The core concept of ESG investing has existed for centuries, dating back to religious codes banning investments in slave labor. Fast-forwarding to the 1960s and 1970s, divestments from South Africa were first advocated to protest the country’s system of apartheid. Many other issues were to follow that also drove socially responsible investing strategies.

In 1971 two United Methodist ministers opposed to the Vietnam War created the Pax World Fund, the first publicly available mutual fund in the U.S. that factored social and environmental criteria into investment decisions. Meanwhile, pension funds with worker-investors’ interests began targeting investments in areas geared to improved healthcare and affordable housing. But decades passed until actions like these were formalized into specific rules and practices that eventually manifested into the framework now known as environmental, social and governance.

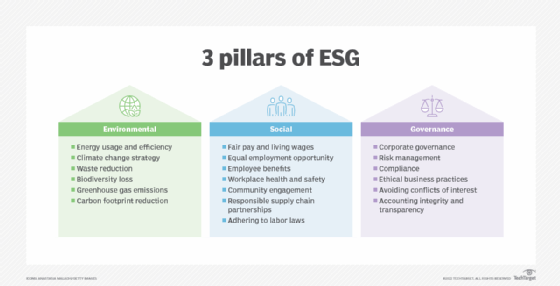

Over time, ESG has motivated a groundswell of pressure from investors and consumers supported by an assortment of national and international regulations. Detailed ESG guidelines, adoption agreements, timelines and compliance issues are not yet fully finalized, said Marsha Reppy, sustainability technology consulting leader at EY Americas. But she expects regulatory standards to be at the forefront and likely to continue expanding beyond climate risks and into social issues.

“CIOs can and should start incorporating [ESG] into their roadmaps, identifying synergies with already planned initiatives,” Reppy advised. Some business sectors will be more heavily impacted than others. Statistical data will be especially critical in meeting ESG guidelines, and compliance by most organizations will require a significant investment in time and money.

It’s essential to develop the right solution architecture that can accommodate these rapidly evolving regulations, processes and technologies. Enterprises will need leeway in adjusting to these changes.

Much of the ESG landscape we see today was shaped by many key events, trends, actions and milestones over the past 35 years.

1990: Domini 400 Social Index

Amy Domini, who managed KLD Research and Analytics, created the Domini 400 Social Index, which focused on companies prioritizing social and environmental responsibility. During this time, including social and environmental issues among business priorities was considered a bad gamble for investors.

The following year, Domini created the Domini Social Impact Equity Fund to test the waters. The fund attracted $1.3 billion by 2001 and showed returns of 15.08% compared to 15.25% for the S&P 500, demonstrating that investing in socially responsible issues can deliver strong financial returns.

The Domini 400 is now called the MSCI KLD 400 Social Index. The weighted index consists of 400 U.S. securities “provides exposure to companies with outstanding ESG ratings and excludes companies whose products have negative social or environmental impacts.”

1992: United Nations Framework Convention on Climate Change

A group of 154 nations signed a treaty to mitigate “dangerous human interference with the climate system” at the Earth Summit in Rio de Janeiro. The treaty called for research and ongoing meetings and planted the seeds for future policy agreements. It also launched an annual meeting of participants called the Conference of the Parties (COP) to hash out details and revise goals. This action helped galvanize international efforts to mitigate temperature increases caused by human greenhouse gas emissions with plans to cap and reduce them over time.

1995: First sustainable investment inventory in the U.S.

The Washington, D.C.-based Social Investment Forum Foundation, now known as the U.S. SIF Foundation, took the first inventory of the total size of sustainable investments, revealing a total of $639 billion in assets managed in the U.S. By 2020, the Global Sustainable Investment Alliance estimated $35.3 trillion in sustainable assets worldwide.

