Investors scrutinize cost of surging brokered deposits and FHLB loans as midsize banks bear brunt of higher interest rates.

US banks have found a way to replace some of the hundreds of billions of dollars in deposits that flooded out their doors early this year. But it’s expensive, and not particularly sticky.

To shore up their books after a flurry of withdrawals by customers, midsize banks across the US have turned to a patchwork of other sources that demand significantly higher interest, typically around 5% or more. Regional banks borrowed billions more from the Federal Reserve, Federal Home Loan Bank system and — to an eye-popping degree — leaned on brokered deposits cobbled together by little-known intermediaries.

An analysis of quarterly regulatory filings for the 84 biggest banks — commanding more than 80% of the industry’s assets — shows not only how much they were borrowing through those channels at the end of March, but also the toll that it was just starting to take on some of their earnings. Those rising costs threaten to turn the most strained banks upside down: leaving them paying more to amass the cash they need than they earn by lending it out.

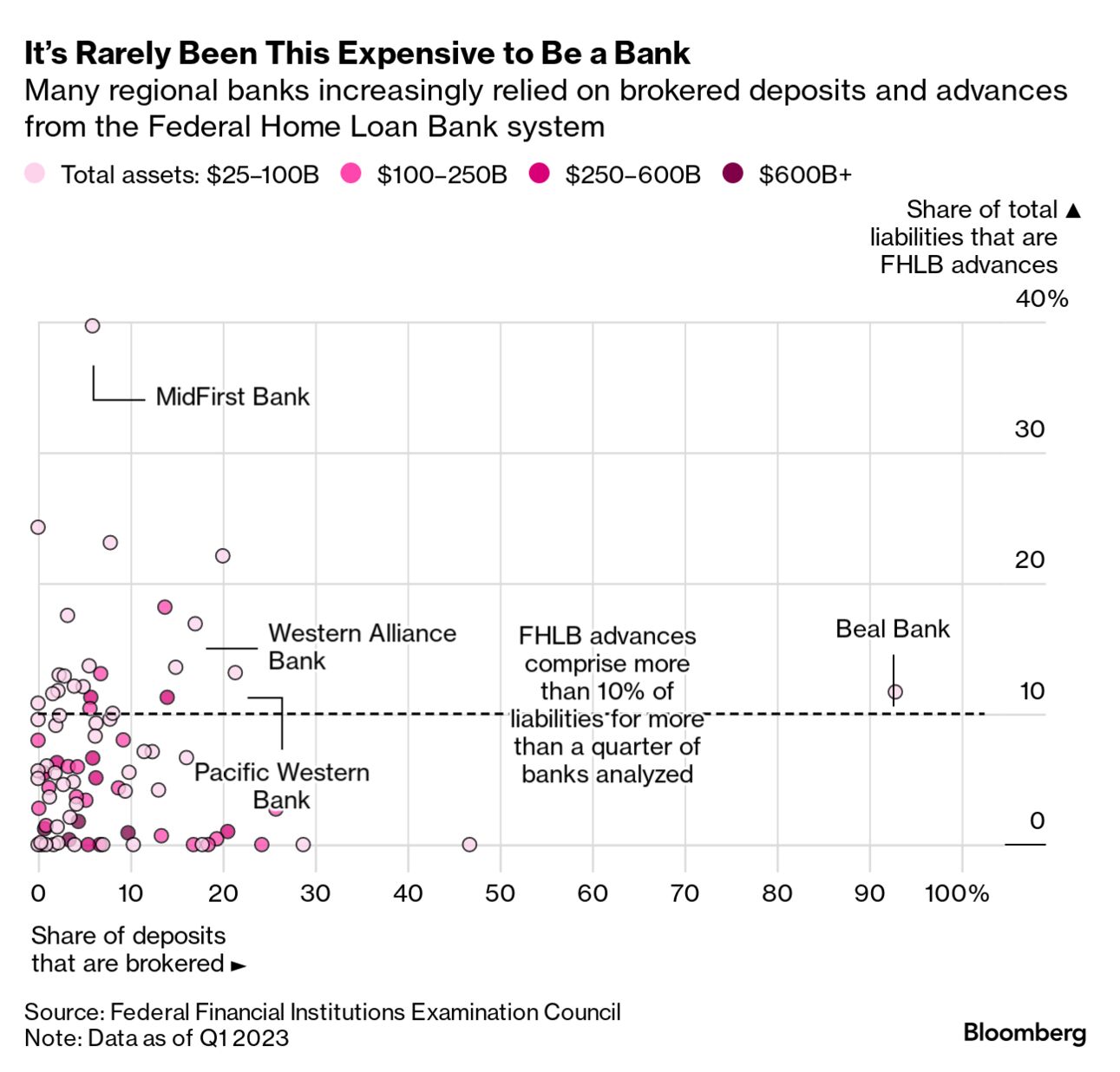

It’s Rarely Been This Expensive to Be a Bank

Many regional banks increasingly relied on brokered deposits and advances from the Federal Home Loan Bank system

Note: Data as of Q1 2023 Source: Federal Financial Institutions Examination Council

