(Bloomberg) — European Union finance chiefs ended months of wrangling over fiscal rigor to agree on new rules that will aim to rein in debt and define the bloc’s ability to invest in key sectors such as defense for years to come.

Most Read from Bloomberg

In the end, the unanimous deal among 27 member states was clinched on a video conference that lasted less than two hours, concluding negotiations launched just before the Covid pandemic.

Wednesday’s agreement introduces more flexibility for fiscal adjustments, while Berlin succeeded in introducing safeguards to ensure common debt reduction and the building up of buffers to absorb future shocks.

The overhaul also aims to give capitals a bigger say in how they rein in public finances, while improving enforcement where limits are exceeded. Yet a goal of simplifying budgetary oversight proved elusive as the final compromise forced negotiators to add demands from each camp.

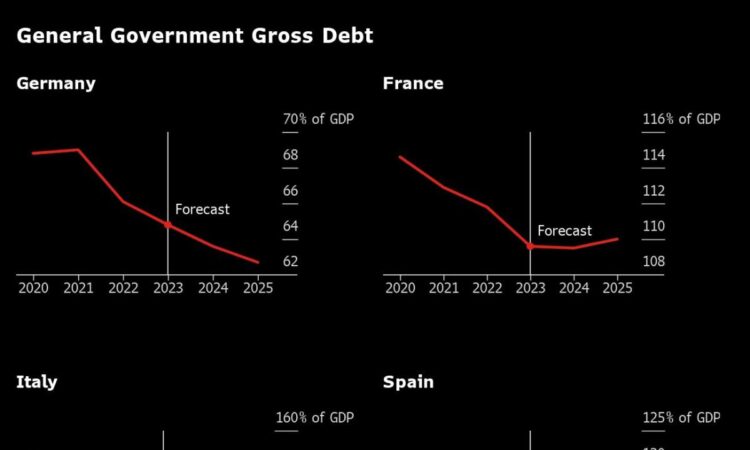

The fiscal rules that bind the euro area’s eclectic economies exist to bring down deficits and put limits on how much debt governments can build up. The old rules were suspended to allow spending leeway during the pandemic and energy crisis and are considered to be outdated.

“The rules are more realistic, they respond to the post-pandemic reality, and they incorporate also the lessons learned from the great financial crisis,” Spanish Economy Minister Nadia Calvino told a news conference after the deal was reached. Her country holds the rotating EU presidency and has been leading negotiations.

Efforts to agree on a new framework exposed differences between hawkish countries led by Germany that called for strict targets to reduce debt, and those led by France and Italy that were concerned about the need to finance the defense and digital industries, as well as the green transition.

After months of technical discussions led by Spain, Paris and Berlin resolved the remaining differences between the EU’s two biggest economies late on Tuesday with a deal they saw as the basis for the wider agreement.

“These rules will guarantee financial stability and sound public finances everywhere in Europe for the years ahead,” French Finance Minister Bruno Le Maire said in a video posted on the X social media platform. “For the first time in 30 years, this stability pact recognizes the importance of investment and structural reforms.”

Italy’s Giancarlo Giorgetti, who last week expressed doubts that a deal could be reached, said in a statement that the new framework is more realistic and called it a positive development.

On Wednesday’s video conference, finance ministers needed to finalize outstanding issues that included a key indicator based on net expenditure designed to monitor whether national economies are sustainable.

Member states also disagreed until the last minute over the pace at which deficits should come down to 1.5% of gross domestic product, with the aim of creating a fiscal buffer below the 3% threshold.

The new fiscal rules will grant member states some leeway on military spending as Russia’s invasion of Ukraine has brought defense to the top of the priority list. By investing in common EU priorities, including the green transition and digital and defense industries, the period during which a country has to balance its public accounts may be extended to seven years from four.

The old rules are due to be reinstated in January and left unchanged would bring back stricter debt limits that are tough for some governments to swallow. Ministers wanted a political deal before year-end to allow time to conclude the legislative reform by spring — ahead of EU elections in June — so it can be in place for the next budgetary cycle.

Negotiators from the EU’s main institutions will hash out the final details of the new economic governance framework before it’s put to a vote at the European Parliament.

–With assistance from Alessandra Migliaccio and William Horobin.

(Updates with Spanish economy minister comment in sixth paragraph, French finance minister comment in ninth, Italian finance minister comment in 10th.)

Most Read from Bloomberg Businessweek

©2023 Bloomberg L.P.

{kind=link}