LONDON, July 18 (Reuters Breakingviews) – Europe is providing a test of whether weak governments can enact strong policies. It has set firm goals to reduce carbon emissions by at least 55% by the end of the decade, before becoming carbon-neutral by 2050. European Union governments have agreed on the strategy, but they tend to paper over the short-term economic costs of the green transition. If they don’t come clean to public opinion, and explain how these costs will be shared, they may face crippling populist protests that will compromise their end goals.

Economists and scientists are in widespread agreement that the planet’s race towards net zero carbon emissions will lead the world to higher, more sustainable growth. They do, however, differ on the short-term costs generated by the acceleration of change, and the need to do by 2030 what governments failed to do for decades. The heatwave currently bringing scorching temperatures to southern Europe further underlines the need for rapid action.

French economist Jean Pisani-Ferry has compared the impact of the green transition to an economic shock equivalent to the sharp spikes in oil prices in the 1970s. Fighting climate change, he argues, amounts to putting a price on a resource – in this case, a stable climate – that for too long was available for free. But unlike previous shocks triggered by geopolitical instability or trade wars, the green transition has been initiated and managed by governments, and largely financed by them.

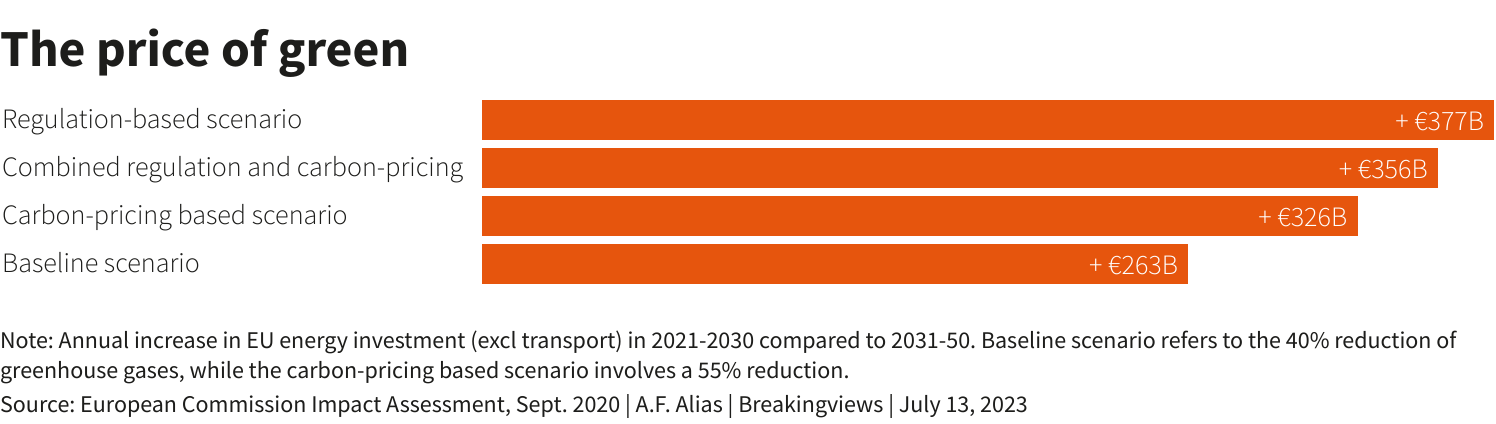

Past inaction has added to the bill. The amount of extra investment needed in the EU energy sector in 2021-2030, compared to the previous decade, would be in the range of 260 billion euros to 380 billion euros, or 1.5% to 1.8% of GDP, according to European Commission estimates.

The speed of the transition will also have an impact on growth and inflation. If the green investments replace other types of more profitable investment from governments, households or businesses, they could have a negative impact on growth. That’s because investments designed to cut down on fossil fuels do not, in and by themselves, increase productivity in the short term.

Furthermore, as noted by the International Energy Agency, the fall of investments in fossil fuel energy is not yet matched by a boost in renewable energy investments – a shortfall that could put further pressure on growth. It will take some time for prices and demand to adjust accordingly. More generally, goods and labour markets will be negatively impacted, in the next decade, by the speedy adjustments necessitated by the move to the zero-emission target. Some workers will lose their jobs, while some industries won’t immediately find the skilled workers they need. That increases the likelihood that inflation will remain above the levels seen in the decades before the pandemic.