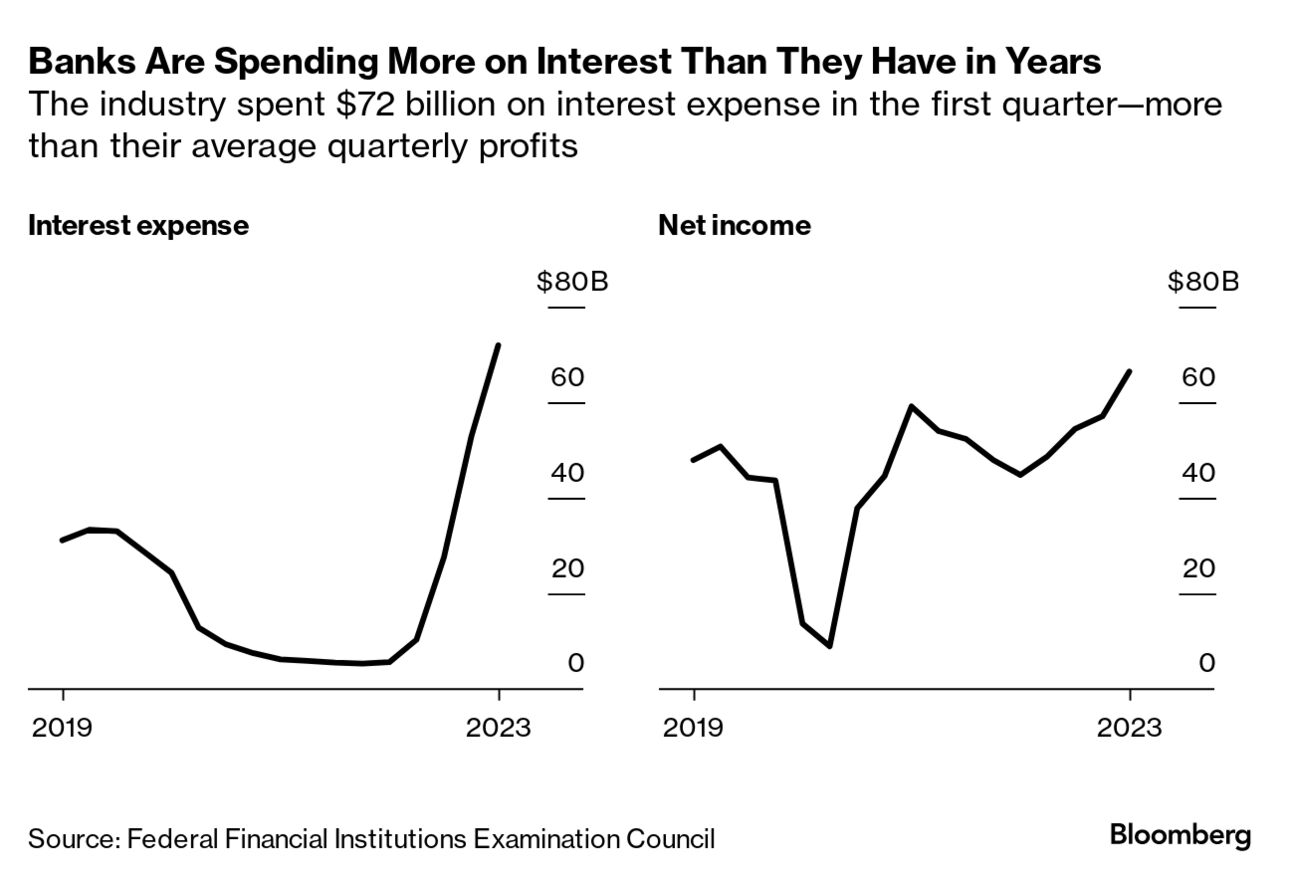

The strains can already be seen in the group’s interest expense, which surged 12-fold to $72 billion in the first quarter from a year earlier. That came as brokered deposits — dubbed “hot money” because the cash is rarely as sticky as that from established customers — and FHLB borrowings more than doubled to $1.42 trillion for the group. Brokered deposits amounted to more than $800 billion of that.

The bad news for bank shareholders is that the first quarter’s higher costs are probably just the start. At many regional banks, funding costs began surging only late in the quarter, as Silicon Valley Bank and Signature Bank were collapsing following the Fed’s aggressive interest-rate hikes. Investors have yet to see what a full quarter in the new landscape looks like — but they will in the coming weeks.

The data point to a potential picture of the next leg of the regional banking turmoil: less crisis and more grind. But if the higher cost of funding moves from lowering profits to causing losses and eating into capital, investors and regulators have already shown they won’t have much patience.

“This was a slow-motion car wreck,” Chris Marinac, an analyst at Janney Montgomery Scott, said in an interview. “We don’t even know if the Fed is going to raise once more. The Fed gave the banks a breather, but we’re not out of the woods yet.”

Higher rates are usually seen as good news for banks, and that’s indeed been playing out for the biggest firms. But this year has shown that some banks can get squeezed by such rapid Fed moves, particularly as money markets and Treasuries become more attractive than savings accounts.

Banks Are Spending More on Interest Than They Have in Years

The industry spent $72 billion on interest expense in the first quarter—more than their average quarterly profits

Source: Federal Financial Institutions Examination Council

Hot money comes in a variety of forms. Nowadays, many brokered deposits are cobbled together by little-known intermediaries that connect banks with wealthy individuals or companies looking for higher rates on their cash. Some are structured in the form of certificates of deposit. That can help banks, allowing them to hold the money for years unless buyers opt to pay a penalty. But it also means lenders are obligated to keep paying those higher rates for that period.

