Despite the handwringing and doom-mongering of many UK talking heads, there is little issue with equity capital market liquidity in London.

According to Dealogic data, the UK was the second top global exchange nationality for ECM volumes in 2Q, behind the US, driven by large capital raisings by listed companies, like National Grid’s GBP 7.2bn rights issue, and a GBP 1.6bn sell-down in LSEG itself.

Equity sellers, in large, already listed, names have little trouble finding vast pools of investor capital to fund ambitious capital expenditure plans or take huge chunks of stock on an overnight block trade.

The question is how to attract new innovative growth companies to London and what is the exchange’s unique USP as it comes to grips with its post-Brexit reality.

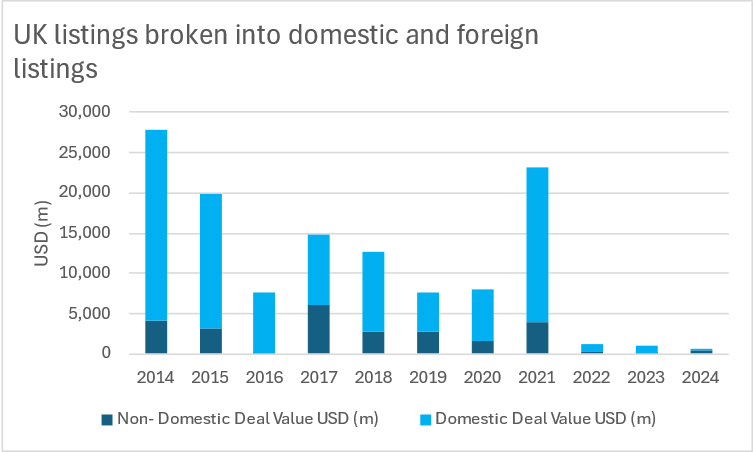

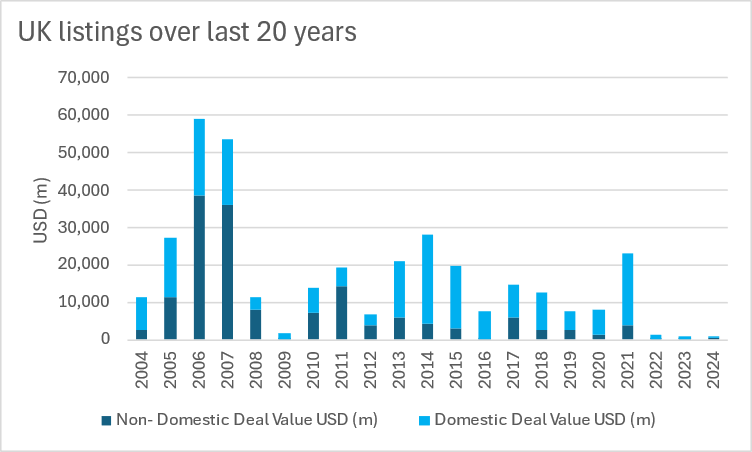

Will London remain an international hub? Or will it have to rely on a flow of domestic listings? It has struggled to get much traction in either, over the last three years.

Source: Dealogic

Bringing UK regulation in line with the US

As London aims to find its place on the global stage post-Brexit and high-profile companies such as ARM Holdings [NASDAQ:ARM] chose the US over London for their IPO venues, the UK made several efforts in recent years to revitalise the market, with a series of attempts at adjusting the regime, Lord Hill set out plans for the UK to reimagine itself as a home for innovative growth companies in the UK’s Listing Review, published in March 2021.

The Financial Conduct Authority published its feedback in December 2021 and signed off on a number of implementations including reducing the minimum free float for a premium listing from 25% to 10%.

The FCA also pledged to allow for a “targeted form” of dual-class share structures within the premium listing segment to encourage innovative, often founder-led companies, onto UK public markets.

Dual class structures though, alongside other mooted reforms, have faced significant resistance from some asset managers and UK pension funds on investor protection grounds.

But ECM practitioners argue that dual-class structures along with the other changes will put the UK in line with the US, where many of the investors complaining already allocate capital.

The FCA has consulted on a new round of measures and is due to report back on in the second half of 2024. These involve moving to a disclosure-based regime, rather than prescriptive rules, which includes removing the need for a shareholder vote on class 1 transactions.

Alasdair Steele, corporate partner and head of ECM at CMS explained that the disclosure regime will make it easier for companies to consider an IPO with a view to conducting roll-up strategies without the need for shareholder approvals and a class 1 circular, making consolidation easier. Without these changes, a company may prefer to remain private, he explained.