Meanwhile, the U.S. SIF’s December 2022 report listed $8.4 trillion in ESG and sustainable investments in the U.S. That was down from $17.1 trillion in 2020 due to a decision to remove investors that don’t provide specific information on what ESG criteria they follow. But U.S. SIF said the $8.4 trillion still amounted to 12.6% of all the professionally managed investment assets in the U.S.

1997: Kyoto Protocol

The Kyoto Protocol was adopted in 1997 and entered into force in 2005. An agreement to specific greenhouse gas reduction targets was eventually ratified by 192 countries, 36 of which signed up for the first commitment period. All 36 countries met their obligations, but nine of them had to fund climate reduction programs in other countries because they went over their targets.

The two largest emitters, China and the U.S., were absent. China set no binding targets, while the U.S. never ratified the treaty. Canada initially participated but withdrew in 2012 after realizing it would be obligated to pay $14 billion in fines for missing targets.

1997: Global Reporting Initiative

To address environmental concerns, the Global Reporting Initiative (GRI) was launched. The group expanded its mandate to broadly address social and governance issues. In 2016 it shifted from providing guidance to ratifying the first global standards for sustainability reporting.

2000: United Nations Global Compact

The U.N.’s Global Compact establishes principles across diverse areas, including human rights, labor, the environment and anti-corruption. More than 13,000 corporate and agency stakeholders in 170 countries participate.

Presented as a forum rather than a regulation, the goals are deliberately vague and intended to spark discussions, negotiations and other measures through dialogue-specific projects. In 2022, 78% of the world’s largest 250 companies used the GRI standards, according to a KPMG survey. Today, participants total more than 20,000 stakeholders.

2000: Carbon Disclosure Project

Paul Dickinson co-founded the Carbon Disclosure Project (CDP) to organize and empower large investors to ask companies to report on their climate performance and ways to mitigate risks. In 2002, 35 investors requested climate disclosures from the 500 largest firms to help normalize climate disclosures.

The project helped support the Task Force on Climate-Related Financial Disclosures, which reached out to more than 8,000 companies. By 2021, companies with 64% of market capitalization responded with climate disclosures. The group expanded its work to improve water security and reduce deforestation. By 2023, CDP represented investors with more than $136 trillion in assets.

2004: First “Who Cares Wins” report published with the term ESG

At the invitation of the U.N., a group of banks and other investment firms summarized the critical issues in a report titled “Who Cares Wins,” which popularized the term ESG. The report provided several recommendations for integrating ESG issues in analysis, asset management and securities brokerages. The group proposed that greater inclusion of ESG factors in investment decisions will contribute to more stable and predictable markets. Four more reports were published from 2005 to 2008.

2005: Freshfields report

With backing from the U.N., the London-based law firm Freshfields Bruckhaus Deringer published “A legal framework for impact: Sustainability impact in investor decision-making.” The report suggested that financial trustees should include environmental and social considerations in their analysis of companies. Over the years, this proposal has been refined into investing for sustainability impact (IFSI).

2006: Principles for Responsible Investment

At the invitation of the U.N., a group of 70 investment and environmental experts published six principles advocating institutional investors should incorporate ESG considerations into their decisions. The principles call for investors to include ESG issues, become active owners, seek appropriate disclosures, promote acceptance of ESG analysis, enhance effectiveness in addressing ESG issues, and report on activities and progress.

2007: Climate Disclosure Standards Board

Many of the largest organizations working on climate issues came together to establish the Climate Disclosure Standards Board (CDSB). The new group created a reporting framework that elaborated on the risks and opportunities of climate change on an organization’s strategies, financial performance and condition. It later added considerations for water security and forest risks.

The CDSB currently provides a framework to harmonize reporting on greenhouse gas emissions and natural capital. It helps efforts to share data structured using the Extensible Business Reporting Language in conjunction with the Climate Change Reporting Framework.

2011: Sustainability Accounting Standards Board

Jean Rogers launched the Sustainability Accounting Standards Board to create meaningful accounting standards that reflect the impact of ESG factors on the bottom line of companies in a specific industry. Beverage companies, for example, would have to account for water security, while sustainable energy companies would have to account for the environmental impact of mining activities that produce their equipment.

