Image source: Getty Images

Investor appetite for riskier FTSE 100 stocks continues to improve. The Lloyds Bank (LSE:LLOY) share price, for instance, has recovered more ground as fears over the banking system recede.

Yet at the current price of 47.9p the company still looks extremely cheap on paper. And so, in theory at least, this leaves plenty of room for additional gains should market confidence continue to improve.

Today the bank trades on a low price-to-earnings (P/E) ratio of 6.3 times. Furthermore, its 5.8% dividend yield seems to offer excellent value for income investors.

Why I’m avoiding Lloyds shares

Having said all that, I’m not planning to buy Lloyds shares for my portfolio.

Predicting the near-term movement of UK share prices is a notoriously difficult task. Market sentiment can turn suddenly for a variety of economic and industry-related factors, as events of recent weeks show.

The Lloyds share price could well spring higher in the coming days. It might also sink again. But I’m fairly certain of one thing — over the long term I think the Black Horse Bank could struggle.

On the plus side…

A steady stream of interest rate increases have boosted profits at the high street banks. The Bank of England has hiked rates an eye-popping 11 times since late 2021. This has helped Lloyds and its peers make more money from their lending activities.

The benchmark rate could climb even further from current levels of 4.25% if inflationary pressures persist.

Long-term uncertainty

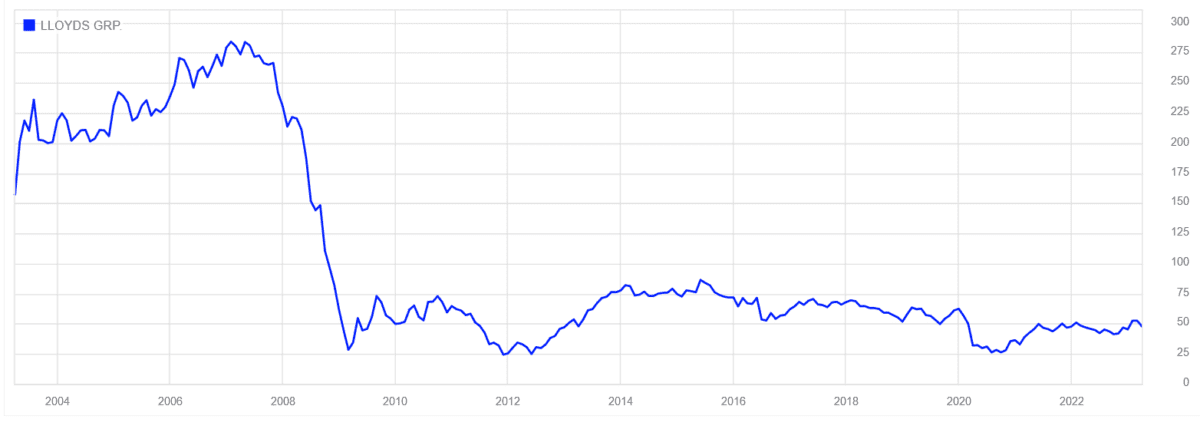

The trouble for Lloyds et al is that interest rates have remained well below historical levels following the 2007-08 financial crisis. This is reflected in their share prices being very short of pre-crisis levels and failing to gain meaningful ground since then (as shown below).

It seems that rates are unlikely to return to levels recorded before the late 2000s too. Indeed, the Bank of England benchmark looks unlikely to rise much higher from current levels. And it’s tipped to reduce sharply from the second half of 2023.

Bloomberg recently reported comments from Bank of England governor Andrew Bailey in which he said that “interest rates will not necessarily have to return fully to, and remain around, the higher levels they once had.” This bodes badly for Lloyds and its peers.

Better buys

In the absence of interest rate rises it’s difficult (at least in my opinion) to see how Lloyds’ share price will gain ground over the long term.

For one, the UK economy looks set for prolonged weakness due to structural problems like elevated public debt, labour shortages and low productivity. In this landscape, retail banks are unlikely to significantly grow revenues.

The issue is being made worse by the digital banks too. These smaller and more nimble operators are capitalising more effectively on the growth of online banking than the high street players. They’re also able to offer more attractive products thanks to their lower cost bases.

I believe the cheap Lloyds share price reflects this tough trading environment. Right now I’d rather invest in other cheap FTSE 100 shares.

{kind=link}