When Rosario Lopez was looking to buy her first home last year, she knew her financing options were limited. She had been paid in cash, working as a security guard in Los Angeles, and didn’t have W-2s. Her credit history was short. So she wasn’t surprised when her bank, Bank of America Corp., told her she wouldn’t qualify for a mortgage.

Lopez, a single mother with three daughters, looked elsewhere. She found Miracle Lender Inc., a San Fernando Valley mortgage brokerage that pitches itself to Latino borrowers with social media advertising in Spanish. “Credit doesn’t matter,” a loan officer for the company says in an Instagram post.

Miracle Lender found a way to get a mortgage for Lopez without involving a bank. It arranged a $412,000 government-backed loan through GenHome Mortgage Corp., a nonbank lender, so Lopez could buy a four-bedroom ranch-style house in Lancaster, a city about 70 miles north of Los Angeles.

But the deal would cost her. She paid $21,533 in total fees, federal data show. That included almost $10,000 in origination charges that went to the lender and broker, as itemized in her mortgage documents, five times the average amount paid by traditional bank borrowers for loans of the same type and similar size in Los Angeles County last year. Most eye-popping: an $8,275 fee for Miracle Lender.

“It’s a lot,” Lopez says of the fees. “But it’s the only way I can get a house.”

Over the past several years, millions of Americans have faced a similar choice as commercial banks pulled back from the $12 trillion US residential mortgage market. They left borrowers to navigate an opaque and complex financial ecosystem dominated by nonbank lenders that don’t take deposits like traditional banks, operate mostly online and are subject to fewer federal regulations. These lenders depend on fee income more than banks, and they often work with independent service providers, including mortgage brokers, which can add to borrowers’ costs. The result: Homebuyers with the least means, often Black or Latino, pay higher fees.

