- This is Money’s long-running mortgage rates round-up looks at the best deals and what you need to consider when looking for a home loan

- We round-up the best fixed rate and tracker rate mortgages

- Check the top deal for your situation with our mortgage calculator tool

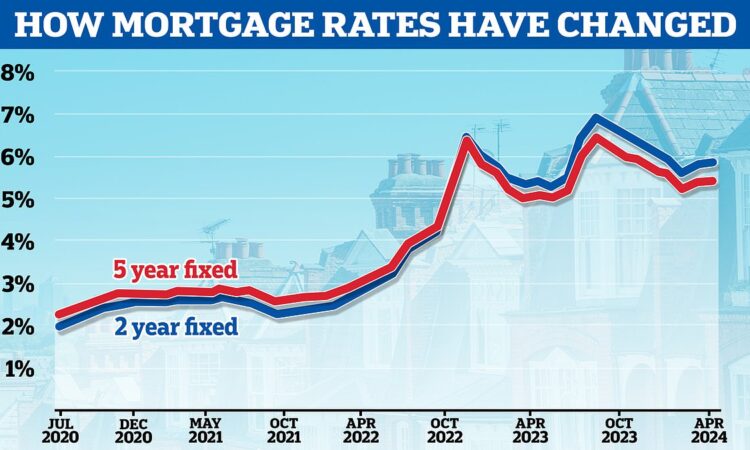

Fixed mortgage rates have edged up since February, after almost six months of consecutive rate cuts by lenders.

Since the start of February the average two-year fixed rate mortgage has risen from 5.56 per cent to 5.81 per cent, according to Moneyfacts.

Meanwhile, the average five-year fix has risen from 5.18 per cent to 5.38 per cent.

The lowest five-year fixed rates on the market are currently all above 4 per cent while the lowest two-year fixes are all above 4.5 per cent.

This will come as a hit to the 1.6 million households remortgaging this year, many of which will be coming off rates of 2 per cent or less.

This pain is expected to continue over the coming years as more people come to the end of their cheaper fixed rate deals.

OBR figures indicate that average mortgage interest rate, when taking into account all households, will hit a peak of 4.2 per cent in 2027. This is up from a low of around 2 per cent at the end of 2021.

However, this is 0.8 percentage points lower than the OBR forecast in November.

The OBR said its latest forecast has been changed as a result of a decline in market expectations for the Bank of England’s base rate, which currently sits at 5.25 per cent.

> Best mortgage rates calculator: Check the deals you could apply for

It’s important to distinguish here between the OBR average rate and the market average rate.

The OBR rate includes all fixed and vairable rates that households are currently paying, including those who remain on very low fixed rate deals – hence why it is lower than the market average rate.

The market average rate, as reported by Moneyfacts, takes into account every fixed rate deal currently available to those either buying or remortgaging. This includes the very cheapest rates, but also the most expensive rates – reserved for those with niche circusmtances or poor credit history.

What’s happened to the market average rate?

Last year, a succession of base rate hikes and disappointing inflation figures saw average two-year fixed mortgage rates reach a high of 6.86 per cent in the summer, according to Moneyfacts, while five-year fixed rates hit 6.35 per cent.

But with the rate of inflation falling back and the Bank of England holding base rate at 5.25 per cent since August, mortgage lenders began cutting rates.

This rate cutting continued into 2024. In January alone, more than 50 mortgage lenders cut their residential rates – some more than once.

While mortgage rates have crept up since February, the cheapest deals remain a lot more palatable then the highs people had to ensure last summer.

In terms of the lowest rates, borrowers can get relatively close to 4 per cent when fixing for five years or just above 4.5 per cent when fixing for two years.

Ultimately, mortgage rates still remain far higher than mortgage borrowers had enjoyed prior to the surge in 2022.

Little more than two years ago, the averages were hovering around 2.5 per cent for a five-year fix and 2.25 per cent for a two-year.

