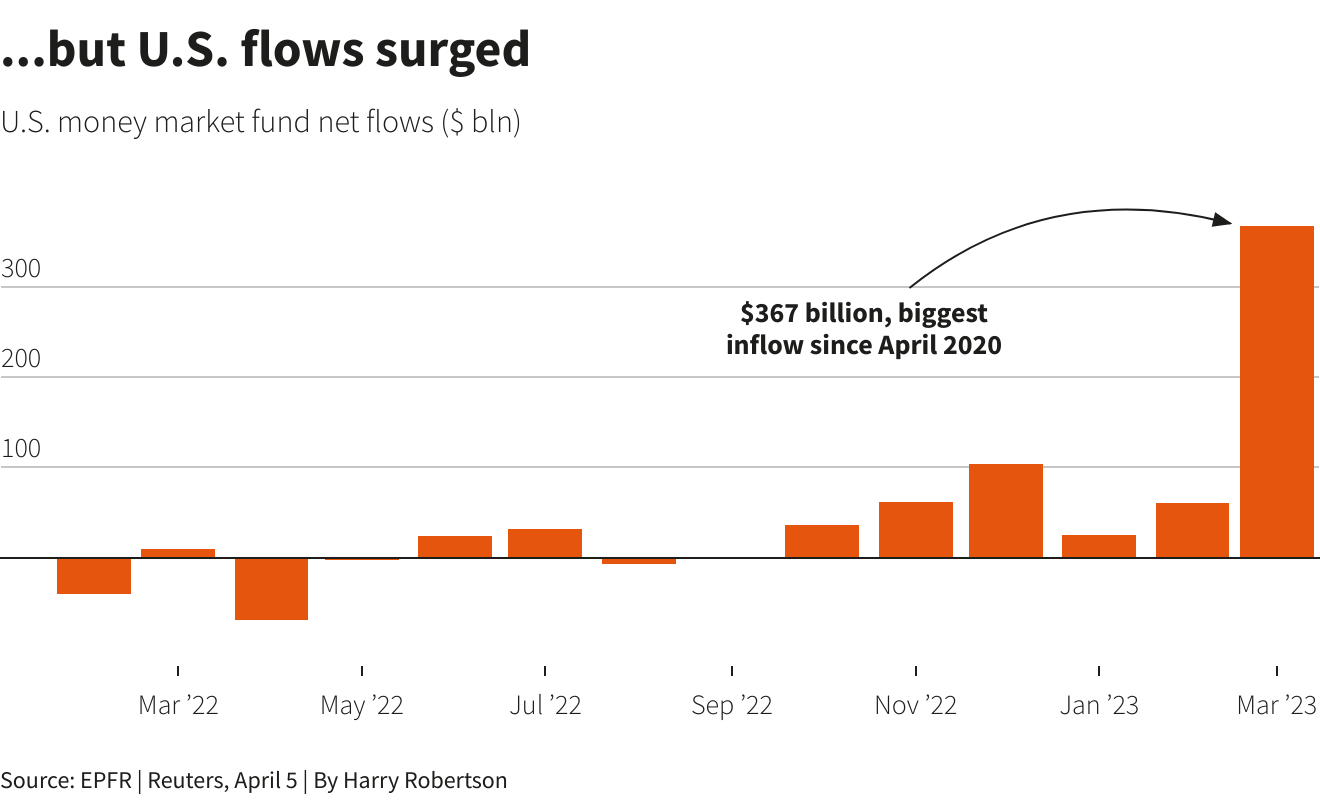

LONDON, April 11 (Reuters) – Investors poured $367 billion into U.S. money market funds in March, according to data provider EPFR, as the collapse of Silicon Valley Bank caused stocks to tumble and called the safety of bank deposits into question.

