Analysis: Little relief for indebted Canadian homeowners as mortgage rates seen higher for longer

A for sale sign is displayed outside a home in Toronto, Ontario in Toronto, Ontario, Canada December 13, 2021. REUTERS/Carlos Osorio/File Photo Acquire Licensing Rights

TORONTO, Aug 23 (Reuters) – Highly indebted Canadians hoping for relief from a rapid rise in mortgage rates are in for some disappointment, as recent moves in the bond market point to interest rates staying at elevated levels for longer than previously expected due to stubborn inflation.

The yield on Canada’s 5-year bond climbed on Tuesday to a 16-year high of 4.17%, up from 2.66% in March, as investors gave up on the notion that the Bank of Canada and other major central banks will pivot quickly to rate cuts.

Nearly all Canadian mortgages have a term of five years or less, compared with the 30-year term that is common in the United States. As of January 2023, residential mortgage debt stood at C$2.08 trillion ($1.53 trillion), according to the Canada Mortgage and Housing Corporation (CMHC).

It means that when roughly 20% of Canadian mortgages come up for renewal in the next year, it will likely put many borrowers in a tougher financial spot than they could have expected just a few months ago. Mortgage rates tend to track moves in the bond market with a lag.

“With each passing month with rates going up and up, we are discussing with consumers how much mortgage they can qualify for, and that’s been diminishing as rates have gone up,” said James Laird, co-CEO of Ratehub.ca.

At 6.79%, the five-year mortgage rate posted by major Canadian banks has climbed to its highest since November 2008, data from the Bank of Canada shows.

When it is time for renewal, options for homeowners hoping to shop for better interest rates might be limited as they would have to re-qualify for the stress test at the latest interest rates with their new lender.

STRESS TEST FLAW

Canada amended its stress test rules in 2021 requiring borrowers to prove they can handle mortgage repayment 200 basis points above their contracted rate and will have to re-qualify if moving to a different lender at the time of renewal.

“That is a flaw in a stress test which hopefully will be changed at some point. … You’re going to see more consumers than usual sticking with their lenders,” Laird said.

The odds of another interest rate hike in September have only risen after inflation rate moved back above the Bank of Canada’s target range, while robust economic growth, particularly in the United States, has fanned fears of rates staying higher for longer.

With no sign of an immediate rate cut in sight, anxious homeowners are now struggling to pay their monthly mortgage payments, and in some cases being forced to sell their houses.

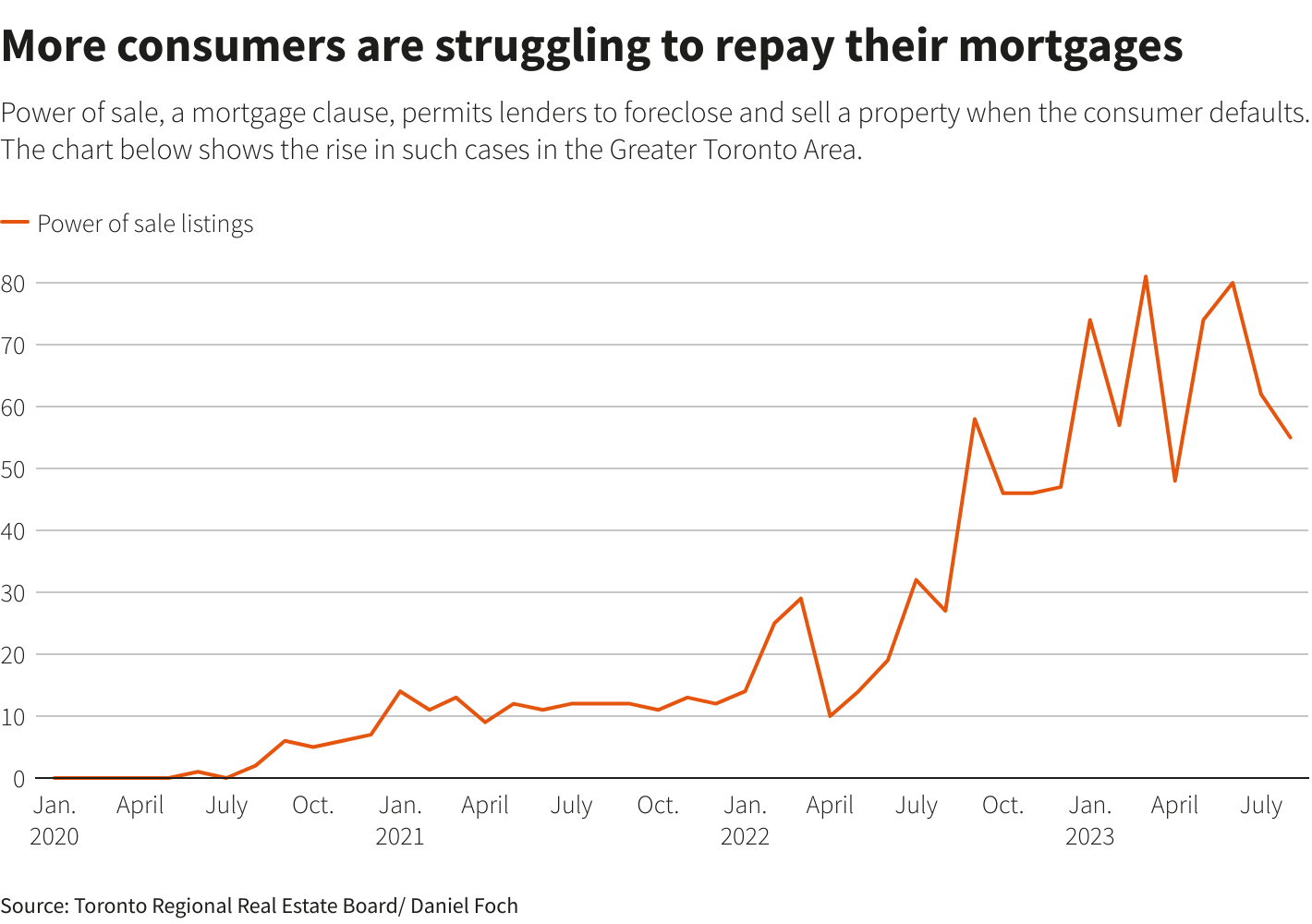

Daniel Foch, director of economic research at Toronto-based RARE Real Estate, pointed to Toronto Regional Real Estate Board data that showed power of sale – a clause that allows lenders to sell a borrower’s property if they default on mortgage payments – had risen in the recent months.

The data showed that power of sale was invoked for 48 to 80 properties in the past three months, compared with 14 to 32 a year ago, in the Greater Toronto Area. That number is on track to hit 75 by the end of August, Foch said.

With interest rates rising to a 22-year high, the mortgage growth rate in Canada has slowed to its weakest pace in roughly four years, according to analysts at KBW, which is expected to weigh on banks’ quarterly earnings starting this week.

“Whereas consumers over the last 12 months have maybe had some strong income growth to offset higher debt payments, that’s not going to be necessarily the case over the next 12 to 24 months,” said Stephen Brown, deputy chief North America economist at Capital Economics.

“It certainly is going to be problematic for the Canadian economy if rates stay at this level.”

($1 = 1.3566 Canadian dollars)

Reporting by Nivedita Balu and Fergal Smith in Toronto

Editing by Denny Thomas and Jonathan Oatis

Our Standards: The Thomson Reuters Trust Principles.