These standards aim to provide the same consistency in reporting on the risks and opportunities of meeting sustainability goals that traditional accounting metrics bring to value investment decisions. The group went on to develop standards for 77 industries across 11 sectors.

2015: U.N. Sustainable Development Goals

The U.N. General Assembly formulated 17 Sustainable Development Goals (SDGs). A few years later, the SDGs were further clarified with 169 specific targets and 232 unique indicators of progress. They cover many issues, including poverty, food security, health, equality, water, clean energy, work, infrastructure, sustainability, climate, oceans, ecosystems, justice and partnership.

2015: Taskforce on Climate-related Financial Disclosures

The Financial Stability Board, an industry consortium that makes recommendations on various risks, launched the Taskforce on Climate-related Financial Disclosures (TCFD). The new group currently works on standards for reporting climate-related disclosures for banks, businesses and investors. It helps price the potential impact of climate risks on a company’s bottom line. More than 3,800 companies have become supporters of the TCFD recommendations.

2016: Workforce Disclosure Initiative

ShareAction, a charity that supports responsible investment, launched the Workforce Disclosure Initiative. The program aims to increase the value and quality of data on workforce health, safety and risk management metrics. Sixty-eight institutional investors currently support the program with more than $10 trillion in assets under management.

2017: The Compact for Responsive and Responsible Leadership

More than 140 CEOs signed The Compact for Responsive and Responsible Leadership at the World Economic Forum (WEF) meeting in Davos, Switzerland. The CEOs made a commitment to collaborate on the U.N.’s SDGs to benefit both the companies they run and the world. One of the compact’s essential points: “Society is best served by corporations that have aligned their goals to serve the long-term goals of society.”

2017: State Street Global Advisors and board diversity issues

Asset management firm State Street Global Advisors, in conjunction with the installation of its “Fearless Girl” statue on Wall Street, told 600 companies in the U.S., U.K. and Australia that it would vote against the chairs of boards that have no female directors or candidates. In a matter of months, 42 companies committed to increasing diversity, and seven of them added women board members. Global Advisors later voted against 400 companies that failed to initiate diversity efforts.

2019: Davos Manifesto 2020

The WEF publishes the Davos Manifesto 2020 as a set of ethical principles to guide companies through the Fourth Industrial Revolution. The document expressed the need for companies to serve employees, customers, suppliers, stakeholders, and local communities and society. Emphasis was on companies treating people with dignity and respect, integrating human rights into the supply chain, paying their fair share of taxes and achieving ESG objectives.

2020: COVID-19 pandemic and other events

The COVID-19 pandemic forced millions of employees to work from home, showing how an unseen danger can upend the world economy and the well-being of individuals. Businesses struggled to keep pace with new operating realities.

Meantime, the legions of remote workers had more time to follow environmental disasters, including extreme heat, forest fires, floods and hurricanes. The mistreatment and subsequent death of George Floyd while in police custody, resulting in a second-degree murder conviction, stoked concerns of racism.

J.P. Morgan’s survey of institutional investors found that 71% of respondents believe an event like the pandemic would “increase awareness and actions globally to tackle high-impact/high-probability risks such as those related to climate change and biodiversity losses.”

2020: Standardized stakeholder capitalism metrics

The WEF and Big Four accounting firms released a whitepaper standardizing metrics for companies reporting on their ESG progress. The metrics helped align reporting on ESG indicators with progress toward SDGs. Since the release, more than 50 companies have incorporated these metrics into their reports, and 90 more companies have committed to implementing them.

