When you apply for financing, like a credit card or loan, the lender that reviews your application is almost certain to check a copy of your credit report and credit score. With certain loans, like mortgages, a lender might review all three of your credit reports and scores from Equifax, TransUnion, and Experian.

Because your credit score matters to lenders, it’s wise to keep an eye on this information yourself. So, you want to make a habit of checking your credit score on a regular basis.

The guide below will show you how to check your credit score and understand the information you’re reviewing. You’ll also learn why there are so many different types of credit scores available, factors that can lower your credit score, and potential ways to improve this important three-digit number.

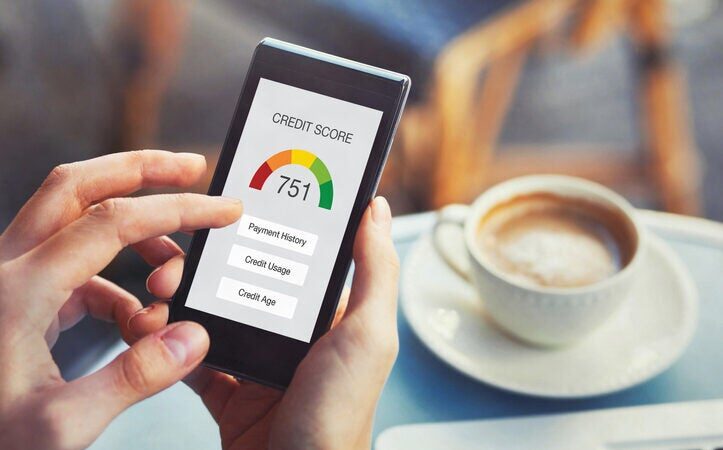

How do I read my credit score?

The best way to read your credit score is to try to understand what a lender sees when it reviews the same number. Most lenders in the United States use scores from FICO® and VantageScore that range from 300-850. The credit score you earn comes from an evaluation of your credit history and communicates how likely you are to pay your bills on time in the future.

A higher credit score indicates that you’re less likely to pay your credit obligations severely late (i.e., 90 days late or worse) in the next 24 months. A lower credit score, by contrast, indicates a greater likelihood you’ll pay a bill late or default on your debts.

The charts below provide a closer look at what your credit score range tells lenders about your creditworthiness.

Where can I find my credit score?

Before you start searching for your credit score, it’s important to understand a few key pieces of information. First, you need to know there’s a difference between credit reports and credit scores.

You have three credit bureaus that issue credit reports — Equifax, TransUnion and Experian. Free copies of these reports are available from AnnualCreditReport.com once a week through the end of 2023. (The Fair Credit Reporting Act ensures consumers get free access to these reports once every 12 months, even once the free weekly access expires.)

However, there are many different types of credit scores. Even though FICO® and VantageScore® are the two primary brands of credit scores that lenders use in the U.S., there are many different versions available. There’s also no federal mandate for consumers to have free annual access to their credit scores. So, finding your credit score can be more complicated.

Nonetheless, there are numerous places to find copies of your credit scores, including:

- Some credit card issuers.

- The credit reporting agencies (Equifax, TransUnion, Experian).

- MyFICO.

- Credit counseling agencies.

- Consumer-facing websites.

- Credit monitoring services.

Several of the options above may charge you fees to access your credit score. And certain credit monitoring services may charge recurring fees every month. So, be sure to read the fine print before entering your credit card information to purchase a credit score.

How to check your credit score

If you want to check a copy of your credit score (or credit scores based on all three of your credit reports), consider the following resources.

- Certain credit card companies offer free monthly credit score access to cardholders, including Discover, Chase, Capital One, and American Express (among others).

- MyFICO.com allows consumers to purchase copies of their three FICO® Scores and credit reports starting at $29.95 per month and up.

- Experian offers consumers free monthly access to their FICO® Score 8 and Experian credit report. Additional credit scores are available at an added cost.

- Equifax gives consumers free access to their VantageScore 3.0 credit score up to once a month through the Equifax Core Credit™ program.

