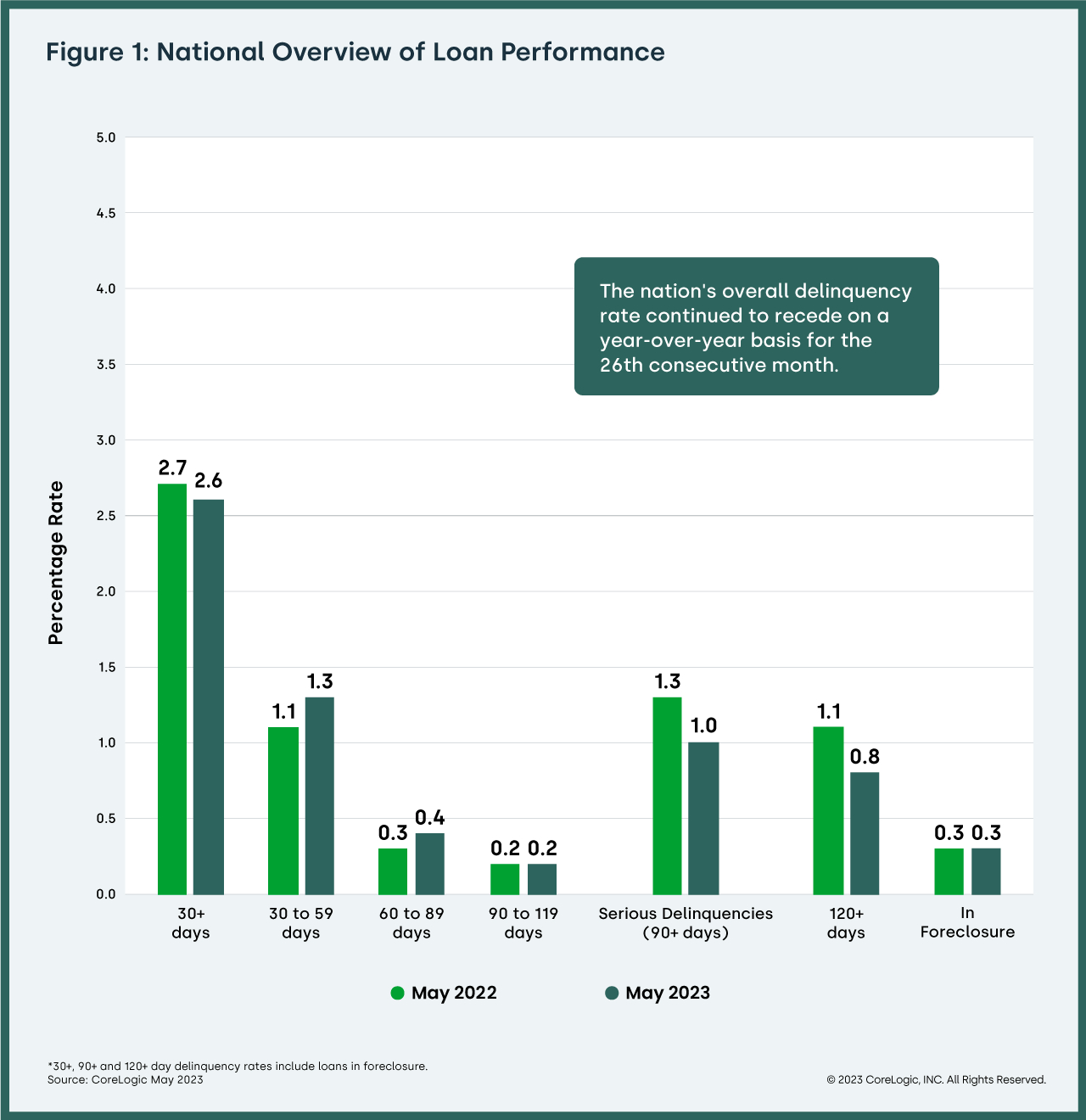

CoreLogic’s Loan Performance Insights Report found that, for the month of May 2023, 2.6% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 0.1 percentage point decrease, compared to 2.7% in May 2022, and a 0.2 percentage point decrease compared with 2.8% in April 2023.

CoreLogic’s Loan Performance Insights Report found that, for the month of May 2023, 2.6% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 0.1 percentage point decrease, compared to 2.7% in May 2022, and a 0.2 percentage point decrease compared with 2.8% in April 2023.

The U.S. overall mortgage delinquency rate again fell to a historic low in May, returning to the level seen in March of this year, while the near-all-time low foreclosure rate has not changed since spring 2022.

