LONDON, Nov 14 (Reuters Breakingviews) – The euro zone is a tale of two interest rates: the official one set by the central bank, and the ones earned by companies and individuals on their investments. The first is at record levels to cool the economy and curb inflation. That’s pushed up the private sector’s interest income, supporting growth. As more debts come due for refinancing next year, though, the economy may fare worse than expected.

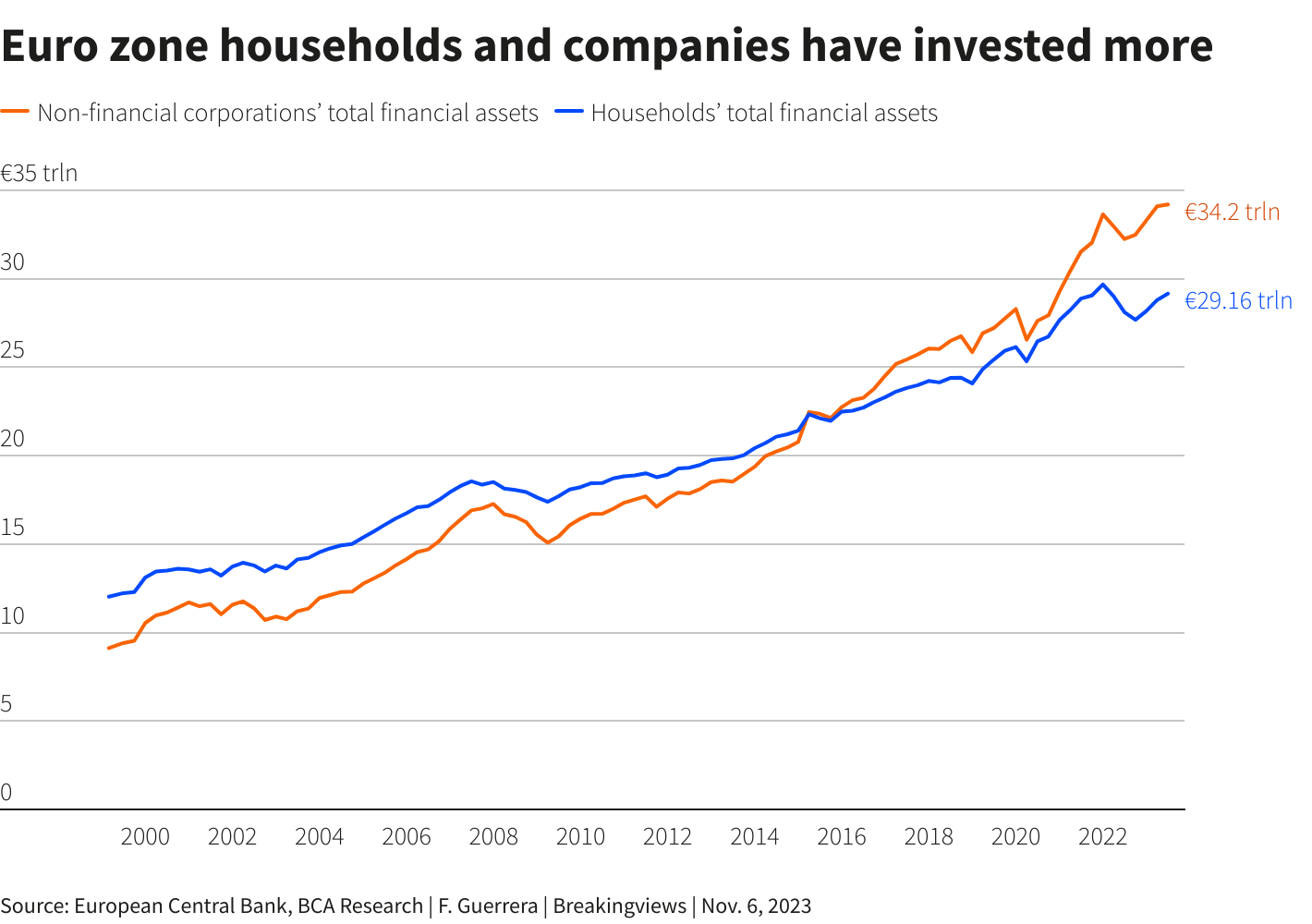

European citizens and corporations have been quietly stashing money in financial assets since the economic crisis of 2008. In the first quarter of 2009, euro zone companies, excluding banks and insurers, held financial assets of 15 trillion euros ($16 trillion), according to European Central Bank data. By the second quarter of this year, that figure had grown to a record 34 trillion euros. Over the same period, the total value of household assets, including deposits, currencies and shares, rose from 17 trillion euros to 29 trillion euros.