The green transition also threatens to cause a major increase in inequalities if governments don’t devise transfers and subsidies to make it less painful for lower incomes. In France, for example, the cost of replacing a combustion engine car and a gas boiler with an electric vehicle and a heat pump would amount to roughly two years of income for the 20% of the population at the bottom of the revenue ladder, and still about one year for middle classes, according to a recent study by Pisani-Ferry and Selma Mahfouz for the French prime minister.

Governments will have to devise specific incentives and subsidies to avoid penalising those who have already suffered disproportionately from the economic impact of Covid-19 and two years of high inflation.

But state budgets will also suffer, making it more difficult to fund any public intervention. Tax receipts will decline as the switch to renewable energies reduces the take from levies on fuel and gasoline. In the UK, for example, that portion of tax revenue, which now amounts to about 1.2% of GDP, will halve by 2030 and disappear by 2050, according to the Office for Budget Responsibility.

Such short-term shocks could be absorbed in the name of longer-term benefits by governments that are politically strong, financially secure, and ready to warn about the sacrifices ahead and make sure they are fairly shared. But the three ways to finance the transition – taxes, spending cuts or more debt – are all problematic in Europe. France and Italy, with respective debt-to-GDP levels of 112% and 144%, can hardly borrow more. Countries such as the UK, with one of the lowest tax burdens in Europe, could consider raising the contribution of businesses or those on higher incomes – but are unlikely to do so due to political opposition.

Germany looks like the country most able to afford the green transition, but its over-emphasis on regulation on environmental matters is running into fierce opposition. A draft law to force new heaters to run on 65% renewable energy from 2025 – amounting to a ban on gas boilers – may not make it through parliament. Meanwhile the far-right AfD is now the second party in Germany, polling ahead of the ruling Social Democrats and Greens. Opposition to the government’s energy policies has become one of the main reasons sympathisers cite for their support.

On Sunday Paolo Gentiloni, the EU economy commissioner, told the Financial Times that Europe will have to fund its own industrial green transition. Yet, while renewing their pledges to abide by the Paris accord to reach net zero by 2050, European politicians keep ducking the question of how they will be able to finance it.

On the contrary, they seem to rule out, for political reasons, most ways to fund their plans. French Finance Minister Bruno Le Maire keeps pretending that he will not have to raise taxes to finance the green transition – and he rejected Pisani-Ferry’s proposal to introduce a well-flagged and temporary wealth tax for that purpose. German Finance Minister Christian Lindner refuses to take on more debt, while ruling out tax hikes. And in the UK, the opposition Labour Party has ditched its plan to invest 28 billion pounds a year in the green transition because its leader Keir Starmer believes he can only win the upcoming general election if he insists on his party’s fiscal prudence.

No major European government has been transparent about the trade-offs that will be necessary this decade or presented any idea on how to avoid adding even more pain for those at the lower end of the wealth and revenue ladder. In an ideal world, this should be part of a long-term plan that clearly spells out the choices and sacrifices ahead. But the fragility of most European governments – divided, threatened by populist unrest, and cash-strapped after three years of economic hardships – puts them in a difficult position to tackle that challenge.

Follow @pierrebri on Twitter

(The author is a Reuters Breakingviews columnist. The opinions expressed are his own.)

CONTEXT NEWS

Southern Europe is bracing for temperatures to reach record highs in the coming days because of a powerful heatwave.

The weather warnings issued in Italy, Spain and Greece highlight the continent’s challenges as it fights global warming.

Europe will require investments of more than 700 billion euros a year to meet its energy transition goals to combat climate change, the European Commission said on July 6. The amount includes 620 billion euros to meet the objectives of the European Union’s Green Deal and its REPowerEU plan, and 92 billion euros to address the objectives of the Net-Zero Industry Act over the 2023-2030 period, the Commission said in its 2023 Strategic Foresight Report.

Editing by Francesco Guerrera and Oliver Taslic

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

{kind=link}