It is a new dawn for asset manager CQS Investment Management, founded 25 years ago by Michael Hintze. It was recently acquired by Canadian financial behemoth Manulife.

For the time being the CQS brand remains, although Lord Hintze has exited the show, taking with him the flagship hedge fund he has long managed. So, it is very much business as usual for CQS, an investment business renowned for its management of credit (CQS stands for convertible and quantitative strategies).

Yet CQS also possesses another string to its bow. It has a natural resources investment team which runs three investment funds.

Between them, the team – comprising Ian Francis, Robert Crayfourd and Keith Watson – manage investment trusts Geiger Counter (investing primarily in uranium equities), the tiny Golden Prospect Precious Metals fund (£29 million capitalisation) and CQS Natural Resources Growth and Income.

The three funds remain somewhat in the shadows – a result of the dominance of rival resources funds such as the £1.1billion BlackRock World Mining, which tend to catch the eye of powerful wealth managers looking to invest clients’ money. It part explains why shares in all three trusts sit at double digit discounts to the value of their underlying assets.

For investors, this potentially provides the opportunity to make additional gains if these discounts narrow – although there is no guarantee of this happening. Over the past five years, shares in the three trusts have traded at a discount more often than not.

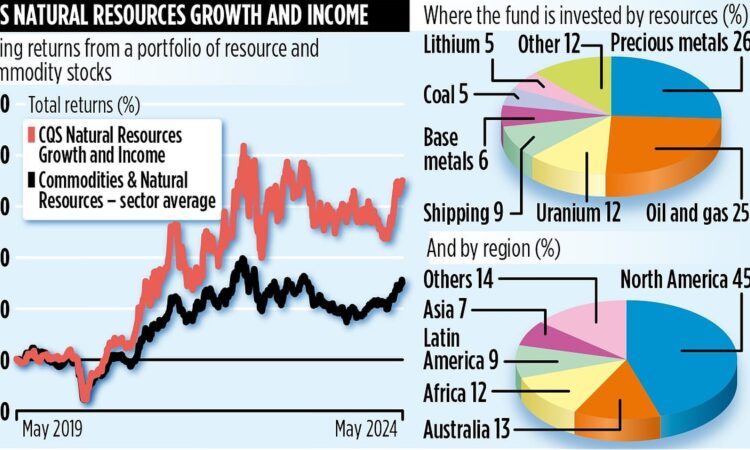

The Natural Resources Growth and Income fund is the more established of the three. Launched in June 2003, this £127 million trust, listed in the UK, invests across a broad spread of international companies with business interests in the mining or extraction of a broad church of natural resources.

Related Articles

HOW THIS IS MONEY CAN HELP

Its investment record is stellar. Over the past five years, it has provided shareholder returns of 187 per cent. Over the past year, it has delivered a return of 18 per cent. By comparison, the respective returns from BlackRock World Mining are 142 per cent and 2.8 per cent.

What makes the trust different from rivals is its focus on mid-sized and smaller companies – so it is not interested in traditional energy-related stocks such as BP and Shell which it believes investors can buy easily and hold as standalone investments in their portfolios.

The result is a fund littered with stocks unfamiliar to the eyes of most UK investors – listed in the US, Canada and Australia. Shale oil companies are a strong investment theme. ‘We like the US shale oil producers,’ says Crayfourd. ‘Their activities are onshore and so have acreage in terms of expansion. Yes, the world is going electric, but it still needs oil.’ Among the fund’s top ten holdings is US shale oil producer Diamondback Energy.

Apart from oil and gas stocks, which represent a quarter of the trust’s assets, the other big sector play is precious metals.

‘We like gold as an asset,’ says Keith Watson. ‘The gold price is supported by strong central bank buying in countries such as China. If western investors get the appetite for gold, the price should continue to rise.’ Australian listed gold miner West African Resources is a top ten holding.

The trust pays a quarterly dividend. For the first three quarters of its current financial year, it has been set at 1.26 p a share. This is equivalent to an annual income of around 2.9 per cent.

Ongoing annual charges are high at 1.8 per cent (source: Association of Investment Companies).

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

{kind=link}