Both groups accumulated investments in the years after the crisis, but the tragic pandemic era accelerated that trend, thanks to fiscal stimulus and government handouts to households and firms. The private sector’s robust balance sheet has countered the ECB’s efforts to reduce soaraway inflation. Even as the central bank lifted its benchmark rate from minus 0.50% in July 2022 to a record 4% in just over a year, the euro zone economy proved resilient, growing by 3.4% last year. Though ECB staff expect growth to shrink to 0.7% this year, that is still better than the recession many economists previously predicted.

Private investment buffers may have delayed a contraction. Households paid 46 billion euros in interest on their borrowings in the three months to June – more than four times the level at the start of 2022, ECB data show. But the interest they earned on their assets increased from 16 billion euros to 66 billion euros in the same period. The resulting net interest income is the highest in 14 years, according to Mathieu Savary of BCA Research.

The windfall for households reflects the make-up of their balance sheets. Nearly 36% of citizens’ assets were in currencies and bank deposits, which tend to respond quickly to rate changes, while nearly all their liabilities were in the form of loans such as mortgages, which tend to have interest rates that are fixed for a while.

By contrast, non-financial companies derive most of their funding from shorter-term bank loans – nearly 80% of those have a maturity of less than one year, according to Oxford Economics. As a result, euro zone firms’ net interest was negative 19 billion euros in the second quarter of 2023. Even so, companies and households have pocketed 6 billion euros in net interest since 2020 and were still net recipients of interest payments of about 660 million euros in June this year.

These financial gains may have helped euro zone growth. Private consumer expenditure, which accounts for around half of the bloc’s GDP, rose by more than 4% a year in both 2021 and 2022, according to the International Monetary Fund, well above the 1% long-term average. Gross fixed capital formation, a measure of corporate investment that accounts for about a quarter of euro zone GDP, also grew much faster than usual in 2021 and 2022.

Some countries and companies were big beneficiaries. Take France, where household financial assets are 245% of GDP while liabilities total just 76% of economic output. Or look at oil giant Shell (SHEL.L), which saw its cash and short-term investments rise from $18 billion in 2019 to $40 billion in 2022, helped by resurgent crude prices, according to LSEG data.

But as higher rates bite, individuals and companies may have to tighten their belts. Firms will be first to receive higher interest bills. Nearly 45% of all the 1.4 trillion euros owed by European investment-grade companies comes due in 2024 and 2025, according to S&P Global Ratings. A further 700 billion euros matures in 2026. It will reset at higher rates. Interest payments on companies’ outstanding bonds and loans have already risen from 1.1% of nominal GDP in 2021 to 1.6% in 2022. Oxford Economics estimates the figure will reach 2.8% this year and 3.1% in 2024.

Homeowners with mortgages, which account for around 27% of euro zone households, are yet to feel the brunt of higher rates. That’s because, in recent years, more than half of all new housing loans had rates fixed for 10 years. A decade ago, that figure was less than a third. Add in other types of credit and nearly 45% of all consumer loans in the euro zone have interest rates fixed for five years or more, per Oxford Economics data.