2021: E.U.’s Sustainable Finance Disclosure Regulation

The European Union’s Sustainable Finance Disclosure Regulation imposed requirements on describing funds with specific sustainable investment objectives that promote environmental or social characteristics and those that are non-sustainable. The rules introduced Principal Adverse Impact, which characterizes the negative impacts of investments on sustainability goals. By 2023, funds that promote sustainability must report on protecting water resources, transitioning to a circular economy, controlling pollution and restoring biodiversity.

2022: Tesla ejected from S&P Sustainability Index

Long known for being environmentally friendly, Tesla CEO Elon Musk revolutionized the auto industry and has dominated the market for electric cars. About one month after Musk initiated negotiations to purchase Twitter, Tesla was cut from the S&P 500 ESG Index due to a “rebalance” and its “decline in criteria level scores” for lack of “low carbon energy and codes of business conduct. [W]hile Tesla’s S&P DJI ESG Score has remained fairly stable year-over-year, it was pushed further down the ranks relative to its global industry group peers,” wrote Margaret Dorn, senior director and head of ESG Indices in North America at S&P Dow Jones Indices, in her May 17, 2022, blog post.

Other reasons for removal from the index were claims of racial discrimination and poor working conditions at one factory as well as Tesla’s handling of a National Highway Traffic Safety Administration investigation into 17 injuries and one death linked to crashes involving the company’s Autopilot feature.

2022: Consolidation of sustainability standards

The International Financial Reporting Standards (IFRS) foundation has maintained accounting standards for most countries, except the U.S. The Value Reporting Foundation (VRF), which managed the Sustainable Accounting Standards Board standards, consolidated into the IFRS to create the International Sustainability Standards Board. The IFRS consolidated the VRF and the Climate Disclosure Standards Board, creating a global baseline for sustainability disclosures, except in the U.S.

The U.S. Generally Accepted Accounting Principles are managed separately by the Financial Accounting Standards Board. The Securities and Exchange Commission proposed new rules requiring “registrants to provide certain climate-related information in their registration statements and annual reports.”

2023: EU’s Corporate Sustainability Reporting Directive

A new European Union directive specified that EU companies and non-EU businesses operating in the EU will soon be required to make corporate sustainability disclosures relating to their alignment with an EU ESG-related taxonomy and audit sustainability data. These reports should include information on environmental and social matters, human rights, anti-corruption and diversity. This information must be included in 2024 year-end reports to be filed in 2025 by companies meeting some of the following criteria: more than 250 employees, €40 million in annual revenue and €20 million in total assets.

2023: ESG investing becomes a political issue in the U.S.

The U.S. Congress adopted a joint resolution to rescind a final rule issued by the Department of Labor in 2022 that allows retirement fund managers to consider ESG metrics in investment decisions. President Biden vetoed the measure, leaving the rule in effect. An ideological battle is unfolding between states that have embraced ESG-focused investing and states seeking to exclude it. Investors may gamble on better returns from ESG investments that take advantage of Inflation Reduction Act climate-related incentives.

Future of ESG investing

The ESG landscape will continue to evolve rapidly. There has been a significant regulatory shift in climate-related disclosures during the last few years that will likely continue, observed Rita N. Soni, principal analyst for impact sourcing and sustainability at the Everest Group. Central banks around the globe, for example, are planning to proceed with climate stress tests.

ESG investing and regulation will continue to expand and cover more topics, said Sammy Lakshmanan, principal of ESG at PwC. Much of the focus in the U.S. is currently on climate, while the EU’s ESG reporting is expanding to include areas like waste, circular economy, biodiversity, diversity and inclusion. “This means that enterprises have to manage the increased regulatory reporting at a more granular level with greater complexity,” Lakshmanan added.

To manage the growing number of metrics that were once voluntarily disclosed but are now required, CIOs will have to invest in the automation and industrialization of ESG data and metrics reporting. As a result, the speed, efficiency and interoperability of the data will need to improve. To provide the required “verification and independent assurance,” Lakshmanan said, “CIOs will also need to ensure the data has the right governance and controls in place.”

{kind=link}