All three UK equity sectors are now among the highest returning of the year, Trustnet finds.

UK smaller companies funds have jumped to the top of the 2024 performance charts thanks to “sellers’ exhaustion”, a recovering economy and increasing mergers and acquisitions (M&A).

According to FE Analytics, the average fund in the IA UK Smaller Companies sector made a 10.8% total return over the first five months of 2024 – making it the highest-returning peer group.

The average smaller companies fund is even beating the IA Technology and Technology Innovations and IA North America sectors, which have been buoyed by the continued strength of the Magnificent Seven stocks.

The IA UK Equity Income and IA UK All Companies sectors hold fourth and fifth places year to date, with respective average returns of 8.5% and 8.1%.

Average return of Investment Association sectors over 2024 so far

Source: FinXL. Total return in sterling between 1 Jan and 31 May 2024.

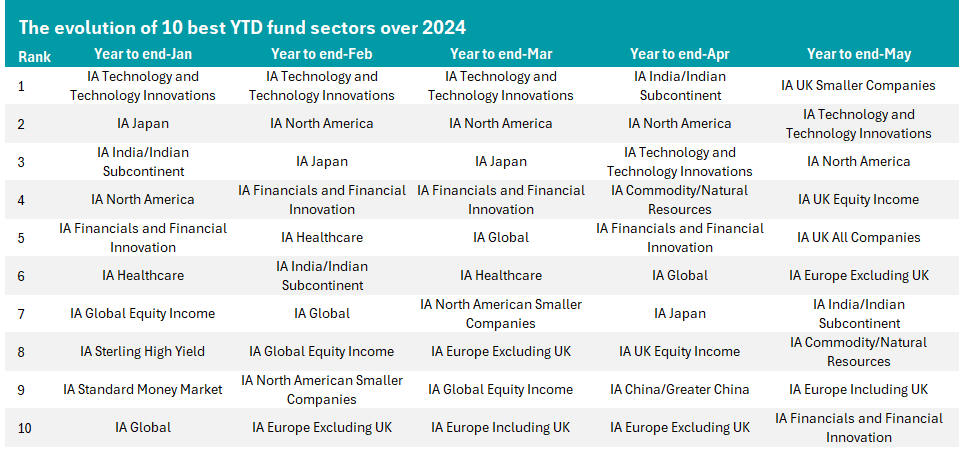

This is a stark turnaround from earlier in the year, when the three UK equity sectors were much lower down in the performance tables, and is down to some strong returns from the UK in May.

Simon Evan‑Cook, fund manager on the VT Downing Fox multi-asset range, said: “The asset class has been so hated, and therefore heavily sold, that there are just fewer disillusioned souls left to sell them down.

“This is borne out by talking with our fund managers, who tell me that stock prices are no longer being eviscerated if the company reports slightly disappointing results. This had been the norm for the last few years, and this change in behaviour has the ring of sellers’ exhaustion to it.”

Source: FinXL

Rob Morgan, chief analyst at Charles Stanley Direct, added: “This rally has been a while coming. The area has long been cheap but what it lacked was a catalyst to break through persistent negative sentiment and reverse the flows out of UK assets that had been depressing share prices.”

He said a number of factors have combined to “tentatively” turn the performance of UK funds around, one of which is an improvement in the domestic economy. Although the UK’s economic numbers are “still not great”, they are better than many feared and support improving sentiment.

“When things seem very negative, a bit of good news goes a long way,” Morgan said.

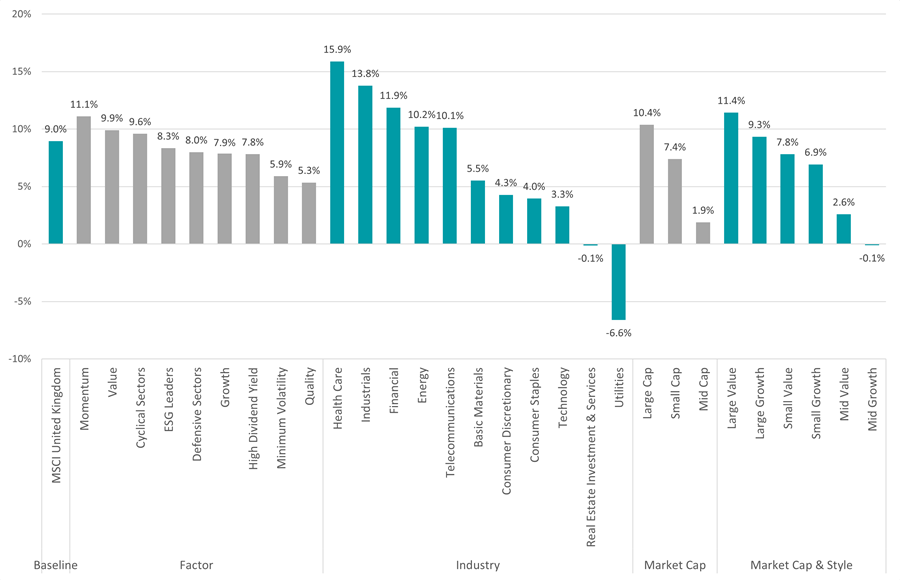

He also pointed to positive trends at a company level. FTSE 100 companies with international-facing businesses have benefitted from the strength of the US dollar, which increases the sterling-dominated earnings and has led strong company results. Meanwhile, sectors such as energy, mining and defence, which are big constituents of the UK market, are benefiting from rising demand.

Snapshot of UK equity market over 2024 so far

Source: FinXL. Total return in sterling between 1 Jan and 31 May 2024.

Both Evan‑Cook and Morgan credited increased M&A as a positive for the UK. Years of underperformance from UK stocks has left them attractively valued when compared with international peers, leading to a series of approaches.

“In UK small-cap world it’s become common to hear the refrain ‘they’re so cheap that if you don’t buy them, somebody else will’,” Evan‑Cook said. “Turns out that was true, because all of a sudden corporate and private equity buyers are snapping up UK companies like it’s the end of an episode of The Apprentice.”

Morgan also argued that this creates a halo effect that bolsters sentiment towards the whole market, not just the target businesses themselves.

While all these factors are supportive of UK equities, they may have had a disproportionate impact on smaller companies.

“As the most undervalued parts of the market, UK small- and micro-caps have risen the most as sentiment has turned,” Morgan explained. “It’s also where liquidity is more limited so even a little bit of an uplift in interest can have a big impact.”

But whether the recent rally has legs is a more difficult question.

Morgan expects the M&A theme to continue to underpin valuations, but said it may not boost all stocks equally. Buyers such as private equity investors look for very specific characteristics in a target company, so the main beneficiaries would likely be active managers who are seeking the same qualities and who thereby end up owning natural M&A targets.

“Meanwhile, more extensive than expected interest rate cuts is a tide that would lift all the boats. Unfortunately, it isn’t that likely, but the gradual impact of lower interest rates further out should still help,” he finished.

“Finally, for UK small-caps the performance of the domestic economy is influential. Expectations are pretty low, so continued growth, albeit at a sedate pace, would create a benign environment.”

{kind=link}