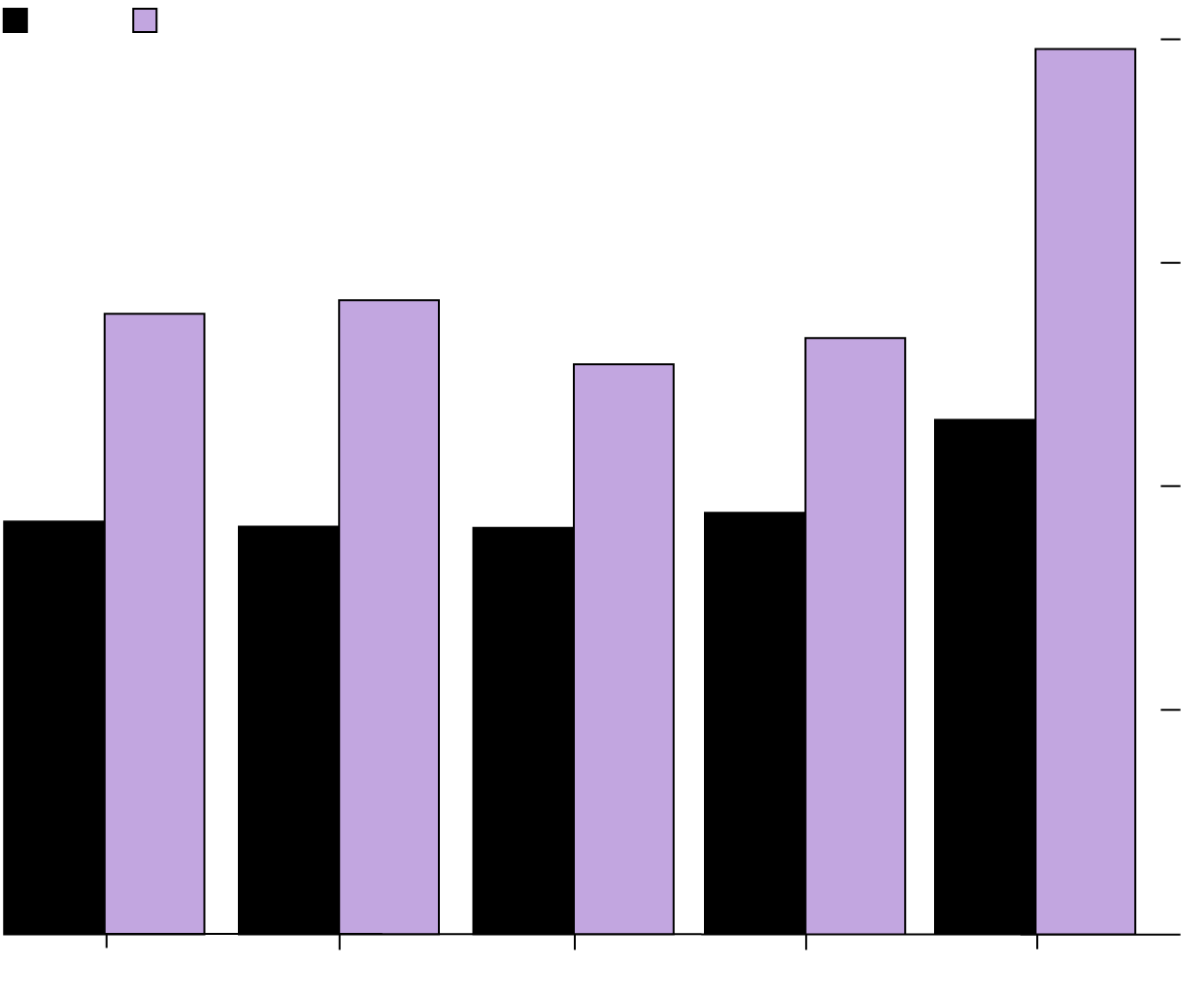

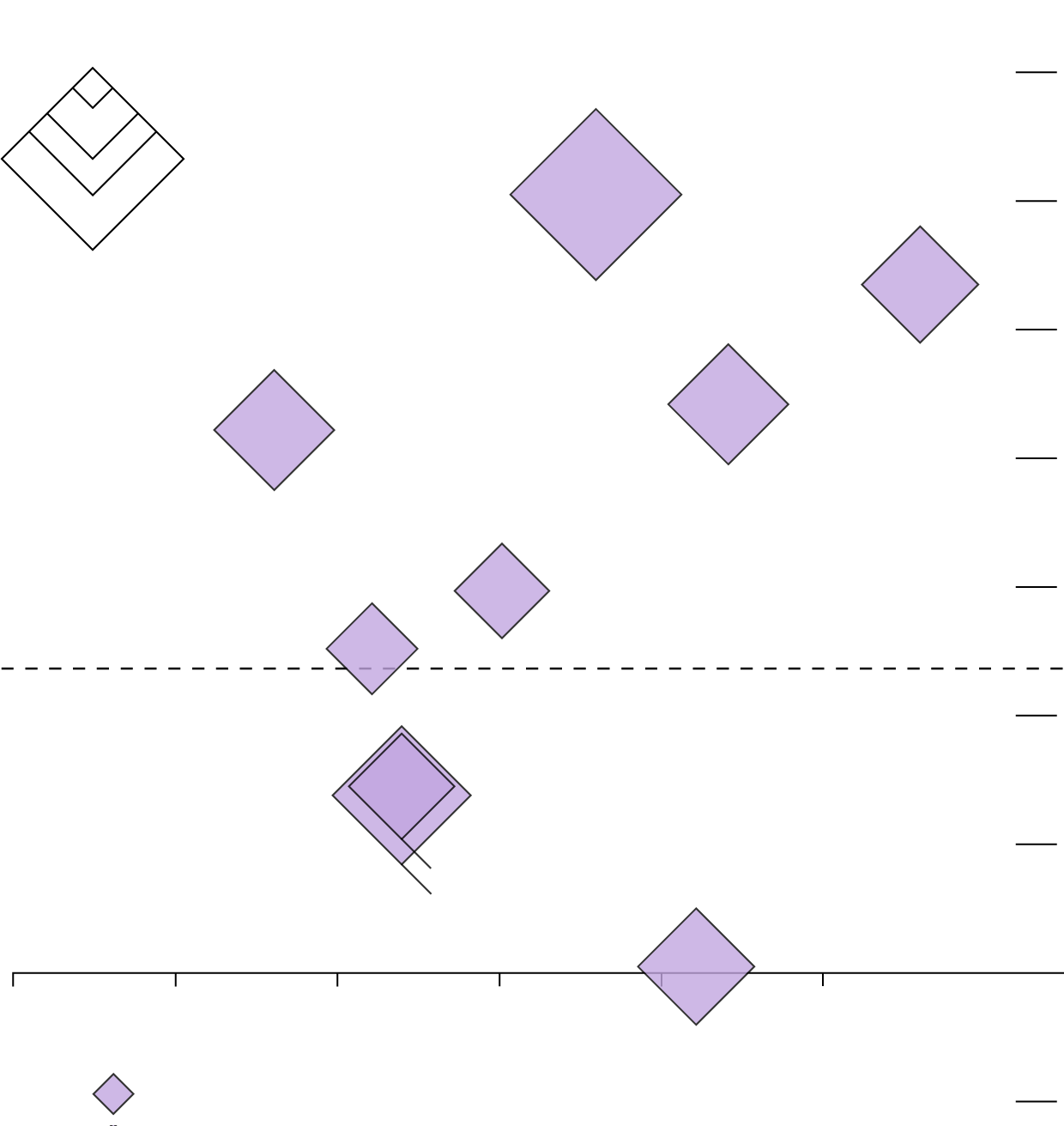

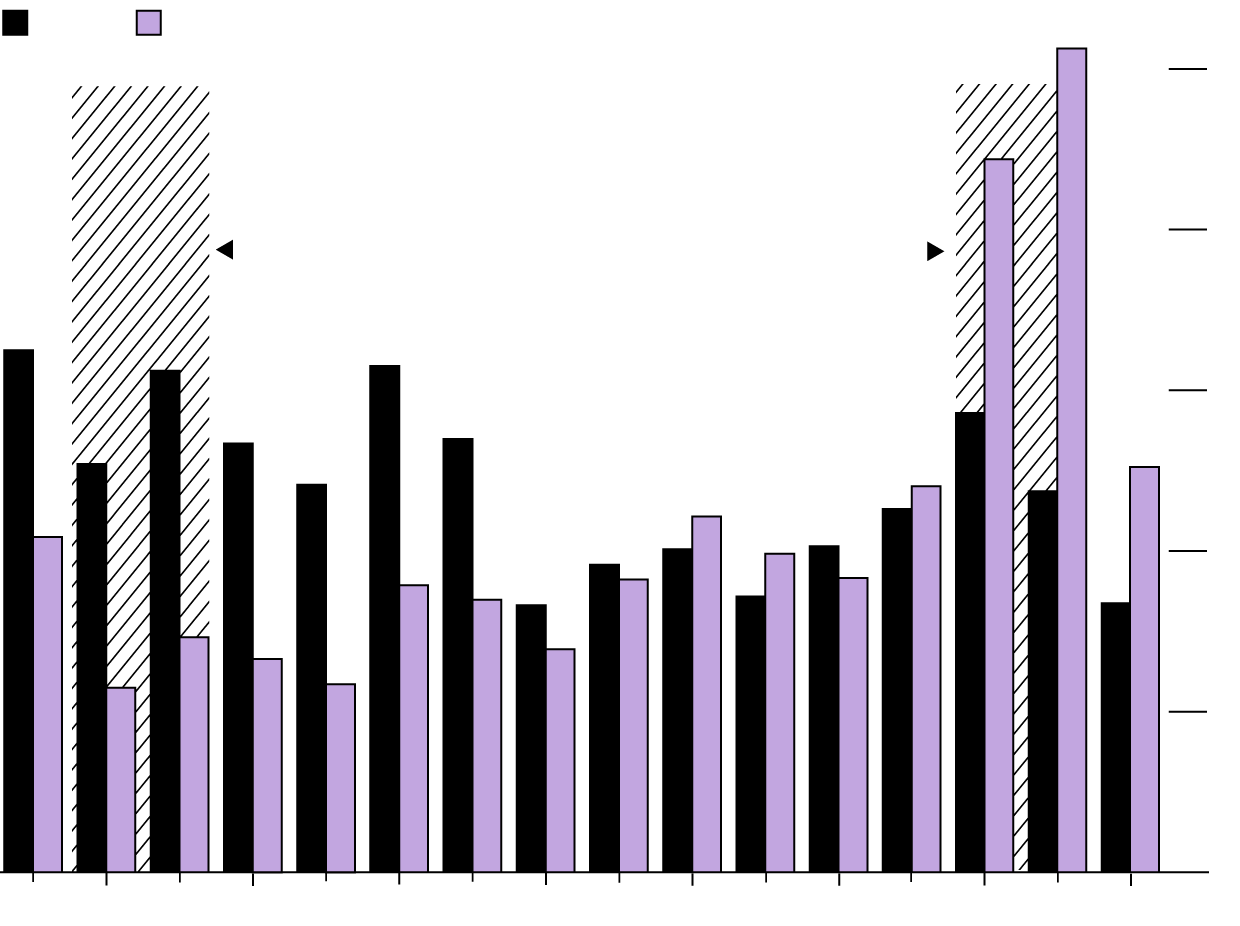

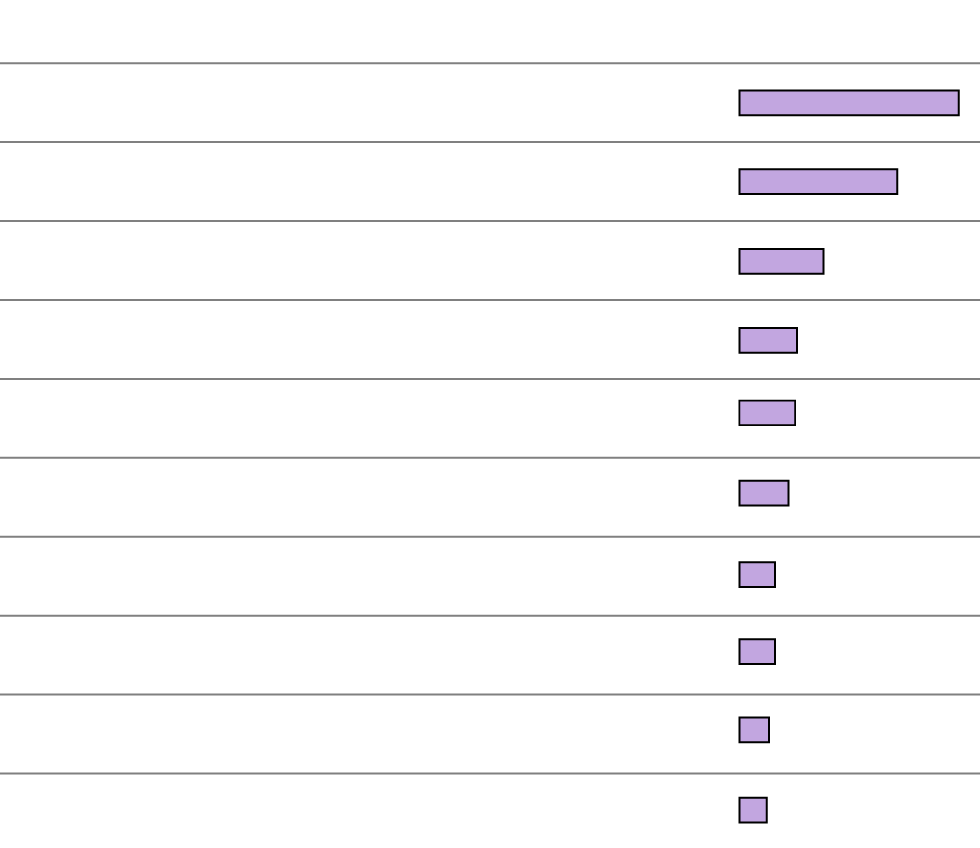

Nonbank Borrowers Paid Higher Fees

Average total loan costs by type of lender

Note: The CFPB started releasing data in 2018 on fees borrowers pay when obtaining mortgages. The bureau defines total loan costs as the sum of origination charges (lender and broker fees) plus third-party charges (appraisals, credit reports and title insurance).

Source: Home Mortgage Disclosure Act data compiled by Consumer Financial Protection Bureau, 2018–2022

Nonbank lenders say they offer home loans to people who can’t otherwise find financing, often with complicated situations that can add to costs. Yet even among comparable borrowers, those who use nonbank lenders tend to pay higher fees.

A Bloomberg News analysis of more than 38 million mortgages originated from 2018 through 2022 found that homebuyers with comparable incomes and loan sizes paid about $300 more in total upfront fees on average if they borrowed from nonbank lenders instead of traditional banks. There was a racial and ethnic penalty too: Latino homebuyers who used nonbanks to get the most common type of mortgage paid $230 more on average than