Impacts of the Expiration of Federal Child Care Stabilization Funding and the Mitigating Effects of State-Level Stopgap Funding | CEA

Introduction

The March 2021 enactment of the American Rescue Plan provided historic federal funding to the child care industry. The unprecedented $24 billion in subsidies to providers helped to stabilize the industry during the COVID-19 pandemic, while also addressing preexisting challenges in the market for child care. The flexibility of the funds helped providers stabilize their businesses in one of the most tumultuous periods in recent history.

In November 2023, the CEA published a working paper that evaluated the impact of the child care stabilization funds allocated by the American Rescue Plan. The working paper largely focused on the onset of those funds and found that the child care stabilization funds accomplished their eponymous goal of stabilizing the industry, resulting in increases in wages and employment for child care workers, as well as increases in the labor force participation rate (LFPR) and employment for mothers of young children.

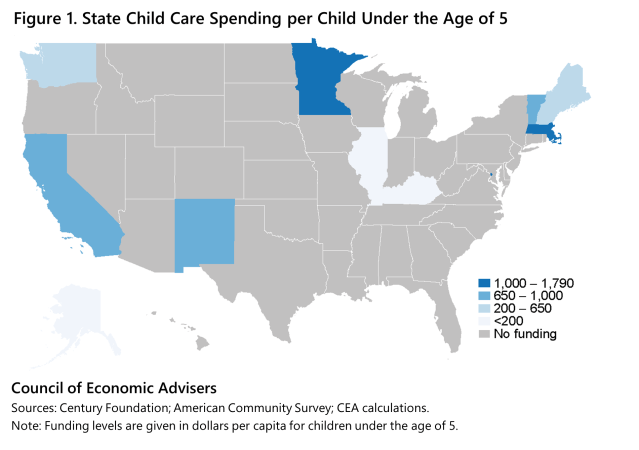

The end of June 2024 marks nine months since the child care stabilization funds formally expired. As the child care industry is one that often operates on slim margins and has historically been unable to provide enough affordable slots for families (U.S. Department of the Treasury, 2021), the expiration of funds posed a threat to the positive progress made. Recognizing this threat, eleven states plus the District of Columbia have implemented some level of “stopgap funding” to fill the gaps left in child care funding when federal dollars from the American Rescue Plan ran out. We define “stopgap funding” as state-level (or district-level in the case of DC) funds —usually via state-level budgetary processes—for stabilization purposes, which often take the form of direct grants to child care providers. Figure 1 shows the level of state stabilization as defined by spending per child under the age of 5 (i.e., the age group most likely to benefit from the funding).

Given limited follow-up data on outcomes in the post-funding period at the time of publication, CEA’s original analysis could only examine preliminary impacts of the expiration of ARP child care stabilization funding—finding suggestive evidence of a slowing of the growth in maternal labor supply that started with the onset of ARP funds. This issue brief updates and extends that analysis with new outcomes and more data to examine the effect of the expiration of funds on child care prices, maternal labor supply, and survey-based measures of access to child care. We also leverage data on state efforts to stabilize child care, which helps us understand if, and how much, state-level funding supported the child care industry when federal funds expired.

Our results suggest an overall slowdown in progress on outcomes such as child care prices and labor force participation and employment for women who are likely to rely on child care. We also show early evidence that states that implemented stopgap funding after federal ARP dollars ran out may have been more resilient in the post-funding period (after October 2023). Survey evidence shows that families with young children are having a harder time finding child care after ARP expiration, but the effects are less pronounced in states that implemented stopgap funding. Moreover, we find suggestive evidence of relatively stronger labor market outcomes for families and parents with young children in these states. We conclude with a summary of actions taken and proposed—in the President’s FY 2025 Budget—by the Biden-Harris Administration to increase access to and affordability of child care for parents across the country.

