Why the UK’s middling growth hasn’t stopped stocks.

The UK’s Office for National Statistics (ONS) published its first estimate for Q1 GDP Friday, showing 0.1% q/q growth.[i] Many outlets portrayed this as lackluster, and it isn’t stellar in isolation. But against long-running and widespread recession expectations, we think it likely amounts to a positive surprise. And that is all stocks need to rise, in our view.

While quarterly headline growth was meager, all major output categories rose. Services and production each grew 0.1% q/q and construction climbed 0.7%.[ii] Within services—the lion’s share of the UK economy—information and communication rose 1.2% q/q and contributed the most to its category. Manufacturing’s 0.5% q/q growth led production, offsetting mining and quarrying’s -5.0% drop, while utilities output was flat. On the expenditures side, household consumption rose 0.1% q/q and gross fixed capital formation jumped 1.3% with business investment, its largest subcategory, up 0.7%.

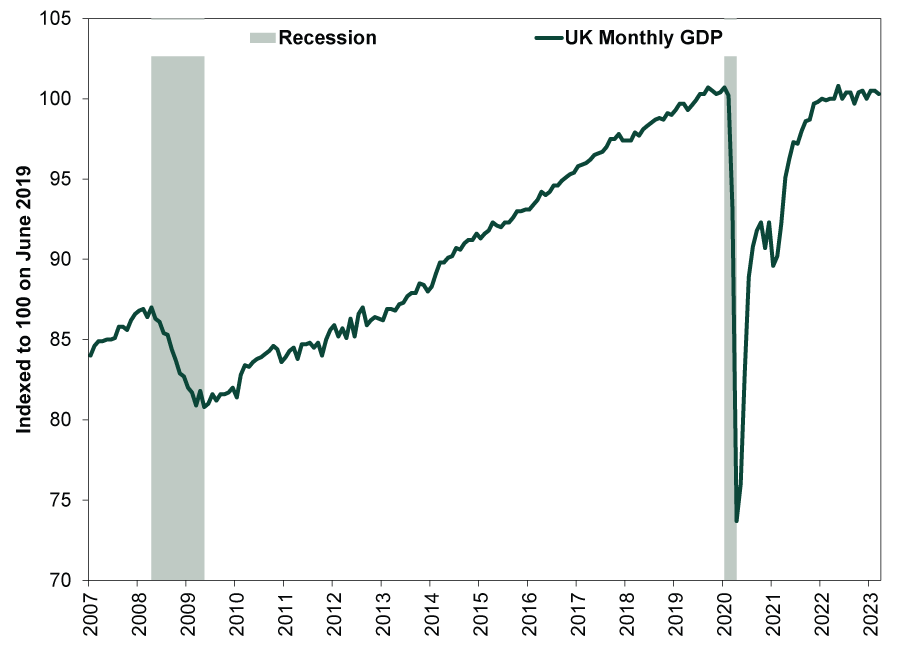

But UK monthly GDP data show growth was frontloaded last quarter. After January’s 0.5% m/m gain, GDP was flat in February and then dropped -0.3% in March.[iii] While production grew 0.7% m/m in March, services fell -0.5%, with consumer-facing services in particular down -0.8%. The ONS noted an “exceptionally wet March 2023 (the sixth wettest March since 1836)” and strikes, aka “industrial action,” likely had an impact. Anecdotal evidence suggests wet weather hit retail sales, food and beverage services, sports and recreation activities and some kinds of construction services like equipment leasing. And while we aren’t passing any judgment on the strikes, they appeared to affect output in the health sector, civil services, education and the rail network.

The UK’s industrial actions have been off and on since last summer, though, which helps account for the latest monthly wiggles in Exhibit 1. While not great for economic activity, strikes—and the weather—are short-term and temporary factors that wane over time. They may delay demand, but they don’t delete it.

Exhibit 1: Don’t Read Too Much Into Monthly Wiggles

Source: ONS, as of 5/12/2023. UK monthly GDP, January 2007 – March 2023. Recession shading based on major peak-to-trough downturns.

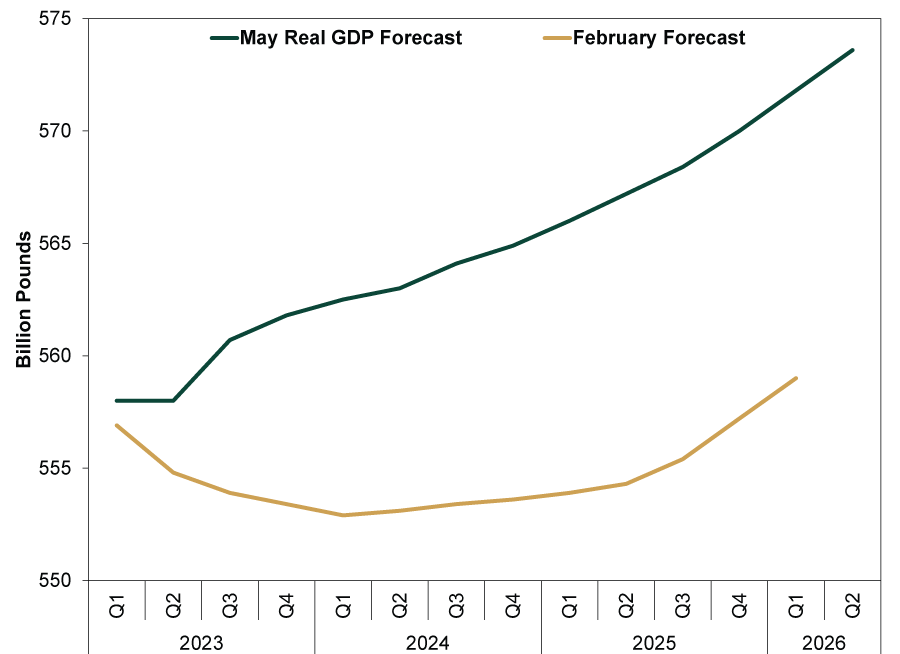

For forward-looking markets, Q1 and March GDP are well in the rear view. More relevant to them is the bigger picture taking shape ahead: The UK economy’s muddling through contrasts with high-profile recession forecasts. Case in point: Just ahead of Friday’s GDP reports, the Bank of England (BoE) revised its growth forecasts to 0.25% this year and 0.75% in 2024. (Exhibit 2) While this would be historically middling, its revamped outlook is far from February’s forecast contractions of 2023’s -0.5% and next year’s -0.25%. Not only does the BoE no longer project any quarterly contractions versus a years-long recession, May’s revision was its biggest upward adjustment since gaining independence in 1997. Whoops!

Exhibit 2: Don’t Read Too Much Into BoE Forecasts

Source: Bank of England, as of 5/11/2023.

The BoE pointed to declining energy prices and better-than-anticipated economic resilience as underpinning its about-face. This is with policy rates higher now than when the BoE began predicting recession last year, which forced Governor Andrew Bailey to admit rate hikes’ economic impact is overrated.

Not that the BoE’s new forecasts will necessarily prove more accurate. But we think it does show the wide gap between expectations and reality, which moves stocks most. The MSCI UK Investable Market Index’s 31.9% gain from the autumn’s low, beating the rest of the world’s 17.7%, strongly suggests to us the UK’s economic prospects aren’t as bad as imagined last fall or earlier this year.[iv] In our view, this is a textbook example that it doesn’t take gangbusters growth for markets to rally, just a wall of worry for stocks to climb.

{kind=link}