comparable White nonbank borrowers, and Black borrowers paid $150 more, the analysis found. That disparity was smaller for Latino bank customers, about $40, and nonexistent for Black homebuyers who got loans from banks.

Note: Bloomberg used a multiple linear regression analysis to calculate the difference in total loan costs by lenders for Latino, Black, Asian and White borrowers of comparable characteristics including income, interest rates, loan size, down payment and debt-to-income ratio.

Source: Home Mortgage Disclosure Act data compiled by Consumer Financial Protection Bureau, 2018–2022

The amounts are small compared with the price of a home, but they add up over millions of mortgages. In the five most recent years for which data are available, nonbanks originated about 60% of US home loans, generating $71 billion in fees, about three-quarters of all charges collected by lenders and brokers.

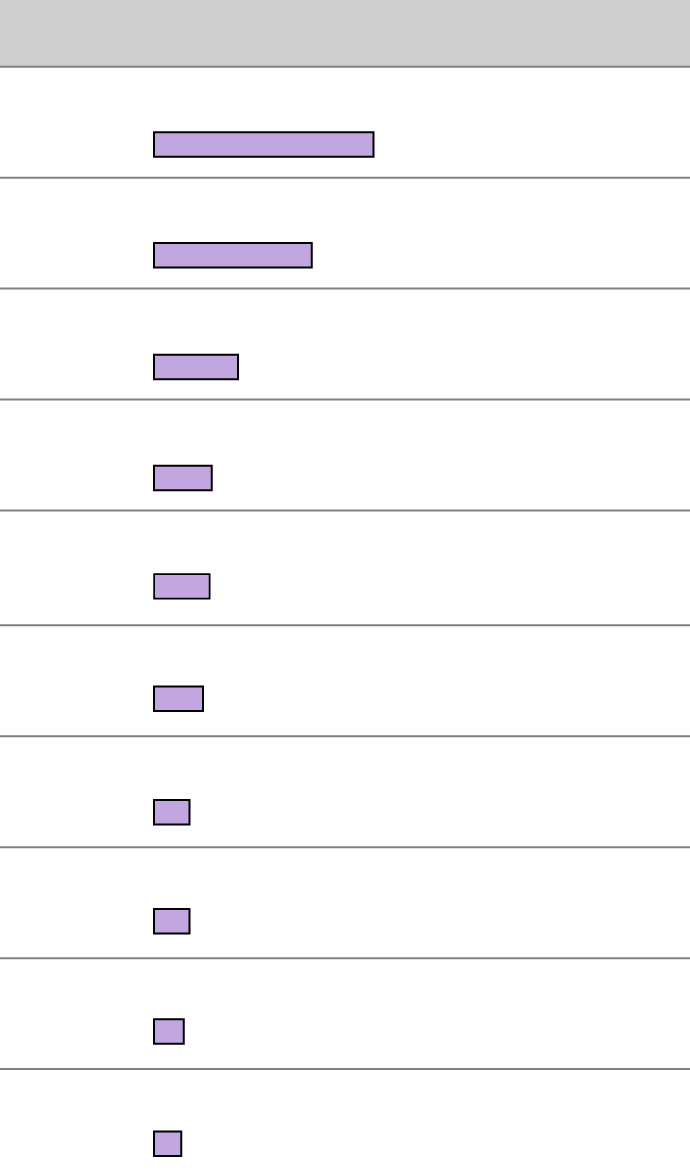

The racial and ethnic disparities tend to be higher in areas with large Latino or Black populations. In Los Angeles County, where more mortgages were issued to Latino homebuyers than in any other county over the five-year period, the fee gap between comparable Latino and White nonbank borrowers was twice the national average.

