The fortunes of investment trust Mercantile are very much tied to the UK economy. If recession is avoided, inflation is tamed and the spate of interest rate rises is brought to an end, the £1.6 billion trust could be on the cusp of a sustained period of strong investment performance.

But, if the economy bombs, the trust could struggle. Lots of ifs – and few clear-cut answers.

It is a point that Guy Anderson, who manages the trust with Anthony Lynch, readily accepts.

He says: ‘The outlook for the UK economy is important for the fund. Half of the revenues generated by the companies we hold are domestic and it is fair to say that it has been a challenging time dealing with all the moving parts that have fuelled inflation – the pandemic, a tight labour market and the invasion of Ukraine and rising energy prices.’

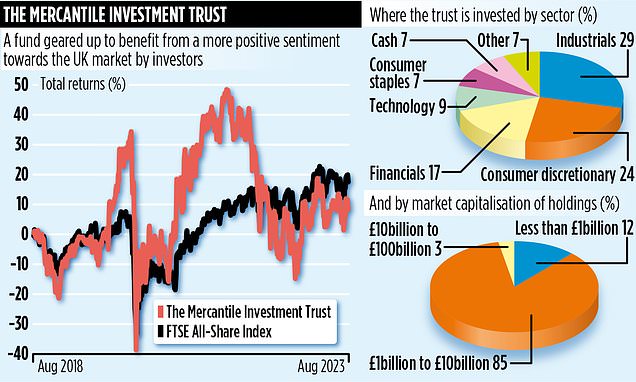

The challenges have taken a toll on the trust’s investment returns. Over the past three and five years it has underperformed its benchmark, the FTSE All-Share Index. For example, over the past five years, it has delivered a return to shareholders of 9 per cent, compared to 16 per cent from the index.

But Anderson remains upbeat. ‘The narrative about the UK is negative,’ he says. ‘I accept that, but the UK economy has been more resilient than many expected. Hopefully, recession can be avoided although what could continue to hurt the market is sticky inflation and more interest rate rises.’

With a lot of economic negativity already priced into many UK stocks, Anderson’s view is that as an investment manager it is now ‘better to be greedy than defensive’. In other words, buy stocks while they are cheap.

It explains why the trust has employed more than £150 million of borrowings to increase its exposure to UK companies. The average cost of the loans is priced at just under 4.2 per cent – which means the assets bought with the loan finance must deliver returns in excess of this figure for shareholders to benefit.

Related Articles

HOW THIS IS MONEY CAN HELP

It is a hurdle Anderson says is achievable given the quality (and value for money) of the trust’s underlying holdings, half of which have been held for at least five years.

The fund has stakes in 67 companies with its two biggest sector positions in industrials and consumer discretionary. Among its key holdings are IMI and Rotork.

‘Both are resilient businesses,’ says Anderson, ‘playing key roles in the energy sector. IMI’s critical engineering division supplies valves across the energy industry while Rotork is a high quality engineer benefiting from greater expenditure by oil and gas companies.’

In the consumer space, key holdings include furniture giant Dunelm which Anderson says has a ‘huge runway of future growth’ on the back of strong store and digital businesses.

WH Smith – like Dunelm a top ten holding – is held because of its focus on the travel industry and a broadening of the products available in its stores. ‘It’s perceived to be yesterday’s retailer,’ says Anderson. ‘That is a misconception.’

A recent addition to the portfolio is airline Jet2 – on the back of a buoyant travel market.

Over the past ten years, the trust has increased its dividend every year – and for the past 30 years, it has not cut it. This financial year Anderson expects an increase on last year’s payment of 7.15p a share. The first quarterly payment of 1.45p compares to last year’s 1.35p. The shares trade at around £2.

The trust, part of the JP Morgan Asset Management stable, has competitive annual charges of 0.46 per cent. Its stock market ID code is BF4JDH5 and market ticker MRC.

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

{kind=link}