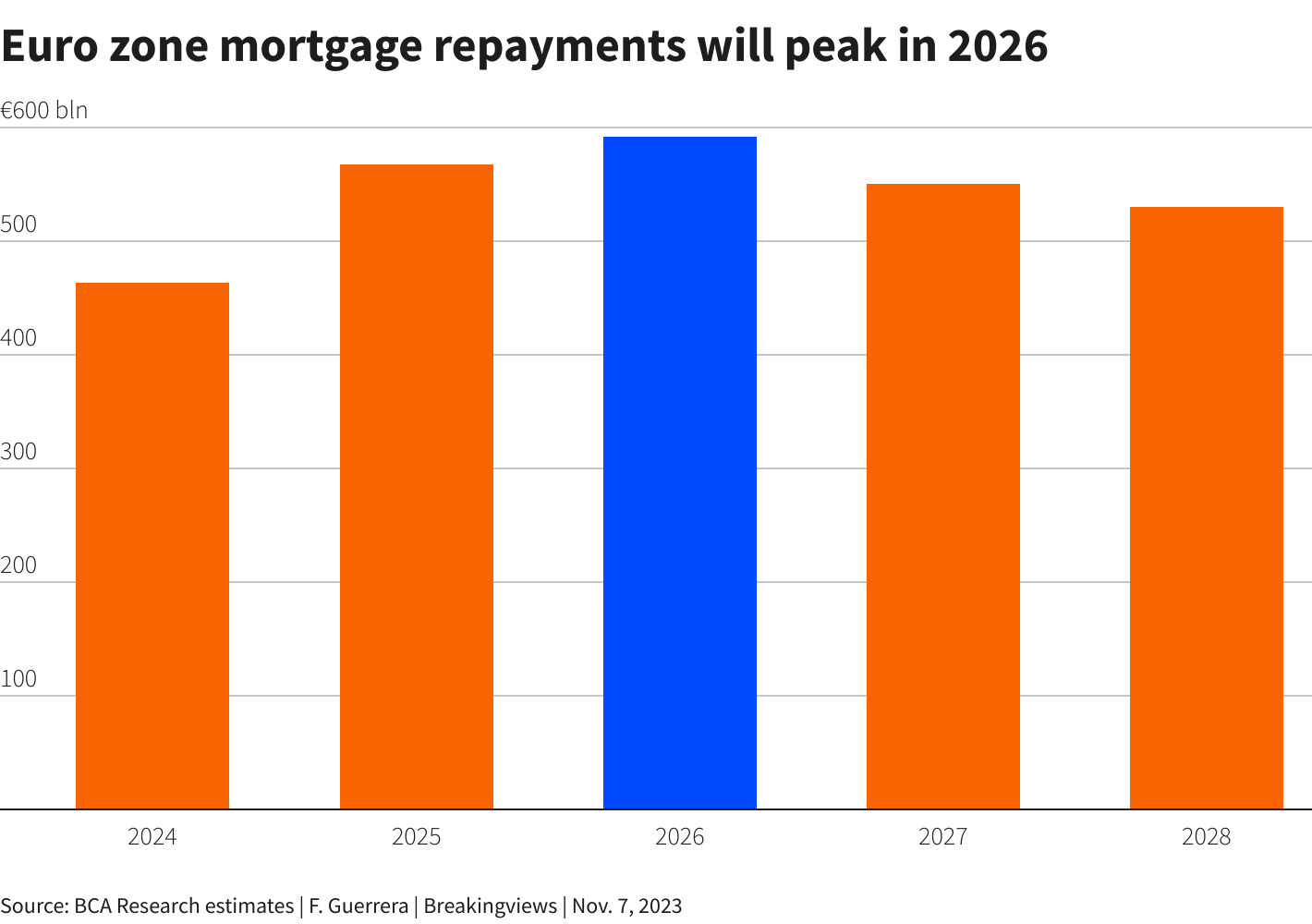

As a result, payments on all outstanding loans will rise by a relatively small 0.3 percentage points of GDP this year and next. The hit will be bigger in countries with more variable-rate loans, such as Spain and Italy, and almost negligible in the likes of France and Germany, where fixed rates are the norm. But as mortgages reset to higher rates, the repayment bill for households will jump from 463 billion euros in 2024 to a peak of nearly 600 billion euros in 2026, according to BCA Research.

Overall, European companies and households are likely to pay more interest on loans than the income they receive from investments. That, in turn, may harm European growth. Coupled with the weakness of traditional export markets such as the United States, the UK and China, and fiscal tightening by governments after the stimulus of the past few years, this increases the risk of a contraction in the euro zone in 2024. Several recession indicators are flashing red, from a slump in manufacturing and services activity to anaemic demand.

Surprisingly, a downturn no longer seems on forecasters’ radars. The ECB expects growth to accelerate to 1% next year, while the IMF is pencilling in an expansion of 1.2%. The bloc’s economy has proved remarkably resilient, but creaking corporate and individual balance sheets suggest the buffers against a recession are fast eroding.

Follow @guerreraf72 on X

(The author is a Reuters Breakingviews columnist. The opinions expressed are his own.)

Editing by Peter Thal Larsen, Oliver Taslic and Thomas Shum

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

{kind=link}