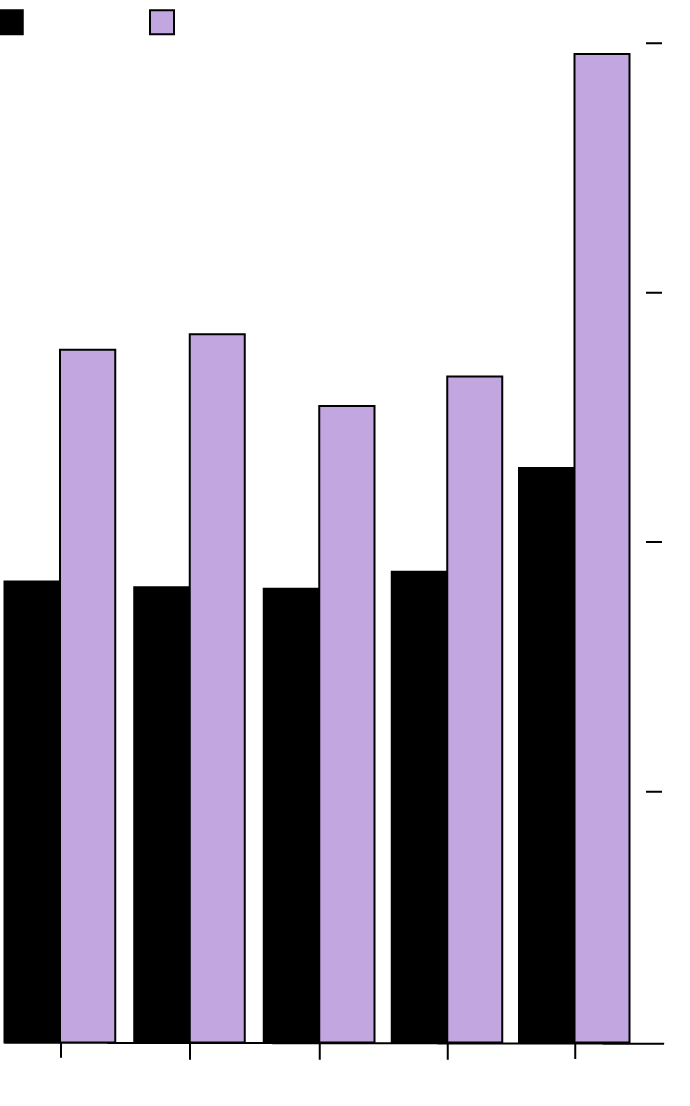

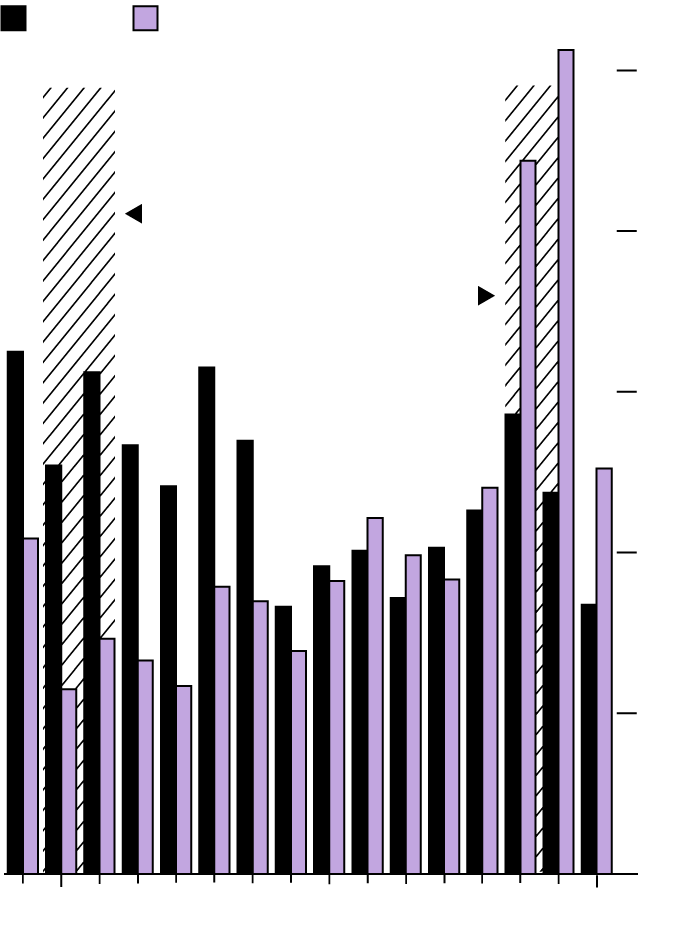

California Counties With Most Latino Homebuyers Had Widest Fee Disparities

Gaps between comparable Latino and White nonbank borrowers in top 10 counties

Note: Bloomberg calculated the difference in total loan costs for Latino and White nonbank borrowers of comparable characteristics such as income, interest rates, down payment and debt-to-income ratio in the 10 US counties with the largest number of mortgage originations.

Source: Home Mortgage Disclosure Act data compiled by Consumer Financial Protection Bureau, 2018–2022

“They’re paying higher fees, and those are the folks who actually need the help the most.”

“It’s reflective of this two-tiered system that we have, particularly in financial markets and banking around economic opportunity — this system where poor people have to pay more and it’s harder to get access to resources and opportunity,” says Deborah Archer, a law professor and director of the Civil Rights Clinic at New York University who also serves as president of the American Civil Liberties Union. “They’re paying higher fees, and those are the folks who actually need the help the most. These conditions that were created by systemic racial inequality are now used to justify further racial inequality and discrimination.”

Nonbank lenders say their pricing doesn’t discriminate on the basis of race or ethnicity and that any disparities in fees can be attributed to individual differences, which Bloomberg’s analysis doesn’t adequately take into account. They also say it’s unfair to look at mortgage fees without considering interest rates and that a borrower’s total payout over the life of a loan, including interest, is a better gauge of cost.

Greg Buchak, an associate professor of finance at the Stanford Graduate School of Business and one of three mortgage researchers who reviewed Bloomberg’s methodology and findings, says calculating that cost requires estimating how long a loan will be in place before it’s refinanced, or paid off, or the house is sold — variables that are hard to predict and based on formulas that neither banks nor nonbanks make public.

The average length of time US homebuyers keep their mortgages is eight years, according to one property-data provider, Attom. Using that figure, Bloomberg found that nonbank loans were more expensive than banks’ at every income level, even when accounting for the interest paid during the average life of a mortgage.

The fees examined by Bloomberg comprise the initial, upfront cost borrowers must pay to receive a loan. Those include both origination charges collected by lenders and brokers and those paid to outside parties including insurers, appraisers and lawyers. The analysis found that the gap in origination charges between banks and nonbanks was larger than the one in third-party fees.