- Credit monitoring programs are available online through various websites. Some are free, while others are fee-based. Free programs often offer limited options (e.g., fewer credit scores, non-FICO Scores, etc.) and you may have to agree to receive marketing for financial products.

What boosts my credit score?

When you understand the factors that influence your credit score, you can use that information to learn how to improve your credit score. Every situation is different. Yet here are some common credit-building strategies you might want to consider.

- Pay down credit card debt. For many people, paying down credit card debt represents an actionable way to improve your credit score. Credit scoring models place a big emphasis on credit utilization—the relationship between credit card limits and balances. When you pay down credit card debt, your credit utilization rate typically declines, which can positively impact your credit score.

- Fix credit errors. A study by the Federal Trade Commission found that one in five people have an error on their credit report. If a credit error is negative, it could drive your credit score downward. But the Fair Credit Reporting Act (FCRA) allows you to dispute mistakes on your credit report if they happen to you. You can use this free guide from the Consumer Financial Protection Bureau to dispute credit errors and try to remove them from your credit report.

- Establish positive credit history. In some cases, adding positive payment history to your credit report might be beneficial. If you’re working to build credit for the first time or rebuild damaged credit, you might want to consider whether secured credit cards, credit cards for people who are new to credit, or credit builder loans could be a good fit for you.

- Get credit for bills you already pay. There’s a good chance you already pay bills each month that don’t appear on your credit report. If so, you might want to consider using a third-party service like Experian Boost to get credit for any eligible rent, utility bills and subscription services you’ve been paying on time.

What brings my credit score down?

Mistakes can set back your credit-building efforts and cause a lot of frustration as you work to earn good credit. Here are three credit pitfalls you’ll want to avoid.

- Late payments: Payment history makes up 35% of your FICO® Score and 40% to 41% of your VantageScore (depending on the version). Not only do late payments have the potential to have a serious negative impact on your credit score, but those derogatory marks can remain on your credit report for up to seven years.

- High credit utilization: A high balance-to-limit ratio on your credit cards can lower your credit score even if you pay your bills on time every month. Credit utilization is a major factor that influences 30% of your FICO® Score. So, it’s important to avoid high credit card balances (in relation to your credit limits) if you want to protect your credit score.

- Applying for new credit in excess: There’s nothing wrong with applying for a new loan or credit card when you need one. But seeking new financing in excess could hurt your credit score. Plus, too many new accounts on your credit report in a short time period could reduce your average age of credit and that might also have a negative credit score impact.

Why it’s important to check your credit score

Good credit is a valuable asset. There’s always a chance you might need to rely on your credit for new financing or even something unexpected. And current creditors (like credit card issuers) often review your credit score for account maintenance purposes.

It’s smart to keep your credit in the best shape possible so it’s available whenever you need it. The best way to ensure your credit is ready when you need it is to review it regularly. Checking your credit reports is most important, but keeping an eye on your credit scores can give you more information about your credit health.

Frequently asked questions (FAQs)

In some cases, you may have to pay a fee to see your credit score. However, free credit scores may also be available in the following ways:

- Many credit card companies offer free credit scores to cardholders as a courtesy.

- Experian offers a free monthly FICO® Score to consumers.

- Equifax offers a free monthly VantageScore 3.0 credit score to consumers.

- You may receive a free copy of your credit score(s) from lenders when you apply for certain types of financing (e.g., a mortgage loan, auto loan, etc.).

- If you applied for credit and the lender denied your application, you may receive a copy of your credit score in the mail as part of an adverse action notice.

A credit report summarizes your credit history and the basis for your credit scores. These reports contain details such as your personal information, current and previous credit obligations, the dates you opened accounts, account balances, payment history, and more.

Consumer reporting agencies prepare your credit reports. The three major consumer reporting agencies in the United States, also known as credit bureaus, are Equifax, TransUnion, and Experian.

It’s wise to check your credit score several times a year and even monthly checks are not excessive. Yet it’s even more important to keep an eye on your credit reports from the three credit bureaus since those reports are the basis for your credit scores.

{kind=link}