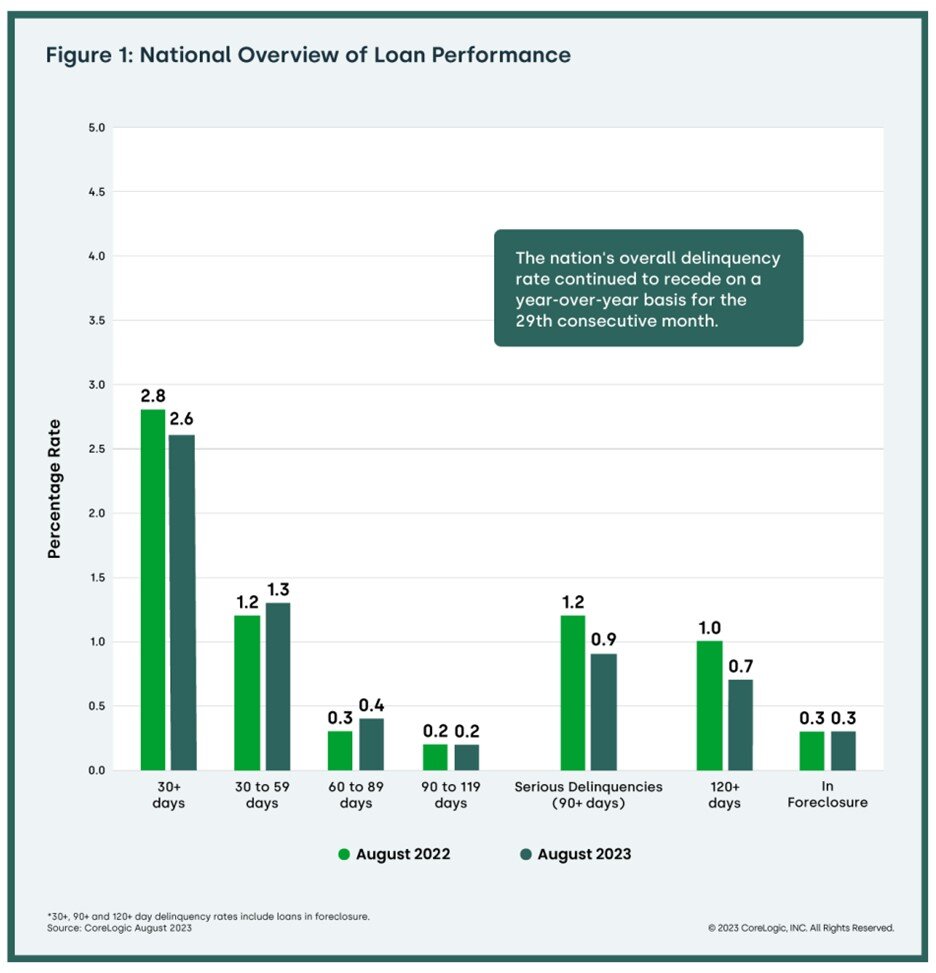

Based on CoreLogic’s latest monthly Loan Performance Insights Report for August, 2.6% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 0.2 percentage point decrease compared with 2.8% in August 2022 and a 0.1 percentage point decrease from July 2023.

To gain a complete view of the mortgage market and loan performance health, CoreLogic examines all stages of delinquency. In August 2023, the U.S. delinquency and transition rates and their year over-year changes, were as follows:

- Early-Stage Delinquencies (30 to 59 days past due): 1.3%, up from 1.2% in August 2022.

- Adverse Delinquency (60 to 89 days past due): 0.4%, up from 0.3% in August 2022.

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 0.9%, down from 1.2% in August 2022 and a high of 4.3% in August 2020.

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.3%, unchanged from August 2022.

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 0.6%, unchanged from August 2022.

The share of U.S. mortgages that fell into serious delinquency — representing borrowers who are three months late on payments — dropped to the lowest level in nearly 25 years in August, at 0.9%. Nationwide, overall mortgage delinquencies (2.6%) and foreclosures (0.3%) also remained near historic lows, a clear sign that most U.S. homeowners can currently cover their monthly payments. But as interest rates have approached 8% in October, more prospective buyers could be sidelined, a factor that makes timing the housing market crucial to building long-term wealth.

“U.S. mortgage performance remained strong in August, supported by a robust job market and a healthy economy,” said Molly Boesel, principal economist at CoreLogic. “However, this thriving job market comes at a time when interest rates are quickly rising, which is keeping many potential homebuyers from being able to secure a mortgage.”