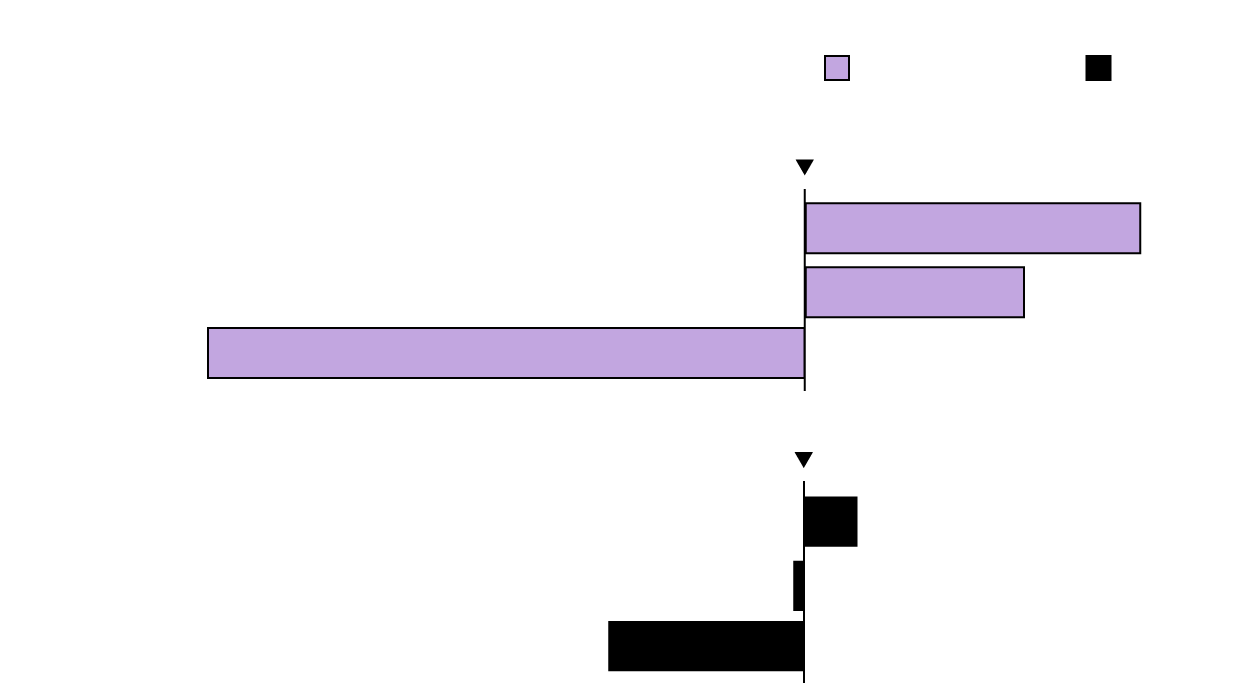

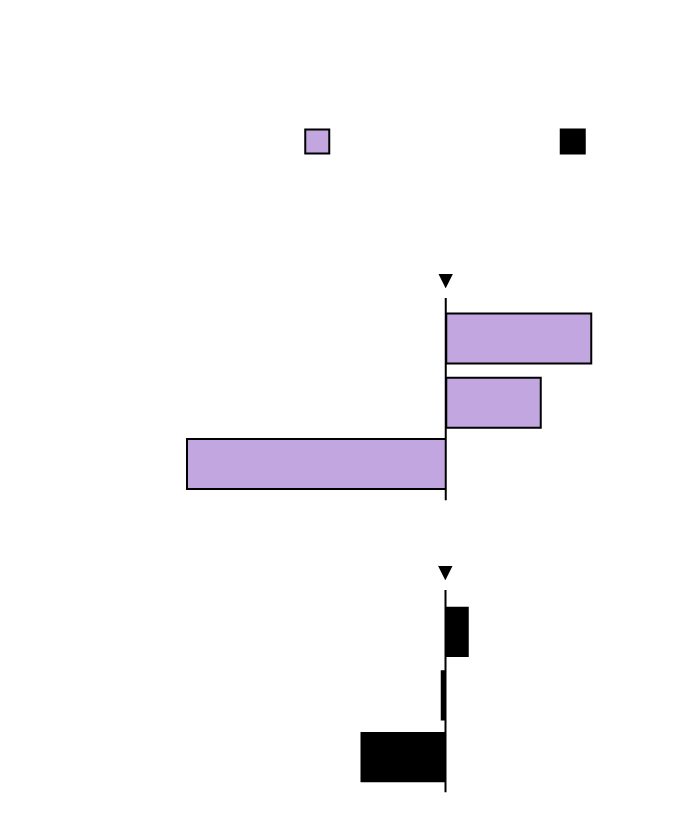

How Fees Pile Up

Some of the charges that appear on disclosure forms lenders are required to show borrowers

Source: Bloomberg

Bloomberg’s analysis relies on a widely accepted statistical tool called multiple linear regression analysis to determine the effects of the lender type and the borrowers’ race played in determining fees while holding differences in income, loan amount and other variables constant.

Credit scores, which lenders use to help set rates and some upfront fees, aren’t publicly available. But Bloomberg used another data point that measures the difference between a homebuyer’s interest rate on the day it was set and what a prime borrower would have paid the same week. The so-called rate spread is highly correlated with borrowers’ credit scores, according to the Consumer Financial Protection Bureau (CFPB), the lone federal agency that monitors nonbank lending practices. The agency declined to comment on Bloomberg’s findings, but its 2015 rules governing the Home Mortgage Disclosure Act say that analyzing upfront fees has “significant utility” in fair-lending analysis.

The bureau’s own annual studies of mortgage trends have found racial and ethnic fee disparities, though they haven’t accounted for how borrowers’ income and other characteristics affect those charges or compared fees at different types of lenders. In its latest report, based on 2022 data, the bureau found that Black and Latino homebuyers paid as much as 48% more, on average, than White and Asian borrowers.

Alexei Alexandrov, a senior adviser at the Urban Institute and a former chief economist for the Federal Housing Finance Agency who also reviewed Bloomberg’s work, says consumers are at a disadvantage when it comes to what is typically the largest and most stressful expense in their lives. “Mortgages are extremely hard to shop for because consumers don’t do the complicated math in their heads,” Alexandrov says. “I don’t know how anyone can expect people to do it.”

For Buchak, it’s all about asymmetry of information. “You go through this whole process, and then at the very end you get a piece of paper that says this is what you owe us,” he says, referring to mortgages from both banks and nonbanks. “And some of those things, you never saw before. These lenders have market power, and if they know you won’t search for a better deal, they charge you a higher price.”

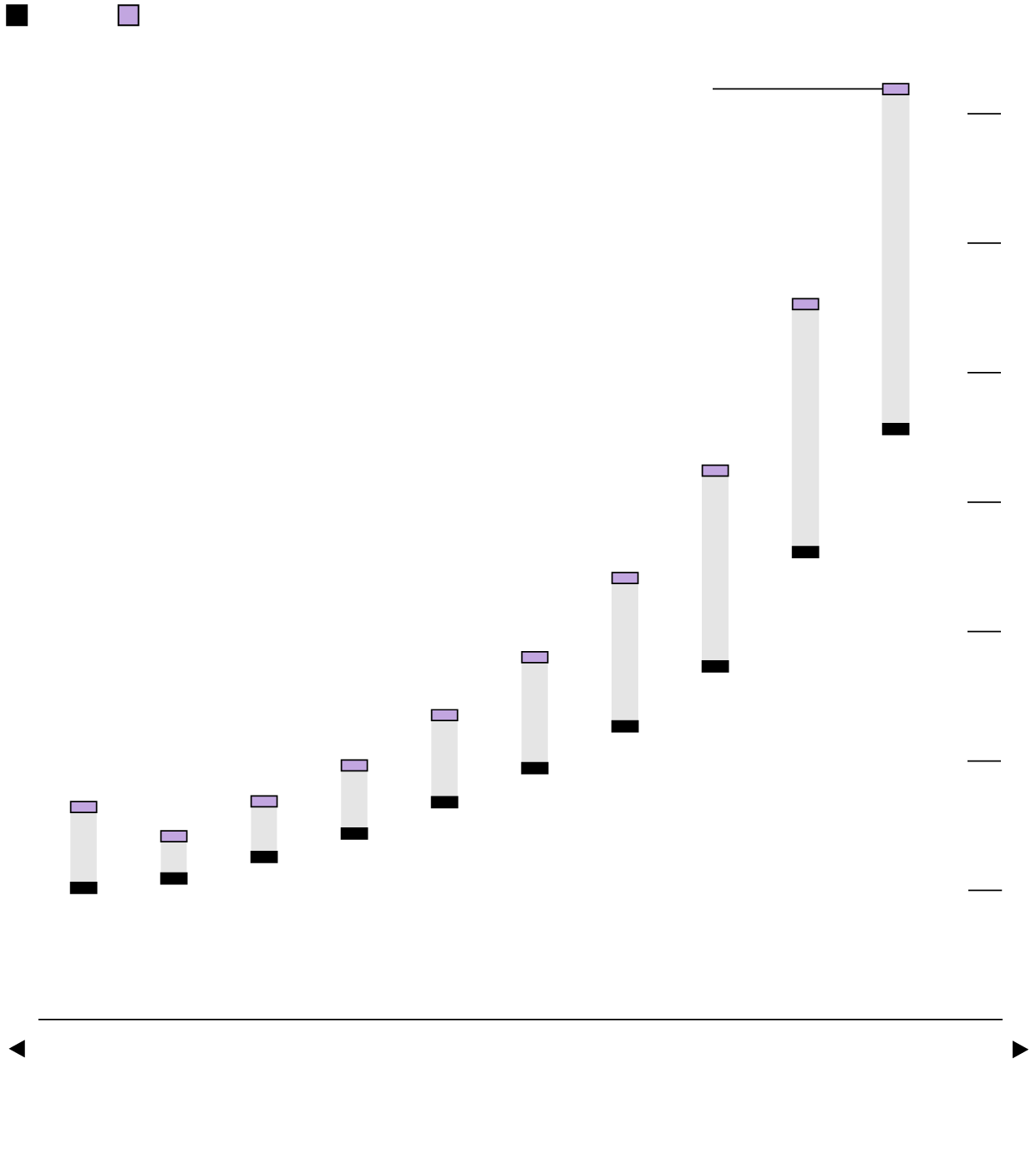

For generations, would-be homeowners turned to traditional banks, which originated about 70% of all US mortgages and refinancings from 2007 through 2013. Then, as new regulations took effect after the financial crisis, big banks including Wells Fargo & Co., JPMorgan Chase & Co. and Bank of America retreated. Some cited low profit margins and high compliance costs.

