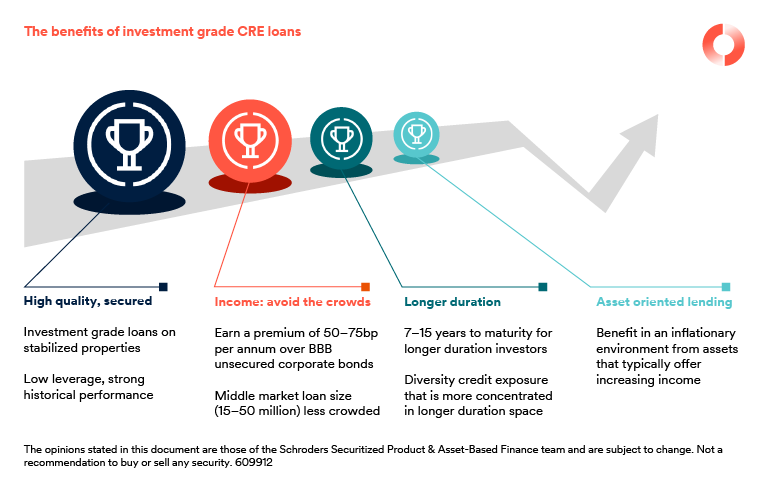

Further efficiency can be had through accessing the less competitive middle market (loans less than $50 million) where regional banks have traditionally dominated the lending. This allows financing on properties with strong fundamentals, strong borrowers and low leverage, to be provided at historically attractive coupons, simply by virtue of the pull back of the banks.

Specifically for insurers, we believe a good starting point in real estate debt markets in loans which were typically and historically financed predominantly by banks. Banks are facing more restrictive capital requirements as part of ongoing and increasing regulation. This will make it less likely that banks will be competitive in some lending markets, this includes US Commercial Real Estate (CRE) lending.

Our focus for our insurance clients in this area is on investment grade quality US CRE loans: those on stabilized properties with cash flow history, strong historical performance and low leverage.

Source: Schroders Capital, for illustrative purposes only. Past performance is not a guide to future performance. Not a recommendation to buy or sell any security.

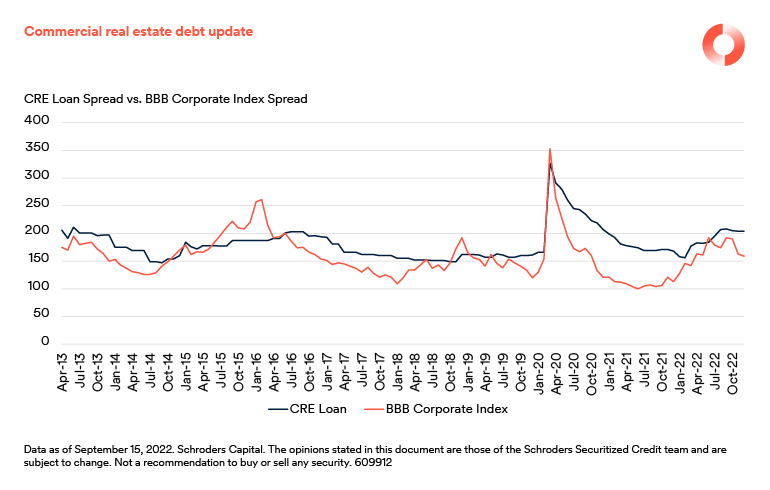

Building a portfolio of loans allows the management of loan term, leverage and location. We can focus on desirable markets and desirable property types that also comes with an additional pick up of 50-75bps of spread over corporate BBBs in most markets.

Source: Schroders Capital, data as of September 15, 2022. The opinions stated in this document are those of the Schroders Securitized Credit team and are subject to change. Not a recommendation to buy or sell any security.

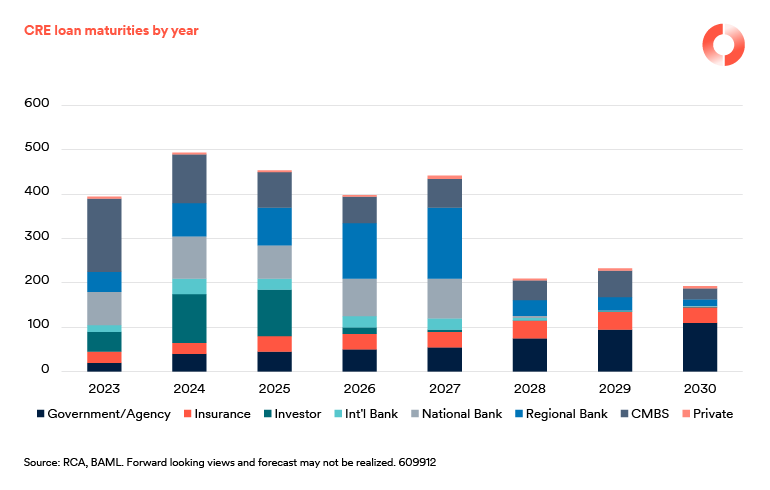

With the evaporation of regional bank competition this is likely to become more attractive and more scalable with more than $1tn in US CRE loans set to mature in the next two years: many will need to refinance.

Source: RCA, BAML. Forward looking views and forecast may not be realized.

With higher cap rates, reduction in competition and a wave of maturities, a market with capital scarcity is likely one where both quality and return can be high.

However, despite changing market dynamics, we do not have to change how we structure loans or insert new covenants. In less competitive markets, terms have evidenced little degradation. We had maintained standards as the market expanded, which is critical to maintaining a healthy portfolio. This is well demonstrated by the fact that during the pandemic, none of our permanent loans defaulted, asked for modification (relief), or missed a payment. This has been a good outcome for our investors (and their boards and committees).

Indeed, the main protection which we have long built into our structuring is ‘consent leverage’ which enables us to vary loan covenant features. For example, if a tenant gives notice of a lease expiring, we are able to sweep up the cash-flow. We were fortunate to have all of these protections going into COVID, and they are obviously particularly important now that interest rates weigh on the LTV calculations around an asset.

In many cases, for a loan refinance, borrowers will have to put “cash in”; we view this commitment as a huge positive, especially as interest rates are likely to be the highest we’ve seen in decades, for a prolonged period of time. In normal markets we favour acquisition loans as there is a valuation and cash equity committed.

Regional preference is key today, as fundamentals are very localized. We clearly have some areas we prefer to others, based on their fundamental attributes. These include net migration, calculations of future supply demand, and local economic circumstances, as well as the diversity of the local economy and its population.

In consequence of these considerations, we have focused our efforts on markets where there has been significant migration in search of more favourable tax regimes, more jobs and better quality of life. This is not a new way of thinking. Avoiding crowded, peak valued markets, with more downside than upside is the core of relative value, and even more important in non-tradeable assets.

Control, quality, covenants and secured predicable income on stabilised properties is an ever increasingly interesting option for those investors that seek a more diversified, efficient and evolved liability matching portfolio.

{kind=link}