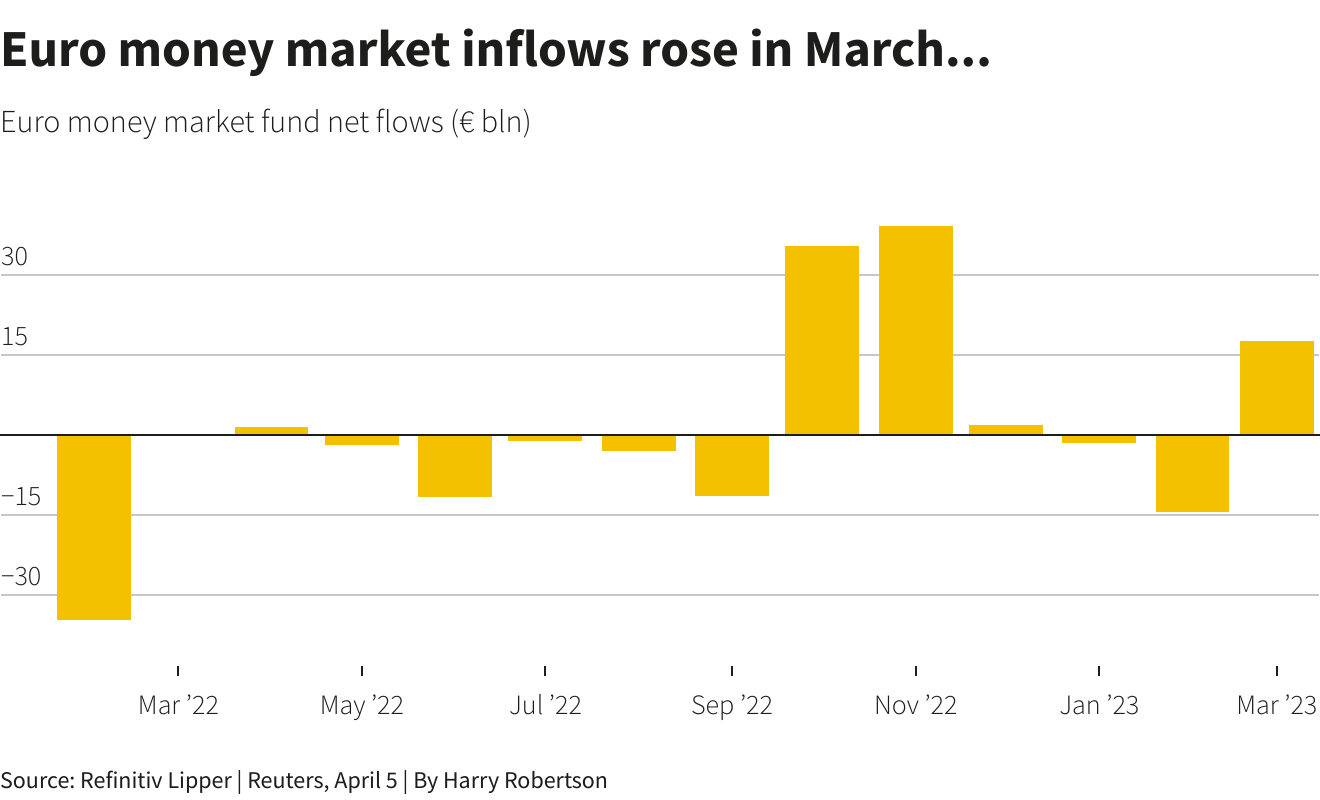

In Europe, investors put 17.7 billion euros ($19.35 billion) into euro-denominated money market funds in March, Refinitiv Lipper data shows, when the Credit Suisse crisis rocked markets.

That was a big jump from the previous three months, and the biggest inflow since November in the aftermath of the UK’s disastrous budget. But the inflows in Europe pale in comparison to the torrent that swept into U.S. funds.

The lower level of inflows suggests investors remained confident about Europe’s banks in general despite the collapse of Credit Suisse, some analysts said. Other analysts said it was due to the fact that euro money market funds are underdeveloped relative to U.S. funds and are focused more on private sector, particularly bank, debt.