In fact, only as far back as October 2021, the lowest mortgage rates were under 1 per cent.

This is Money’s best mortgage rates calculator can show you the deals you could apply for and what they would cost.

You can also work out how a different interest rate would change your monthly payments, taking into account any fees, using our true cost mortgage calculator.

What next for mortgage rates?

Mortgage borrowers on fixed term deals should worry less about where the base rate is today, and more about where markets think it will go in the future.

This is because banks tend to pre-empt base rate movements. Lenders change their fixed mortgage rates on the back of predictions about how high the base rate will ultimately go, and how long inflation will last for.

Last year, forecasts for where the base rate would eventually peak fell from a high of 6.5 per cent to 5.25 per cent and then focus turned towards when base rate would be cut.

At the start of this year, markets were pricing in six base rate cuts in 2024 with investors betting on rates falling to 3.75 per cent by Christmas.

They have since rolled back on this following stubborn inflation readings that came in slightly higher than markets had predicted.

Investors are now forecasting that rates will fall to 4.5 per cent by the end of this year – with the first move downwards coming in June.

Market expectations are reflected in swap rates. These are agreements in which two counterparties, for example banks, agree to exchange a stream of future fixed interest payments for a stream of future variable payments, based on a set amount.

Mortgage lenders enter into these agreements to shield themselves against the interest rate risk involved with lending fixed rate mortgages.

Put more simply, swap rates show what financial institutions think the future holds concerning interest rates.

As of 11 April, five-year swaps were at 4.05 per cent and two-year swaps were at 4.6 per cent – both trending below the current base rate.

This is slightly up compared to the start of the year when five-year swaps were 3.4 per cent and two-year swaps were 4.04 per cent.

However, it’s a lot lower than it was during the summer of 2023.

Only as recently as July, five-year swaps were above 5 per cent. Similarly, the two-year swaps were coming in at around 6 per cent.

You can check best buy tables and the best mortgage rates for your circumstances with our mortgage finder powered by London & Country – and figure out what you’ll actually be paying by using our new and improved mortgage calculator.

Why did mortgage rates rise?

Mortgage rates first began to increase towards the end of 2021, when inflation began to rise resulting in the Bank of England increasing base rate to try and combat it.

However, rates accelerated after the mini-Budget in late September. The pound tumbled after the then-Chancellor, Kwasi Kwarteng, announced a wave of unfunded tax cuts that unsettled bond markets.

After former Prime Minister, Liz Truss, resigned in October and new Chancellor Jeremy Hunt reversed nearly all of the mini-Budget announcements. The markets calmed down and the cost of borrowing then fell with mortgage rates slowly dropping too.

But following a fresh round of stubbornly high inflation figures in 2023, markets began betting the base rate would peak at 6.5 per cent by the end of the year.

This led to mortgage lenders beginning to whack their rates up again.

However, when June’s inflation figures came in lower than market expectations, market forecasts as to where the base rate would peak fell to below 6 per cent.

And after a string of further positive readings on the inflation front, markets settled on a base rate peak of 5.25 per cent (where it is now) and began forecasting cuts in 2024.

What will happen to house prices?

Depending on which house price index you follow, property prices may have either fallen slightly over the course of 2023 or be marginally up.

According to the latest figures from the Office of National Statistics (ONS), as of January, the average home is worth 0.6 per cent less than it was a year earlier, as the mortgage crunch took its toll on property sales.

However, the latest house price index from Halifax, which relates to its own approved mortgage applications, said that house prices have inched up 0.3 per cent compared to this time last year.

Meanwhile, Nationwide has recorded a 1.6 per cent rise annually.

Looking ahead, many predictions were downbeat at the start of the year with some forecasters expecting prices to fall by up to a further 5 per cent in some cases.

But there are now plenty with a more positive outlook for house prices thanks to a stronger start to the year with more buyers and sellers on the move.

The estate agent Knight Frank said house prices would rise by 3 per cent this year having previously predicted a 4 per cent fall.