In May 2023, the U.S. delinquency and transition rates and their year-over-year changes, were as follows:

- Early-Stage Delinquencies (30 to 59 days past due): 1.3%, up from 1.1% in May 2022

- Adverse Delinquency (60 to 89 days past due): 0.4%, up from 0.3% in May 2022

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 1%, down from 1.3% in May 2022 and a high of 4.3% in August 2020

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.3%, unchanged from May 2022

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 0.6%, unchanged from May 2022

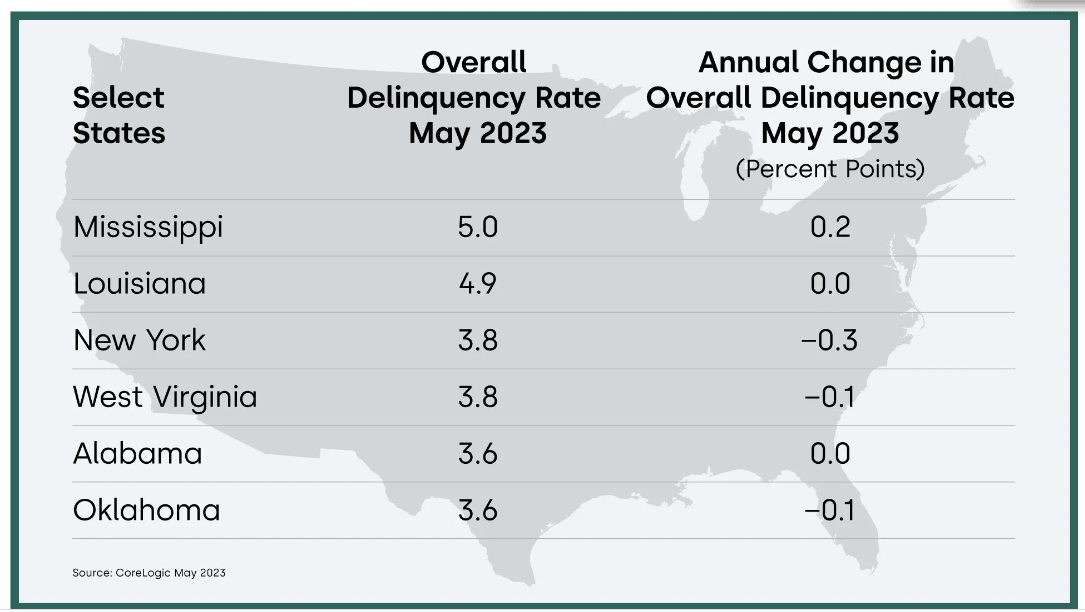

CoreLogic reports that 14 states and nearly 170 metropolitan areas saw overall delinquencies increase year-over-year in May, similar to April data. Still, despite this pattern and gradually declining U.S. home price gains over the past year, overall mortgage performance remains quite healthy, boosted by steady employment numbers.

“May’s overall mortgage delinquency rate matched the all-time low, and serious delinquencies followed suit,” said Molly Boesel, Principal Economist at CoreLogic. “Furthermore, the rate of mortgages that were six months or more past due, a measure that ballooned in 2021, has receded to a level last observed in March 2020.”

Fourteen states posted an annual increase in overall delinquency rates in May 2023. The states with the largest increases reported were: Idaho, Indiana, Michigan, Mississippi, and Pennsylvania (all up by 0.2 percentage points). An additional 14 states saw no change in overall delinquency rates year-over-year. The remaining states’ annual delinquency rates dropped between 0.3 and 0.1 percentage points.

In May 2023, 168 U.S. metro areas posted an increase in overall year-over-year delinquency rates. Elkhart-Goshen, Indiana; and Punta Gorda, Florida (both up by one percentage point) led the pack, followed by Cape Coral-Fort Myers, Florida; and Lubbock, Texas (both up by 0.9 percentage points).

Three U.S. metro areas posted an increase in serious delinquency rates (defined as 90 days or more late on a mortgage payment) in May, while changes in other metros ranged between -1.3% and 0.0%. The metros that saw serious delinquencies increase were Cape Coral-Fort Myers, Florida; and Punta Gorda, Florida (both up by 0.7 percentage points) and Elkhart-Goshen, Indiana (up by 0.2 percentage points).

“A very strong job market continues to help borrowers pay their mortgages on time,” Boesel continued. “The U.S. economy has added nearly 25 million jobs since April 2020 and about four million in the last year. As a result, the unemployment rate has ranged from 3.4% to 3.7% for the past 16 months. While the job market may slightly weaken over the next year, we project that mortgage performance will remain healthy.”

The data in CoreLogic’s Loan Performance Insights Report represents foreclosure and delinquency activity reported through May 2023. The data accounts for only first liens against a property, and does not include secondary liens. The delinquency, transition, and foreclosure rates are measured only against homes that have an outstanding mortgage. Homes without mortgage liens are not subject to foreclosure, and are, therefore, excluded from the analysis. CoreLogic has approximately 75% coverage of U.S. foreclosure data.

{kind=link}