Share to

WASHINGTON, D.C. (February 8, 2024) – The delinquency rate for mortgage loans on one-to-four-unit residential properties increased to a seasonally adjusted rate of 3.88 percent of all loans outstanding at the end of the fourth quarter of 2023, according to the Mortgage Bankers Association’s (MBA) National Delinquency Survey.

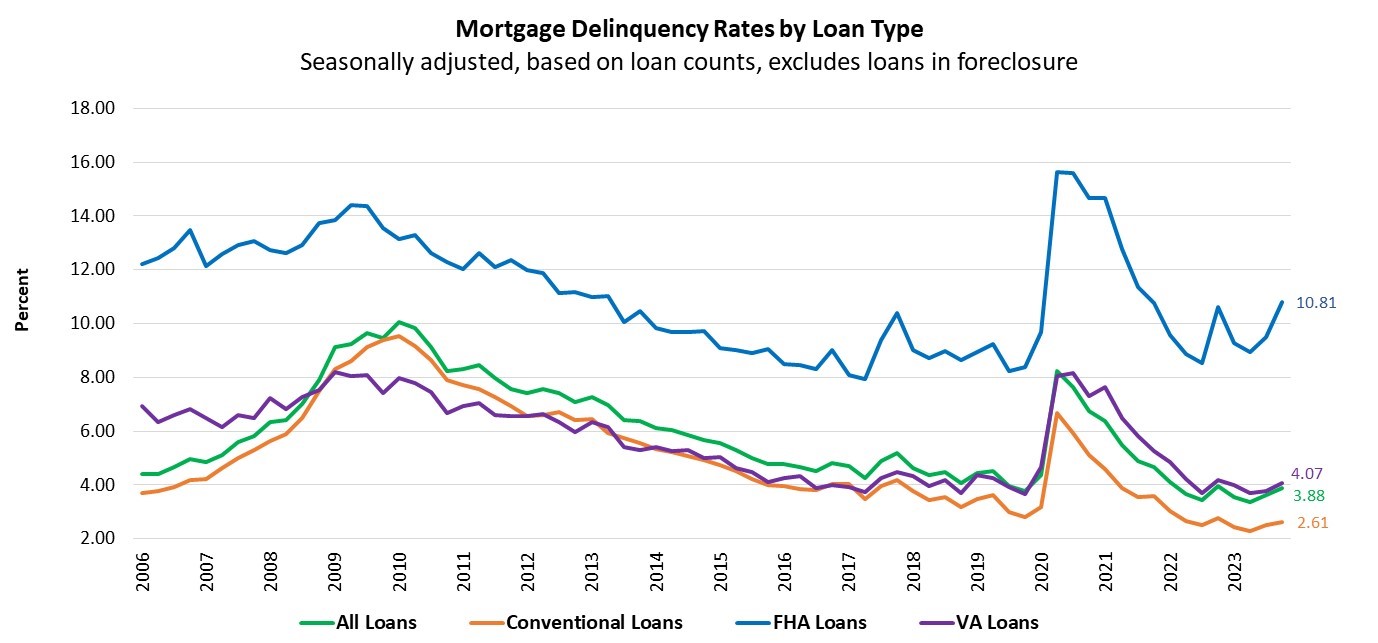

The delinquency rate was up 26 basis points from the third quarter of 2023 but down 8 basis points from one year ago. The historical average for the seasonally adjusted mortgage delinquency rate from 1979 through 2023 is 5.25 percent. Of particular note, FHA delinquencies were up 131 basis points.

The percentage of loans on which foreclosure actions were started in the fourth quarter remained unchanged at 0.14 percent.

“Mortgage delinquencies increased across all product types for the second consecutive quarter,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “While the overall delinquency rate is still very low compared to the historical average, the pace of new loans entering delinquency picked up and some loans moved into later stages of delinquency. The resumption of student loan payments, robust personal spending, and rising balances on credit cards and other forms of consumer debt, paired with declining savings rates, are likely behind some borrowers falling behind at the end of 2023.”

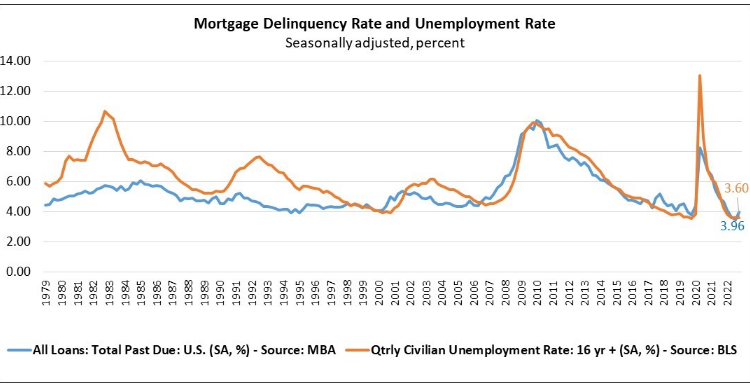

Added Walsh, “The labor market is still quite resilient with the unemployment rate – strongly correlated with mortgage performance – remaining at 3.7 percent in January. Any weakening in employment conditions would likely lead to more borrowers falling behind on their payments in the coming quarters.”

Key findings of MBA’s Fourth Quarter of 2023 National Delinquency Survey:

- Compared to last quarter, the seasonally adjusted mortgage delinquency rate increased for all loans outstanding. By stage, the 30-day delinquency rate increased 7 basis points to 2.10 percent, the 60-day delinquency rate increased 11 basis points to 0.73 percent, and the 90-day delinquency bucket increased 7 basis points to 1.05 percent.

- By loan type, the total delinquency rate for conventional loans increased 11 basis points to 2.61 percent over the previous quarter. The FHA delinquency rate increased 131 basis points to 10.81 percent, the highest level since the third quarter of 2021. The VA delinquency rate increased by 31 basis points to 4.07 percent.

- On a year-over-year basis, total mortgage delinquencies decreased for all loans outstanding. The delinquency rate decreased by 17 basis points for conventional loans, increased 20 basis points for FHA loans and decreased 9 basis points for VA loans from the previous year.

- The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure. The percentage of loans in the foreclosure process at the end of the fourth quarter was 0.47 percent, down 2 basis points from the third quarter of 2023 and 10 basis points lower than one year ago. This is the lowest foreclosure inventory rate since fourth quarter of 2021.

- The non-seasonally adjusted seriously delinquent rate, the percentage of loans that are 90 days or more past due or in the process of foreclosure, was 1.52 percent, matching the lowest level since 1984. It remained unchanged from last quarter and decreased by 37 basis points from last year. Compared to a year ago, the seriously delinquent rate decreased by 26 basis points for conventional loans, decreased 98 basis points for FHA loans and decreased 42 basis points for VA loans.

- The five states with the largest quarterly increases in their overall delinquency rate were: Louisiana (77 basis points), West Virginia (53 basis points), Illinois (44 basis points), Texas (44 basis points), and New Mexico (42 basis points).

- For the purposes of the survey, MBA asks servicers to report loans in forbearance as delinquent if the payment was not made based on the original terms of the mortgage.

NOTE: For non-seasonally-adjusted (NSA) supplemental information on the performance of servicing portfolios by investor type, loans in forbearance by investor type, and the status of post-forbearance workouts, as well as servicer call volume metrics, please refer to MBA’s Monthly Loan Monitoring Survey at www.mba.org/lms. January 2024 results will be released on Tuesday, February 20, 2024.

{kind=link}