By Adam Luck and Tom Kelly for the Daily Mail

22:01 25 Apr 2023, updated 22:01 25 Apr 2023

- UK pensioners put cash into what they were told were ‘safe and low risk’ funds

- They trusted the funds because of the respected institutions promoting them

- But most of the investments were high risk, sold by unlicensed financial advisers

- Pensioners often charged management fees even after the value had collapsed

Hundreds of British pensioners have launched a £120 million compensation battle after accusing two major investment firms of promoting a notorious fraud.

They allege Friends Provident International (FPI) and Utmost International ‘turned a blind eye’ to a raft of risky investments, including a scam that saw an ‘utterly dishonest’ solicitor jailed for 14 years.

Pensioners told Money Mail they were left suicidal, with retirement dreams in tatters, after putting their cash into what they were told were ‘safe and low-risk’ funds which they trusted because of the respected institutions promoting them.

In fact, most of the investments were high-risk and sold by unlicensed and unregulated financial advisers, according to the claim, but were nevertheless approved to use online accounts with both financial giants to assess the state of their investments.

In a further blow, the pensioners say FPI and Utmost often charged them thousands of pounds in management fees even after the value had collapsed.

Between 2006 and 2013, people put their savings into investments marketed and sold as an ‘insurance policy’ or ‘bond’ by the financial giants, which effectively acted as a vehicle for a series of high-risk funds.

Most investors were approached by independent financial advisers through word of mouth but were shown branded corporate literature from the investment giants promoting the funds.

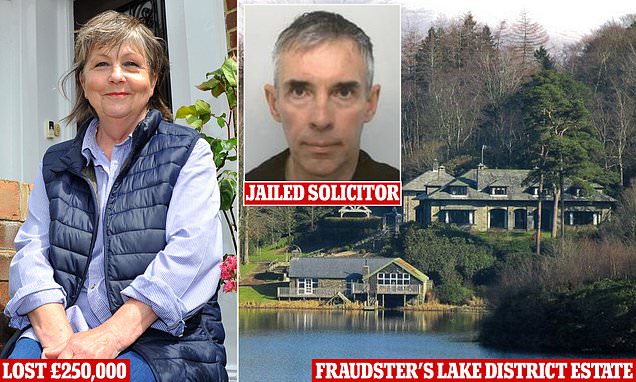

One of these funds included the Axiom fraud, in which solicitor Timothy Schools fleeced £20 million from investors to fund a luxury lifestyle, including buying a £5 million shooting estate.

Related Articles

HOW THIS IS MONEY CAN HELP

Others included speculative property developments which either collapsed or lost significant value.

Both FPI and Utmost, previously known as Skandia, Old Mutual International (OMI) and Quilter International, now claim in court papers that they had no obligation to check out the funds that collapsed and have blamed investors and the financial advisers.

But Money Mail has seen a brochure produced by FPI for potential investors which boasts the company makes sure that fund managers ‘go through due diligence’ when assessing investment opportunities.

A similar one produced by Skandia said ‘we deal only through professional advisers’ who should ‘fully understand’ the products being sold.

The pensioners also claim they were told the investment firms were regulated by the City watchdog, the UK Financial Services Authority (FSA, which has since become the Financial Conduct Authority, FCA). But they later discovered because the firms are in the Isle of Man, there is no such protection.

One couple who lost £250,000 went to the Isle of Man Ombudsman only to be told they couldn’t get the cash back. They were offered just £200 to make up for Skandia’s poor customer service.

Architect Andrew Walters and his wife Sharon Huyshe have had their dreams of retiring in Greece left in tatters after they used cash from the sale of their Sussex home to make the investment. Andrew, 68, has abandoned retirement plans and is now stuck working seven days a week.

Sharon, who lives in Hythe, Kent, says: ‘It destroyed everything. We had to sell the house we’d bought in Greece, return to England and go back to work. Money saved over a lifetime of hard graft just vanished.’

Their adviser promised the bond they invested in was low-risk, but it turned out to be a high-risk investment which rapidly collapsed, costing them a huge part of their nest egg. But Skandia continued to charge annual fees of around £8,000 a year.

Bob Blackman, the chair of the All-Party Parliamentary Group on Personal Banking and Fairer Financial Services, says the group will investigate the case.

He says: ‘The established, credible brands of Friends Provident and Old Mutual would have played a part in winning the trust and confidence of investors in these cases, to their eventual regret.’

Alan Parry, 72, a retired quantity surveyor, lost £500,000. He invested in various funds in 2012 through OMI, or Skandia as it was known at the time.

This included £200,000 in Axiom. He says: ‘Surely, OMI and FPI have a duty of care to make sure that these funds promoted on their platforms are genuine and not run by criminals.’

Stephen Mitchell, 65, from Surbiton, was ‘absolutely devastated’ when he had to abandon retirement and return to work in insurance after losing £125,000.

This included £10,000 in Axiom, through both FPI and OMI.

He says: ‘I was told it was a guaranteed money-maker. I thought the companies would at least do some due diligence on the funds.’

OMI states in its defence that ‘it did not undertake… any due diligence in relation to the risk or suitability of… assets’ and FPI said it had never ‘implied’ it had done ‘due diligence’ on the assets.

Thai-based independent financial adviser David Mills, who gave a witness statement to the claimants’ lawyers, says that FPI agreed to work with his firm despite the fact it was unlicensed to operate in Thailand.

He says that FPI representatives had told him their products were ‘rock solid’ and the funds on their platform gained their approval after appropriate due diligence.

More than 700 claimants have signed up for the class action, which is being led by Signature Litigation and is expected to come before the Isle of Man courts next year.

FPI claims that it only has to follow FCA rules ‘in so far as it related to its business in the United Kingdom’.

Because these products were largely sold outside the UK, FPI believes that it has acted legally but is not bound by the FCA.

Utmost states it left the FSA in 2012.

Both Utmost International and FPI declined to comment but deny any liability.

moneymail@dailymail.co.uk

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

{kind=link}