Into the void rushed hundreds of nonbank lenders. By 2021, as historically low interest rates drove mortgage lending to heights not seen since before the Great Recession, the numbers had flipped and nonbanks were originating almost 70% of all US home loans. The proportion slipped to 60% last year, and their business suffered as rising mortgage rates dried up loan demand.

Nonbanks Dominate US Mortgage Lending as Banks Pull Back

Number of home-loan originations

Source: Home Mortgage Disclosure Act data compiled by Consumer Financial Protection Bureau, 2007–2022

Today, the biggest banks rarely lend to first-time, low-income borrowers. Nonbank lenders underwrote 90% of all Federal Housing Administration (FHA) mortgages last year, the type of government-insured loan that Lopez got. Bank of America originated just 1,008, or 0.1% of the total; a decade ago it was 28,000. A spokesman for the bank says it offers first-time buyers other types of affordable loans that aren’t backed by the government.

Big banks still make money from US mortgages, though it’s behind the scenes. A review of state records shows that the four largest US banks provided as much as $100 billion in credit lines to nonbank mortgage companies last year.

“If they are going to leave from Bank of America, who tells them, ‘I’m sorry, you don’t qualify,’ they are going to go to whoever qualifies them,” says Erika Toriz, executive director of Haven Neighborhood Services, a nonprofit consumer advocacy group in Los Angeles. “There are people who really want their dream of homeownership, and they do anything to achieve that dream.”

Erika Toriz, executive director of Haven Neighborhood Services in Los Angeles.

Photographer: Lauren Justice/Bloomberg

Achieving that dream has come at a price. Unlike banks, which can cross-sell other services such as credit cards, car loans and brokerage accounts, nonbank lenders rely more on what can seem like a dizzying array of charges. Bank borrowers also face rate-lock fees, funding fees and processing fees, but they pile up faster at nonbanks.

“Nonbanks can’t be banks,” says David Stevens, a former head of the Mortgage Bankers Association, which represents both bank and nonbank lenders. “They can’t compete on the lower cost of funds, but what they do provide is greater access to credit.”