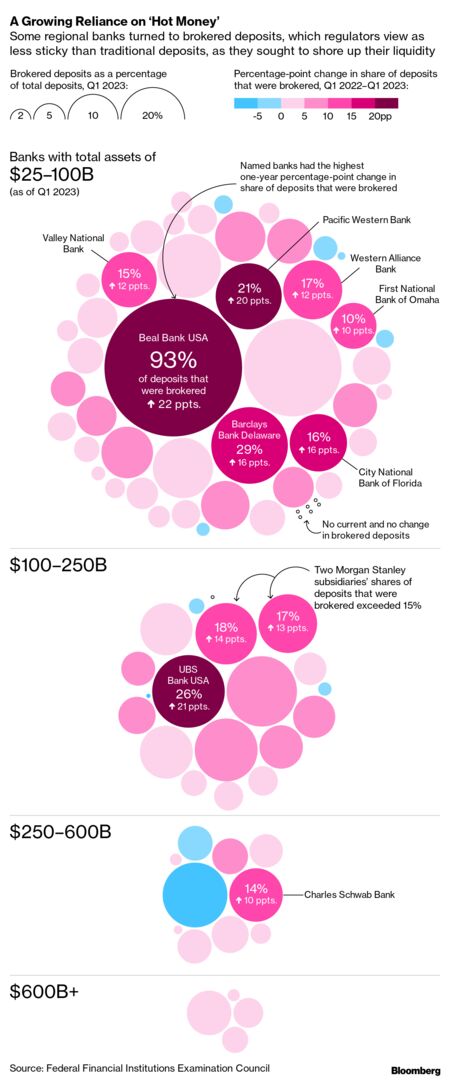

In total, brokered deposits jumped 15% to $808 billion in the first quarter from the end of last year at the 84 lenders, according to the analysis.

Regulators have often taken a dim view of brokered deposits, said Matt Bisanz, a partner in law firm Mayer Brown’s financial services regulatory and enforcement practice. That’s because “historically, brokered deposits could move and move quickly.”

Shareholders have already taken note of some of the firms with the greatest increases in brokered deposits and have been selling the shares. Take PacWest Bancorp, which has seen its stock price slump more than 60% this year. Brokered deposits at the firm jumped 1,774% to $6.09 billion in the first quarter from a year earlier and made up over one-fifth of the total. Absent the extra cash, the bank would have reported a 32% decline in deposits instead of 15%.

Western Alliance, where shares have also plummeted, saw brokered deposits more than triple in that same time frame. Back out those additional funds, and deposits at the quarter’s end would have dropped 20.6% instead of 8.8% as reported.

The increases are already weighing on analysts’ view of both banks’ prospects. Analysts tracked by Bloomberg now project Western Alliance will post a full-year profit of $808 million, or about $400 million less than what they estimated at the start of the year. At PacWest, analysts project a loss of more than $1 billion for the year, compared with the $470 million profit they expected at the beginning of 2023.

“Using Western Alliance’s quarter-end data as of March 31 is misleading of our current liquidity profile since it captures the peak impact of the fallout from the Silicon Valley and Signature Bank failures in mid-March,” Dale Gibbons, vice chairman and chief financial officer at Western Alliance, said in an emailed statement. “Since that time, our borrowings have declined by billions to more normalized levels.”

A spokesperson for PacWest didn’t respond to requests for comment.

A Growing Reliance on ‘Hot Money’

Some regional banks turned to brokered deposits, which regulators view as less sticky than traditional deposits, as they sought to shore up their liquidity

Source: Federal Financial Institutions Examination Council

The industry’s net income was still ticking higher in the first quarter, with Fed rate hikes bumping up lending revenue and the jump in funding costs only starting to materialize.

But since then, banks have been bracing shareholders for tougher times ahead. One by one this month, executives from regional banks across the country warned investors that higher funding costs were weighing on the industry. M&T Bank Corp. said there’s a big risk that consumers will keep pulling deposits out of banks. Columbia Financial Inc. warned that its efforts to hold onto depositors would likely hinder profitability for the year. Fifth Third Bancorp said net interest income, a measure of lending profits, won’t rise as much this year as it previously expected.

On top of the brokered deposits, banks paid up to borrow from the Federal Home Loan Bank system, typically the last stop before they use the Fed’s discount window, which carries a greater stigma.

For the subset of banks analyzed, FHLB borrowings swelled to 3.5% of total liabilities in the first quarter from less than 1% in 2021. FHLB advances are secured by mortgages and other assets, and the majority have to be paid off or refinanced again in relatively short order.

In the first quarter, 67% of the loans had a maturity of a year or less.

Eventually, replacing core deposits with hot money and higher-interest borrowings can be a recipe for instability. That’s what authorities pointed to at First Republic when they seized the bank at the start of May, orchestrating its emergency sale to JPMorgan Chase & Co.