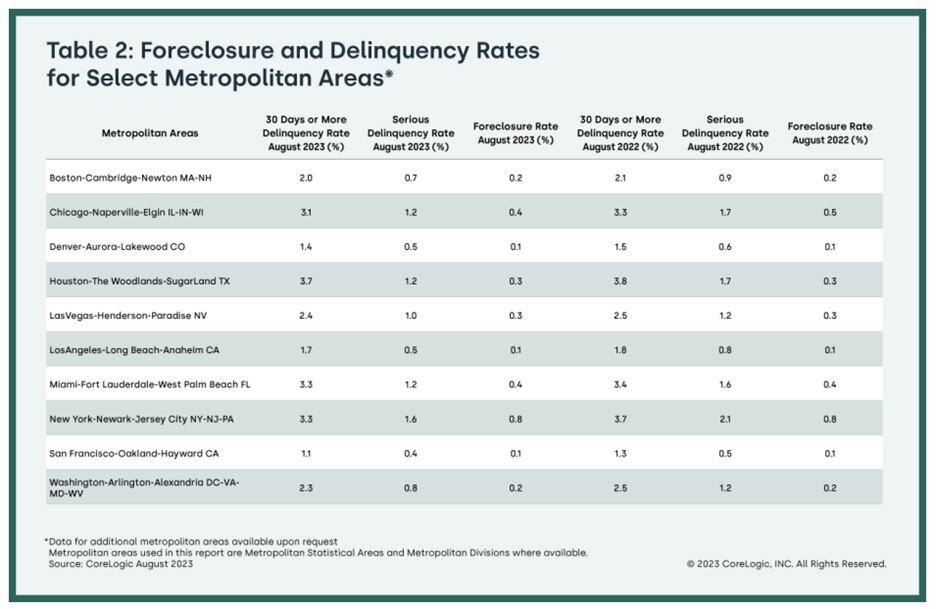

State and Metro Takeaways:

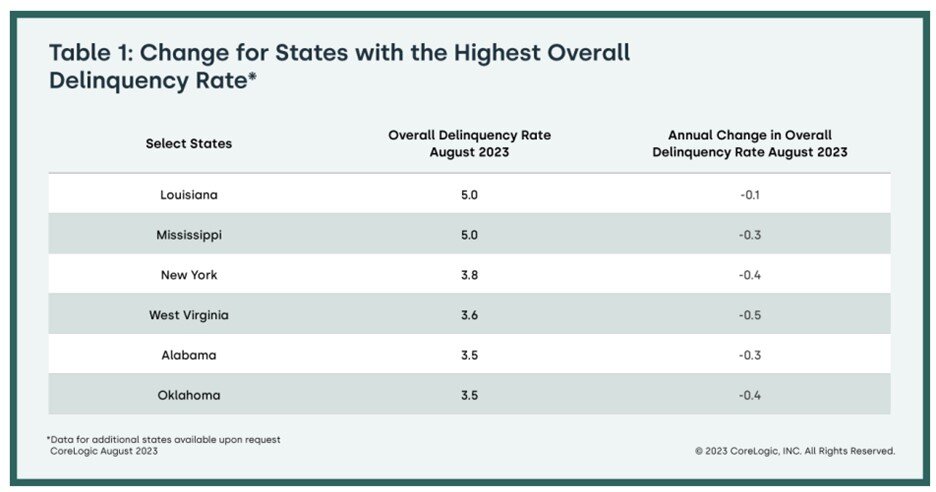

- Of U.S. states, Idaho and Utah posted small annual increases (both up by 0.1 percentage point) in overall mortgage delinquency rates in August. Overall delinquency rates were unchanged year over year in Arizona, Florida, Indiana and Oregon. The remaining states’ annual delinquency rates declined between 0.1 and 0.8 percentage points.

- In August, 51 U.S. metro areas posted increases in overall year-over-year delinquency rates. The metros with the largest increases were Elkhart-Goshen, Indiana (up by 0.6 percentage points); and Kokomo, Indiana and Punta Gorda, Florida (both up by 0.5 percentage points).

- In August, three U.S. metro areas posted an increase in serious delinquency rates (defined as 90 days or more late on a mortgage payment), while changes in other metros ranged from – 1.4 percentage points to 0.0 percentage points. The metros that posted annual serious delinquency increases were Punta Gorda, Florida (up by 0.5 percentage points); Cape Coral Fort Myers, Florida (up by 0.4 percentage points) and Cheyenne, Wyoming (up by 0.1 percentage point).

{kind=link}