WHAT IS A MONEY MARKET FUND?

A money market fund (MMF) is a mutual fund that invests in highly liquid – that is, easy to buy and sell – short-term debt products, such as those issued by governments or highly rated companies. Companies and investors see them as safe places to park cash.

The European money market fund sector is far smaller than in the United States. U.S. MMF assets surged to $5.2 trillion in March from $2.5 trillion in 2014 .

European-domiciled MMFs – including sterling and dollar funds – have grown from 1 trillion euros in assets in 2014 to around 1.5 trillion euros, based on data from the European Fund and Asset Management Association (EFAMA). Of that, around 40% are euro-denominated funds.

U.S. BANK NERVES

The huge flows into U.S. MMFs in March were driven in large part by companies and investors yanking their money out of banks, analysts have said.

Households and businesses pulled a record $174.5 billion from U.S. commercial banks in the week to March 15, as Silicon Valley Bank and Signature Bank both collapsed.

“The investor reaction would seem to suggest that investors have got more faith in European banks right now than they do in the U.S,” said Michael Metcalfe, head of macro strategy at State Street Global Markets.

European banks are also passing on interest rate rises more effectively, encouraging customers to keep their money locked up, JPMorgan strategist Nikolaos Panigirtzoglou said.

New deposits with an agreed maturity can earn 2.31% in the euro zone on average, compared with a European Central Bank interest rate of 3% and a yield on MMFs approaching the ECB rate.

In the U.S., one-year deposits return 2.24%, compared with the Federal Reserve’s interest rate range of 4.75% to 5%.

The latest European Central Bank data shows customers withdrew 143 billion euros from overnight deposits at euro zone banks in February, although they also put 83 billion euros into deposits with an agreed maturity of up to two years.

ECB board member Isabel Schnabel said in late March that euro zone banks had not seen a general deposit outflow despite the banking tremors.

THERE’S NOTHING LIKE THE U.S. TREASURY MARKET

Inflows into European MMFs did jump in March, showing that some companies and investors are drawn to them when things get choppy.

EPFR said BlackRock’s euro liquidity fund was the big winner, with more than 2.5 billion euros of inflows.

“We’re seeing that pick up ourselves,” said David Callahan, head of money markets at Lombard Odier Investment Management.

But Callahan also said some investors are nervous about putting their money into European MMFs, which are typically invested in bank debt.

Panigirtzoglou said around 90% of European MMFs are so-called prime funds that invest “heavily” in bank debt.

In contrast, he said almost 90% of U.S. MMFs only invest in U.S. government debt – a vast and ultra-safe market – giving investors more comfort during a crisis.

Federico Cupelli, deputy director for regulatory policy at EFAMA, said: “Sovereigns in the EU do not have the same credit standing, maybe except the German government. You can go back to the 2015 euro crisis to see why that is the case.

“So there’s fundamentally a lack of scalable alternatives existing in Europe. There’s nothing similar to the U.S. Treasury markets.”

HOW IMPORTANT IS REGULATION?

MMFs in Europe and the United States struggled with redemptions in some cases when economies went into lockdown to fight COVID-19 in March 2020, forcing central banks to inject liquidity into markets to avoid them freezing up.

The European Securities and Markets Authority (ESMA) has laid out suggestions for making the MMF market safer, including potentially getting rid of two types of funds that are seen as less stable, and increasing the amount of highly liquid assets that funds must hold.

But Cupelli said proposals that MMFs should hold more public debt bump up against the problem that there is not enough of that debt to go around.

And he said eliminating certain types of funds could limit the potential growth of the MMF market.

A top ESMA official said last month that reforms to tackle vulnerabilities in MMFs were urgently needed for the sector to cope better with economic shocks.

Reporting by Harry Robertson; Editing by Nick Macfie and Jane Merriman

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}