Cultural shift required

UK-based ECM practitioners have been largely positive about UK market reforms. But there is a firm sense that the true key to revitalising the LSE is in attracting vast pools of pension capital to the market.

The government has made some early attempts to encourage this.

Under UK Chancellor Jeremy Hunt’s Mansion House Compact of 2023, 10 UK pension funds have agreed to the objective of allocating 5% of their capital to “growth companies”.

Ariel White-Tsimikalis, a partner at Goodwin Proctor, pointed out that this includes AIM-listed stocks.

“Whilst it would be good to see more institutional investment into public equities and growth stocks in particular, it will be helpful to start somewhere,” she said.

“Investors shifting to higher growth companies will foster innovation,” White-Tsimikalis said. “There are great companies in the UK and once more institutional investors can see they can make money from them, this should lead to a deepening of the risk appetite in the long run.”

ECM practitioners agree that London needs a change in investing culture. For all the focus on the reforms on the stock market, ultimately it is the investors that need a change in mindset, with pension funds favouring other asset classes over equities.

According to data from the think tank New Financial, in a 2023 report sponsored by Abrdn and Citi, just 6% of UK pension fund assets were allocated to UK equities in 2021. This slipped from 39% in 2002.

Steele pointed out that although the Mansion House Compact is pointing in the right direction, there will be little incentive for the likes of pension funds to allocate to UK-listed stocks unless they are mandated to do so.

This is linked to the backlash investors face for losing money from UK pension pots on risky assets. Practitioners pointed out this stigma has grown over the last thirty-plus years following the Robert Maxwell pension fraud in the 90s and losses felt during the credit crisis, leading to UK investors favouring dividend yield stocks over risky growth assets.

A UK JOBS ACT

London is wedded to a past of being a top international exchange for global companies to list. The pipeline for potential IPOs though has a more domestic feel to it.

Over the past three years, the number of international companies listing in the UK has shrunk. Non-domestic IPO volumes were just USD 26m in 2023; this year has already surpassed that number following the USD 358m IPO of Air Astana [LON:AIRA]; the Kazakh carrier is down almost 15% from the IPO price.

While domestic IPO volume has fallen significantly since 2021, volumes surpassed USD 1bn in both 2022 and 2023, so there is some hope at least of encouraging more UK companies to market.

Domestic deals also don’t necessarily mean worse, or less exciting companies, for investors.

The top domestic listing this year has been the GBP 172.9m IPO of Raspberry Pi [LON:RPI] which raised GBP 166m, representing 30.7% of its ordinary shares at 280p, and was trading at around 401 pence per share at the start of June, a 43% jump in its value.

There are hopes that other interesting small and mid-cap IPOs might follow.

A key to UK market revitalisation may not lie in attracting mega foreign listing, but leaning in on its domestic strengths.

White-Tsimikalis said that listing rule changes are already having an impact, encouraging companies to re-consider listing in London as the IPO window begins to creep open.

She flagged the US Jumpstart Our Business Startups Act (JOBS ACT), signed into law by US President Barack Obama in 2012, which eased US securities regulation in order to promote business growth and equity investment in startups.

“NASDAQ wasn’t always what it is, the JOBs Act played a critical role in fostering growth companies to go public in the US. I believe with the current UK listing regime overhaul, we are having our own JOBS Act moment in the UK,” White-Tsimikalis said.

The US law had its own critics at the time, with many consumer groups and investor associations saying at the time it would fundamentally reduce investor protections.

Sound Familiar?

“We all need to get behind this London’s success and be cohesively involved,” White-Tsimikalis said. “Focusing purely on Day 1 valuations is only half the story and risks will be perpetuating a negative narrative, we need to support a stronger funding continuum for UK innovation especially the innovation coming out of our academic institutions.”

“The direction of our times is for London to be a destination for innovative growth companies to list,” she said. “There is no reason London can’t be the Nasdaq of Europe,” she said.

London is still a premier global exchange, but the relative attractiveness of any given global stock market will ebb and flow with fashion and trends.

Truly long-lasting reform will be for the UK to create a culture where vast pools of domestic pension capital can support new champions to and beyond a stock market listing.

London needs a whole punnet of Raspberry Pis.

“The next government needs to have a cascade effect through the economy, once that is going in the right direction, and things are considered stable,” Steele said. “People will feel more confident in the UK, then people will invest more in the stock market,” he added.

It is a challenge, but for any government looking to reinvigorate UK financial services, it is one they must grasp with both hands.

{kind=link}