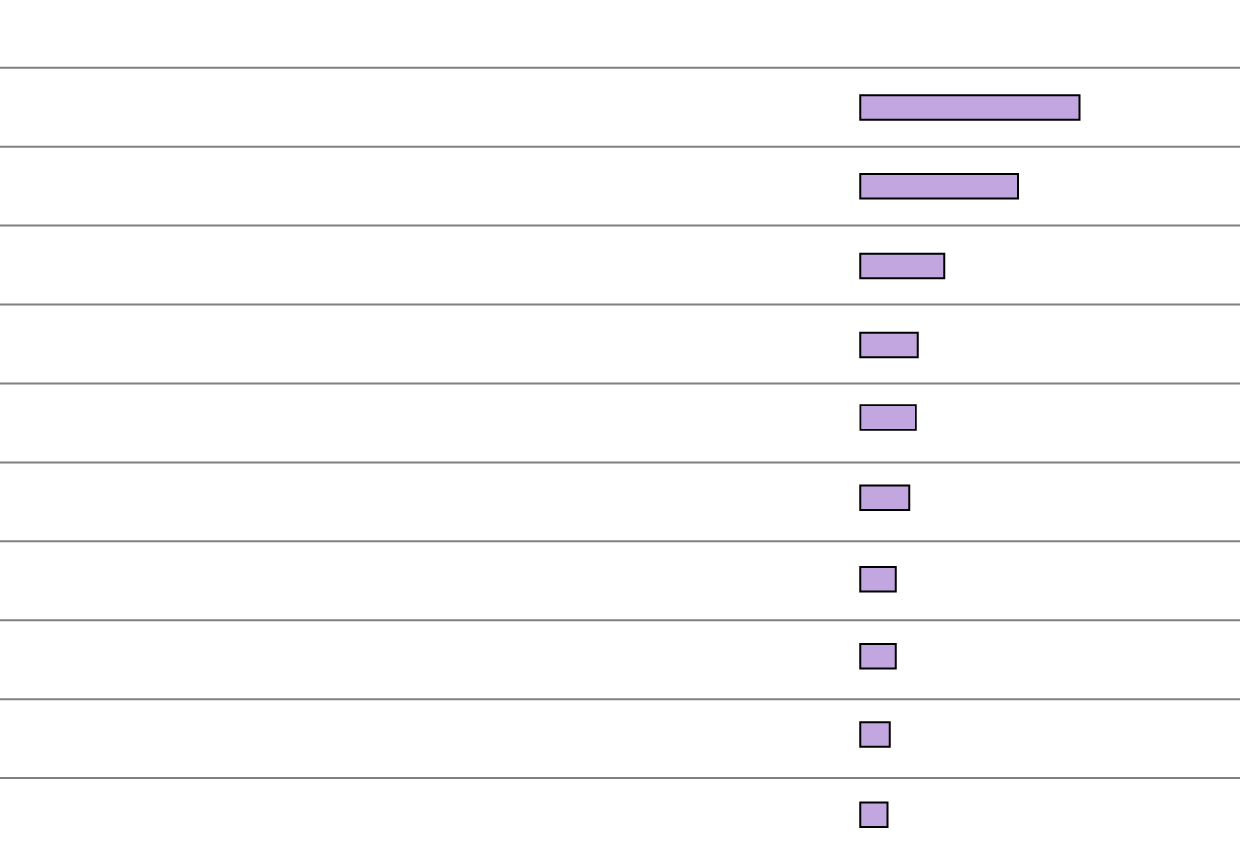

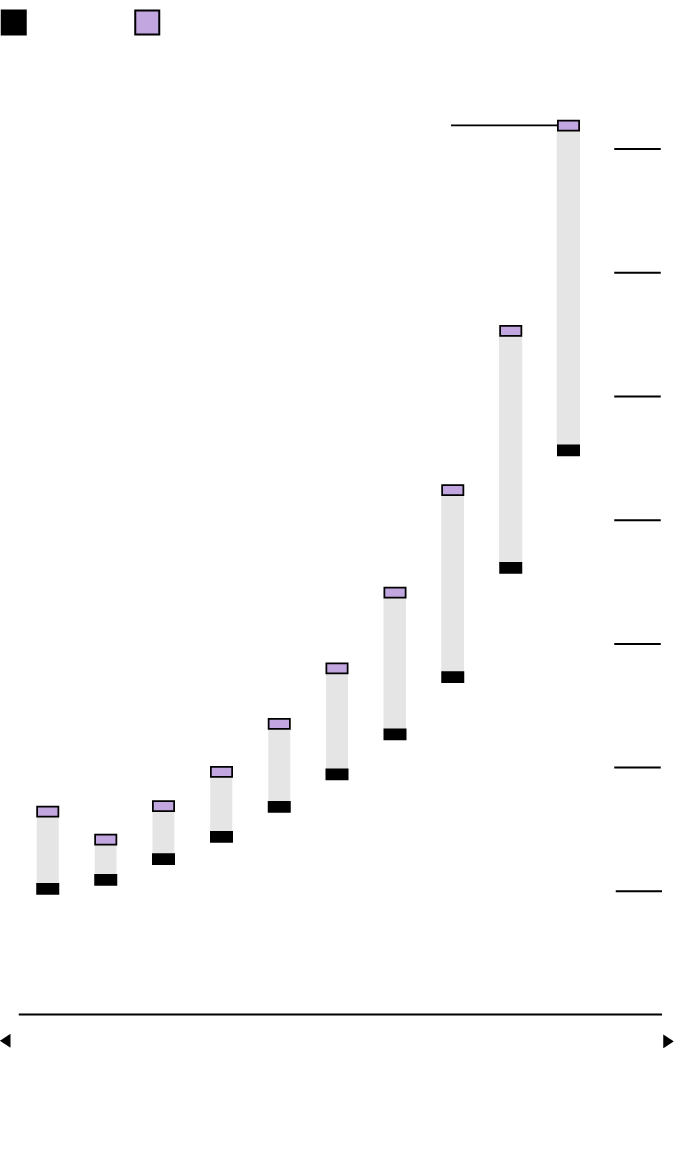

Top 10 Nonbank Lenders Originated $3 Trillion of Mortgages

By total loan amount, 2018–2022

Source: Home Mortgage Disclosure Act data compiled by Consumer Financial Protection Bureau

Federal rules cap origination fees on government-backed mortgages at 3% of the total loan amount. Lenders can originate loans with higher fees, but they must determine that borrowers can pay, and they’re prohibited from selling such loans to Fannie Mae, Freddie Mac or other government-sponsored entities. There’s also no limit on charges by brokers, realtors, appraisers and insurers who aren’t affiliated with the lenders.

Still, even after stripping out third-party fees, the disparities remain. Nonbank borrowers paid 22% more on average in origination charges than bank borrowers who bought similarly priced homes, received comparable interest rates and had similar incomes, debt loads and creditworthiness, Bloomberg found. Among nonbank customers, Latino and Black borrowers paid an average of $170 and $120 more in origination charges, respectively, than White homebuyers.

In some individual cases — say, a mortgage with an $8,700 broker’s fee — documents shared with Bloomberg make it clear what’s driving the higher costs. But it’s difficult in the broader analysis to pin down reasons for the fee gaps. Not all charges are broken out in the public data, and some borrower characteristics, such as Lopez’s lack of W-2s and her credit score, aren’t provided at all.

Nonbank lenders say any analysis of fees that doesn’t include credit scores is unreliable. Lenders use those scores to help decide whether to approve mortgages and to set interest rates. They also can affect borrowers’ upfront fees, reflecting the risk of underwriting bad loans. That risk is greater for nonbanks, which had a higher percentage of loans rejected by government-sponsored entities than banks did from 2016 through 2022, federal data show.

Nonbank lenders also say homebuyers can agree to pay more upfront to secure lower rates, a tradeoff known as buying points. But Bloomberg’s analysis accounts for fees borrowers paid to lower their rates by including these amounts in its regression model.

To better understand the interplay between credit scores and rates, Bloomberg examined 11 million mortgages bought by Freddie Mac, which buys loans from lenders to support the mortgage market. An analysis of this data, which included credit scores and covered 2018 through the third quarter of 2022, showed that nonbanks offered higher interest rates than banks for home-purchase loans to borrowers with comparable credit scores — six basis points on average.

No Matter Their Rates, Nonbank Borrowers Paid Higher Fees

Average total loan cost per $100,000 mortgage, by rate spread

Note: Borrowers were divided into 10 groups based on their rate spread, the difference between a loan’s annual interest rate and the average prime offer rate for a comparable mortgage the same week the interest rate was set. The spread, calculated by the CFPB, provides insights into lenders’ rate-setting decisions, which are based on credit scores, macroeconomic conditions and other factors that aren’t available in HMDA data.

Source: Home Mortgage Disclosure Act data compiled by Consumer Financial Protection Bureau, 2018–2022

At least some of the fee disparity is rooted in how nonbanks operate. While most banks use their own loan officers to process mortgages, nonbanks rely more on outside sources, including real estate agents, unaffiliated brokers and housing developers to generate business. The arrangements overlap in ways that are not always clear or disclosed in the federal data. Some developers require that loans come from specific lenders. Some realtors also act as mortgage brokers, an arrangement known as double-dipping, which was prohibited for government-insured loans before last December.

To make matters more complicated, some nonbank lenders, such as United Wholesale Mortgage, use independent brokers, while others, like Guaranteed Rate Inc., have loan originators on staff. Rocket Cos. does both. Nonbanks say that whether a lender uses in-house or outside originators matters because brokers are more often compensated through fees, while in-house staff are paid in rates. (The federal data doesn’t specify which model a lender uses.)

Adam DeSanctis, a spokesman for the Mortgage Bankers Association, says nonbanks tend to offer borrowers a wider variety of loan types and terms, which create costs for them. “Fundamental differences in business models, product offerings and cost structures makes comparing aggregate loan pricing offered by banks and independent mortgage companies problematic,” he says.

Sarah DeCiantis, chief marketing officer for United Wholesale Mortgage, the second-largest US mortgage originator, said in an email that Bloomberg’s analysis is flawed because it doesn’t take credit scores and other variables into account. “Nonbank lenders lend to everyone who qualifies and thus more frequently lend to lower-income borrowers than banks do,” she wrote. “Common sense tells you that a higher risk profile would result in different fees, rates and overall cost of a loan.” She also said that upfront fees reflect different compensation structures and consumer choices, and don’t establish whether a borrower got a better or worse deal.

Rocket, the largest originator, referred Bloomberg to David Skanderson, a fair-lending analyst at Charles River Associates in Washington, who declined to comment about the findings. Guaranteed Rate also declined to comment.

Whatever the reasons for the disparities, higher fees can be a burden. “Closing costs are one of the biggest barriers to new homeowners,” says Jesse Van Tol, president of the National Community Reinvestment Coalition, a nonprofit group based in Washington. “Saving for a house is hard enough. When you are paying $5,000 more than other borrowers, it is a massive barrier.”

The mortgage that Kehinde Ojo and her husband got last year came with high fees and a high interest rate.

Kehinde Ojo

Moreno Valley, California

In many ways Ojo, a Nigerian-born manager of home-care aides at a medical staffing agency, was an attractive borrower. She had $140,000 to put toward a down payment on a home in Moreno Valley, 65 miles east of Los Angeles. She says she and her husband had a joint six-figure income, meaning they’d have an enviably low 20% debt-to-income ratio, with plenty of room to cover payments on the $523,000 mortgage they were seeking. There was just one wrinkle: Ojo had recently emigrated to the US and didn’t have a Social Security card.