It flipped its forecast on the back of falling inflation which it says will lead to falling interest rates, which in turn will help galvanise the market.

Other estate agents are also claiming the market has changed course amid falling mortgage rates.

Ed Phillips, chief executive of estate agent Lomond said: ‘While we’re yet to see any notable jump in property values just yet, market momentum is building, with a firm foundation now laid to facilitate further growth as we head into what is traditionally the busiest time of year.’

Marc von Grundherr, director of Benham and Reeves said: ‘As we approach the spring selling season a very marginal decline in the monthly rate of house price growth should be viewed as nothing more than the market pausing for breath before the floodgates open.

Verona Frankish, chief executive of online estate agent Yopa added: ‘The appetite of the nation’s homebuyers may have been dampened by higher mortgage rates, but it certainly hasn’t disappeared, as demonstrated by the improvements seen in mortgaged approved house prices seen in recent months.

‘With the seasonal spring surge in market activity also imminent, it’s only a matter of time before we see the UK property market shift up a gear with respect to both sales volumes and house price growth.’

What next for the base rate?

Between December 2021 and August 2023, the Bank of England increased base rate from 0.1 per cent to 5.25 per cent, in a bid to curb rising inflation.

But the Monetary Policy Committee has now changed tact and has opted to hold base rate on five consecutive occasions since September.

What it does next will very much depend on the rate of inflation. Its next meeting takes place on 9 May.

Markets are currently forecasting base rate to go no higher than where it is now. We’ve reached the peak so to speak.

But if inflation rises again or is more volatile than expected, then there is no reason why the Bank of England won’t raise the base rate higher.

The BoE still thinks consumer price inflation will ‘temporarily’ fall back to 2 per cent by April, as the impact of previous hikes take effect.

But CPI, which remained at 4 per cent in January, is forecast to rise back to 2.75 per cent by year-end and remain above the bank’s target of 2 per cent until 2027.

However, Bailey recently told the Treasury Select Committee that investor bets on interest rate cuts this year ‘were not unreasonable’.

The Governor had previously warned that expectations of a March base rate cut from its current level of 5.25 per cent were ‘premature’, driving forecasts back to mid-2024.

Bailey said: ‘The market is essentially embodying in the curve that we will reduce interest rates during the course of this year.

‘We do not endorse the market curve. We are not making a prediction of when or by how much [we will cut rates],’ he said before adding: ‘it’s not unreasonable for the market to think about’ reductions in borrowing costs.

What mortgage deal should you choose?

Five-year fixed rate mortgages were once the most popular type of mortgage deal.

Now, increasing numbers of borrowers are opting for two-year fixed rate deals in the hope that interest rates will have fallen by the time they come to refinance.

There have also been a higher numbers of borrowers going for tracker mortgages that typically come without early repayment charges and track the base rate.

Although mortgage rates are higher than many people are used to, it may still pay to switch, especially if you are on your lenders’ standard variable rate.

And for those coming to the end of a fixed term, switching to another fixed term could be cheaper than sticking with their existing one.

It’s also worth considering sticking with your current mortgage lender by what is known as a product transfer. Figures shared exclusively with This is Money showed borrowers are securing better rates by staying put.

Choosing what length to fix for depends on what you think will happen to interest rates during that time, and what your personal circumstances are – for example if you will need to move.

Those opting for a two-year fix are essentially hedging their bets on interest rates falling over the next couple of years.

They’ll be banking on the expectation that once inflation subsides, interest rates will come down.

Fixed rates of any length also offer borrowers certainty over what their payments will be from month-to-month.

If rates do begin falling, a tracker mortgage without an early repayment charge could put borrowers in a position to take advantage.

However, for all the potential benefit, a tracker product will also leave people vulnerable to further base rate hikes in the meantime.

Whatever the right type of mortgage for your circumstances, shopping around and speaking to a good mortgage broker is a wise move.

For a full rate check use This is Money’s mortgage finder service and best buy tables. These are supplied by our independent broker partner London & Country.