“The higher cost borrowings that significantly exceed asset yields have contributed to the bank becoming structurally unprofitable,” California Department of Financial Protection and Innovation Commissioner Clothilde Hewlett wrote in an order seizing First Republic. “The bank is conducting business in an unsafe or unsound manner.”

The reality for smaller banks is that it’s simply going to be harder to compete with a Treasury bill yielding more than 5%, said Michael Driscoll, managing director and head of the North America financial institutions group at DBRS Morningstar.

“Banks are working hard to keep deposits, and they’re just having to pay up,” Driscoll said.

“Barclays is well-capitalized, with a very strong liquidity and funding position and a stable and diversified deposit base,” a spokesman said in an emailed statement. “Our diversified business mix and highly disciplined approach to risk management means we continue to be well-positioned to navigate the current market volatility. We have a long history of helping customers and clients during unprecedented economic challenges and will continue to help them manage and navigate market disruption.”

“For Schwab, supplemental funding sources such as retail CDs are short-term in nature. In Schwab’s example, most of our CDs as of 3/31 will mature before the end of 2024, with some starting this year. Furthermore, cash realignment trends show strong indications of abating during the second half of 2023, allowing us to roll off these temporary higher cost of funds in quarters.”

City National Bank of Florida

“City National Bank of Florida generated significant client deposit growth of $862 million in Q1 of 2023, representing a 20% annualized growth rate,” a spokesman for the bank said in an emailed statement. “This growth outperformed the broader banking industry, which experienced deposit attrition of 14%during the same term. In a strategic move designed to capitalize on lower funding costs, CNB replaced $925 million in FHLB borrowings with $966 million in brokered deposits in January and February of this year. This decision helped bolster CNB’s liquidity and capital ratios between year-end 2022 and the close of Q1 2023, with the Bank’s available liquidity representing 43% of total assets and its Total Risk Based Capital Ratio measuring 13.9%, well above the 10.0% threshold considered ‘well capitalized.’ As a commercial bank that has been serving the businesses and individuals driving Florida’s economy for 77 years, CNB remains among the strongest, best capitalized banking institutions in the country. From real estate and small business lending, to private banking and commercial finance, CNB is focused on responsible lending, delivering exceptional service to best-in-class clients, and pursuing steady growth across Florida’s key sectors. This model has fueled CNB’s strength and stability for decades, and it will continue to guide the bank into the future.”

“In periods of volatility, brokered deposits have proven to be a stable and reliable source of FDIC-insured indirect customer deposits for Valley and the banking industry in general,” a spokesman for Valley National said in an emailed statement. “As direct deposit pricing competition has increased over the past year, the gap to incremental brokered deposit funding costs has narrowed significantly. This has made the use of brokered deposits relatively more cost effective today than in other periods.”

“Using Western Alliance’s quarter-end data as of March 31 is misleading of our current liquidity profile since it captures the peak impact of the fallout from the Silicon Valley and Signature Bank failures in mid-March,” Dale Gibbons, vice chairman and chief financial officer at Western Alliance Bank, said in an emailed statement. “Since that time, our borrowings have declined by billions to more normalized levels as deposits have increased in line with our $2 billion per quarter growth guide and we’ve completed over $4 billion in asset dispositions. In addition, deposits reported as brokered in our March 31 call report include over $3 billion in ‘reciprocal’ deposits. These are relationship-based deposits and do not necessarily reflect higher rates that wholesale brokered funding may require. These funds were placed with other banks via inter-bank depository networks in order to maximize deposit insurance coverage for our clients, and for which we received an equal amount of deposits in return.”

Banks that declined to comment, didn’t respond to requests for comment or did not have immediate comment when reached:

Beal Bank, First National Bank of Omaha, MidFirst Bank, Morgan Stanley, UBS

{kind=link}