The Ojos turned to Ray Ferguson, a loan officer at mortgage brokerage Bay Equity Home Loans, a unit of Redfin Corp., to arrange financing. Independent brokers are supposed to shop around for options, but Ojo recalls having few choices. Ferguson set her up with a loan from Newfi Lending with closing costs of $8,415. That was 24% higher than what banks in the area charged for similar mortgages.

The total included $4,600 to drop their interest rate by 0.875%, closing documents show. But even after the Ojos agreed to pay the additional money, Newfi gave them a rate of 8.75%, almost 2 full percentage points higher than the average that borrowers paid at the time they closed in October 2022.

Standing in the doorway of her new home as her son impersonates Super Mario behind her, Ojo says Ferguson told her she didn’t have many options.

A subdivision in Moreno Valley, California, 65 miles east of Los Angeles.

Photographer: Kyle Grillot/Bloomberg

“Mainstream banks, like Wells, Chase, BofA, I don’t think any of them do” loans like the Ojos’, says Ferguson, who told Bloomberg he typically gets paid 1% of the mortgage amount, in this case about $5,000. “In certain situations, you don’t have a choice.”

That is because mortgages like the one the Ojos got — loans where the borrower is missing documentation or other information — don’t meet Freddie Mac and Fannie Mae underwriting standards. These so-called non-qualifying mortgages typically have higher rates. But some mortgage brokers say that can be mitigated by a good credit score and a high down payment. Ojo says she had both.

“It’s not fair,” she says. She hopes she can get a more affordable mortgage after receiving a Social Security number. “When I have that, everything will fall back in place.”

A spokesperson for Newfi, owned by investment firm Apollo Global Management Inc., says the company can’t comment on specific borrowers but that it provides loans for people who might not be able to get a mortgage from a traditional bank. “We operate in a highly regulated industry at both the state and federal levels and follow all applicable laws,” the spokesperson says. “There are many important factors involved in the loan underwriting process that determine the total cost of a loan, which are not accounted for in the HMDA data set.”

Andres Maduro

Tampa, Florida

Like Ojo, Andres Maduro, 42, says he didn’t have much choice in picking a lender. When he found a $140,000 two-bedroom, two-bath Tampa townhouse he wanted to buy in 2019, the selling agent told him he’d have to get his government-insured mortgage from LoanDepot Inc., Maduro recalls. That made Maduro, a JPMorgan bank branch paralegal, uncomfortable, but he went along. “I didn’t want to lose the property,” he says.

Such an arrangement makes it difficult to shop around, and the $6,431 in closing costs that Maduro paid was 24% higher than the average amount banks in Tampa charged FHA borrowers, according to Bloomberg’s analysis. Fees levied by Irvine, California-based LoanDepot, the nation’s third-largest nonbank lender last year, were 25% higher on average for Latino borrowers like Maduro than for non-Latino White borrowers over the five-year period.

Because he wasn’t able to compare fees, Maduro had no idea they were high. But he says he wasn’t surprised. “The bank I work for, we are highly, highly regulated, and I know these fintechs are not,” Maduro says. “I think that’s where the American dream gets lost.”

A spokeswoman for LoanDepot didn’t respond to questions about Maduro’s fees but said in an email that the company is “committed to making homeownership more accessible and achievable for all families, especially the diverse communities of first-time homebuyers.”

Business relationships like the one that led Maduro to LoanDepot are not uncommon. Toriz at Haven Neighborhood Services in Los Angeles says many Latino borrowers don’t have strong ties to financial institutions. “They trust realtors more than their banks,” she says.

For nonbank lenders, whose loan officers and mortgage brokers court realtors to drum up business, that creates an opportunity. Those relationships can be confusing to borrowers, who don’t always know they can opt out of an agent’s recommendations.

That was the case with Annalie Echenique, who came to the US from Cuba in 2005 with dreams of owning a home. She was 20 and pregnant when she arrived in Miami, and the path to a down payment was a rigorous exercise in budgeting. “We eat at home,” she says. “We don’t go anywhere.”

Annalie Echenique

Homestead, Florida

Echenique managed to save about $300 a week working 14 hours a day as a lab supervisor. But when she wanted to buy a four-bedroom condo in Homestead, Florida, in 2021, her annual income was only $56,000 and her credit score 620. That made her a subprime borrower, meaning her best chance at financing was an FHA-insured mortgage.

Echenique says her realtor, Lina Miranda, had her sign an agreement indicating she’d work exclusively with her, as well as a specific independent mortgage broker. Echenique says the realtor told her she would lose a $5,000 deposit if she tried to shop around.

Miami-based mortgage broker D&F Lending Corp. received a $7,830 commission on the $285,000 mortgage it obtained for Echenique from Dallas-based Caliber Home Loans Inc., her closing document shows. Her total closing costs: $10,207. In Miami-Dade County, where Echenique lives, the gap in fees between comparable Latino and White nonbank borrowers was 90% more than the national average, Bloomberg found.

Caliber is owned by nonbank lender NewRez LLC, one of the five biggest US mortgage lenders. NewRez Chief Marketing Officer Zach Pardes says Bloomberg’s findings that nonbanks charge higher fees aren’t surprising. “This is due to flexibility in lending criteria, quicker approval processes and tailored solutions for borrowers who may not otherwise meet traditional depository requirements,” Pardes says. Neither Miranda nor Diana Aponte, owner of D&F Lending, responded to questions about the fees or whether the brokerage paid Miranda for Echenique’s business.

Annalie Echenique at her house in Homestead, Florida.

Photographer: Eva Marie Uzcategui/Bloomberg

Echenique says she learned a costly lesson: “If you can check with other brokers or other companies, do it.”

Federal law bans paying commissions in exchange for referrals by any party involved in a mortgage transaction. But there are exceptions. Developers and other affiliated businesses can steer homebuyers to lenders as long as they disclose their relationships. There’s no prohibition against mortgage brokers serving double duty as real estate agents and collecting a second check.

Rosario Lopez

Lancaster, California

That’s what Miracle Lender loan officer Jose Orellana did with Rosario Lopez. He referred her to a realtor from Citiwide Realty Group, which shares an address and operates under the same brokerage license, state records show. Orellana declined to comment about Lopez’s mortgage or his commission, but he defended his work helping people get loans. “There are not a lot of Spanish-speaking loan officers,” Orellana says. “So I tend to focus, essentially, on that, because I feel like there is a lack of education from the Latino community when it comes to home purchasing.” Alex Iglesias, who holds the license for both companies, didn’t respond to requests for comment.

Lopez speaks English, but for borrowers who don’t, multilingual loan originators like Orellana can be a lifeline to a financial industry that might otherwise be out of reach. A spokeswoman for Irvine, California-based GenHome, which provided the mortgage, said the loan was in compliance with all federal and state laws and that the fees were disclosed to the borrower. Miracle Lender declined to comment.

For the ACLU’s Archer, providing a lifeline doesn’t justify high fees. “They’re catching people at some of their most desperate moments, when people want and need this housing opportunity,” she says. “To charge exorbitant fees is really taking advantage of people at one of their most vulnerable times.”

Van Tol, the National Community Reinvestment Coalition president, says it’s all part of a pattern. “For many years, in a variety of ways, people of color and low-moderate income have paid more in ways that are not legitimate,” he says. “Those practices were called reverse redlining or predatory inclusion, where people in those communities were targeted for loans that had problematic features. The high fees are part of the evolution of how that happens.”

{kind=link}