Best fixed-rate mortgage deals

We have taken a look at the best deals on the market based on a 25-year mortgage for a £290,000 property – the current UK average house price according to the ONS.To check up-to-the minute rates based on your own circumstances, use This is Money’s mortgage finder service and best buy tables.Please bear in mind that the mortgage deals listed below are for those those buying and moving home, The rates for first-time buyers and those remortgaing may be slightly different.Also bear in mind that the mortgage deals below are best in terms of having the lowest rate. They may not be the cheapest deal overall when arrangement fees are also factored in.

Bigger deposit mortgages

Five-year fixed rate mortgages

Allied Irish Banks (AIB) has a five-year fixed rate at 4.09 per cent with a £200 fee at 60 per cent loan to value.

NatWest has a five-year fixed rate at 4.19 per cent with a £1,495 fee at 60 per cent loan to value.

Two-year fixed rate mortgages

MPowered Mortgages has a 4.52 per cent fixed rate deal with a £999 fee at 60 per cent loan-to-value.

Halifax has a two-year fixed rate at 4.6 per cent with a £1,099 fee at 75 per cent loan to value.

Mid-range deposit mortgages

Five-year fixed rate mortgages

AIB has a five-year fixed rate at 4.29 per cent with a £200 fee at 75 per cent loan to value.

Halifax has a five-year fixed rate at 4.36 per cent with a £1,099 fee at 75 per cent loan to value.

Two-year fixed rate mortgages

MPowered Mortgages has a 4.57 per cent fixed rate deal with a £999 fee at 75 per cent loan-to-value.

Halifax has a two-year fixed rate at 4.65 per cent with a £1,099 fee at 75 per cent loan to value.

Low-deposit mortgages

Five-year fixed rate mortgages

AIB has a five-year fixed rate at 4.61 per cent with a £200 fees at 90 per cent loan to value. This is specifically for home movers.

HSBC has a five-year fixed rate at 4.65 per cent with a £499 fee at 90 per cent loan to value.

Two-year fixed rate mortgages

The Cumberland Building Society has a two-year fixed rate at 5.07 per cent with a £1,060 fee at 90 per cent loan to value.

Coventry Building Society has a two-year fixed rate at 5.11 per cent with a £999 fee at 90 per cent loan to value.

>> Check our our mortgage tracker to compare the latest available deals

Tracker and discount rate mortgages

The big advantage to a tracker mortgage is flexibility.

The can sometimes be the case with discount rate mortgages, which track a certain level below the lenders’ standard variable rate.

A fixed-rate mortgage will almost inevitably carry early repayment charges, meaning you will be limited as to how much you can overpay, or face potentially thousands of pounds in fees if you opt to leave before the initial deal period is up.

You should be able to take a fixed mortgage with you if you move, as most are portable, but there is no guarantee your new property will be eligible or you may even have a gap between ownership.

Many tracker deals have no early repayment charges, which means you can up sticks whenever you want – and that suits some people.

Make sure you stress test yourself against a sharper rise in base rate than is forecast.

Getting a mortgage is tougher than it once was. You will need to get your finances in order and be prepared for the lengthier application process and in-depth affordability interviews getting a mortgage requires nowadays.

Lenders also apply different standards to what they will lend.

Weigh up the above, check the rates here and in our best buy mortgage tables, have a scout around what the best deals look like – and speak to a good independent broker.

There are a couple of things to look out for if you do decide to fix.

You need to check the bumper arrangement fees are worth paying – if you don’t have a big mortgage you may be better off with a slightly higher rate and lower fee.

It’s also wise to think carefully about whether you expect to move home soon. A good five-year fix should be portable, so you can take it with you.

But your new property will need to be assessed and you might need to borrow extra money, and so your lender could still say no. Getting out of a fixed rate typically requires a hefty hit to the pocket from early repayment charges.

[item name=standardModule id=310 style=310 /]

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

{kind=link}