The Child Care Market and the ARP Stabilization Funds

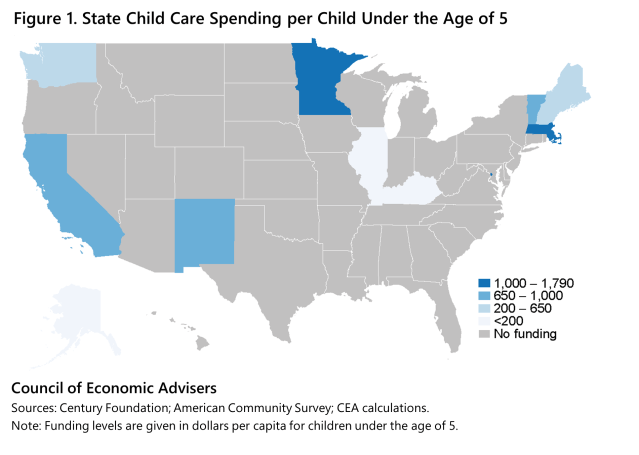

The CEA has previously detailed the importance of access, affordability, and quality in the child care market. With roughly 60 percent of children under the age of six in the United States spending some time in nonparental care on a regular basis, the ability of parents to access affordable care has economic benefits for families and society as a whole. There is extensive research relating access to child care and maternal labor supply (Blau and Tekin 2007; Gelbach 2002; Herbst 2017; CEA 2023). Consistent with this, employment in the child care industry (a proxy for the size of the industry) over the last three decades has largely grown in tandem with the female labor force participation rate among 25–54 year-olds. Figure 2 shows the rapid increase in both indicators up to the early 2000s. At this time, prime-age female LFPR stagnated and child care employment began to decline. Both began to see a resurgence in the later 2010s and have started to recover following the COVID-19 shock. Ultimately, the ability of mothers, and parents more broadly, to participate fully in the labor force is often dependent on the extent to which child care supply can meet families’ growing demand at a price they can afford.

The majority of child care in the United States is provided by the private market (Child Care Aware, 2023) and the business model is fragile. Child care is very labor intensive and state and local regulations, seeking to provide high-quality care, often stipulate the required ratio of children per adult in a classroom (Workman, 2018; Childcare.Gov). The average child care center has 3 to 4 adults per classroom serving roughly 10 children under age 3, and 6 to 7 adults in classrooms serving about 17 children between ages 3 and 5 (National Survey of Early Care and Education, 2023). As such, care providers must choose a wage at which they can attract enough teachers to be in compliance with state standards while also charging a price that families can afford to pay. This often results in a gap between what families can afford and the cost of providing quality care (US Department of the Treasury 2021; CAP 2023). In other words, there is a fundamental imbalance in the child care market, where the structure of the market is such that, left to itself, the market will invariably provide too few affordable, quality slots to enable families with low or even middle incomes to be able to access it.

On top of these pre-existing structural challenges, the COVID-19 pandemic took a particularly high toll on the industry. While the pandemic kept parents and children at home, many child care providers lost the entirety of the revenue base that helped them stay afloat: between February 2020 and April 2020, child care employment fell more than 30 percent. This is more than double the economy as a whole, which saw a 13 percent decline in employment.

Recognizing the persistent disruptions of the care infrastructure wrought by the pandemic, the American Rescue Plan (ARP) Act allocated additional funds to stabilize the supply side of child care, including $24 billion in funding for the new Child Care Stabilization Program—roughly $12 billion per year. For comparison, the child care and development fund (CCDF)—the country’s largest federal funding stream dedicated to affordable child care—was funded at just over $8 billion in 2019 and $9.5 billion in 2022 (after upwards adjustments in response to the pandemic) (Bipartisan Policy Center 2023). Supply side interventions are important in an industry where capacity constraints are binding. Although many lower-income households would likely qualify for subsidized care, these constraints contribute to low participation rates among eligible families.[1] The U.S. Department of Health and Human Services estimates that in 2019, roughly one in six children eligible for care benefits received them.

Data indicate that more than 225,000 child care programs in the United States, with total capacity to serve as many as 10 million children, received funding through stabilization grants intended to help the industry recover by providing funds to child care programs to help cover operational costs such as wages and benefits, rent and utilities, and program materials and supplies (White House 2023). Many states report that these funds went towards personnel costs at centers, and rent and utilities at family child care homes. In short, these funds went towards reducing the direct cost to families as well as increasing the capacity of child care centers to meet demand for care.

Summary of Previous Results

The original 2023 CEA analysis relied on carefully chosen comparison groups to isolate the causal effect of stabilization funds on outcomes of interest. The first part of the analysis provided evidence that the stabilization funds were effective at increasing child care access. Specifically, it showed that the stabilization funds led to lower relative price growth in the child care industry, more child care workers (a proxy for increased supply), and higher wages for child care workers.

The second part of the 2023 analysis, sought to identity the causal effect of this stabilization on maternal labor supply. Using mothers with children over age 6 or women without children (those less likely to benefit directly from the funds) as a basis for comparison, the labor force participation of mothers of young children (under 6 years old) increased by between 2 and 3 percentage points after stabilization funds were made available. Because (a) all women would have been affected by underlying trends such as working from home and (b) these relative changes occur right after ARP stabilization, these patterns likely reflect the effect of ARP child care stabilization net of other potentially confounding factors.

Results Part 1: Exhaustion of Federal Funds

The expiration of the stabilization funds on September 30, 2023 potentially led to an unravelling of the gains documented in the original CEA analysis. Here we examine some of these effects.

Impact of ARP Expiration on Prices

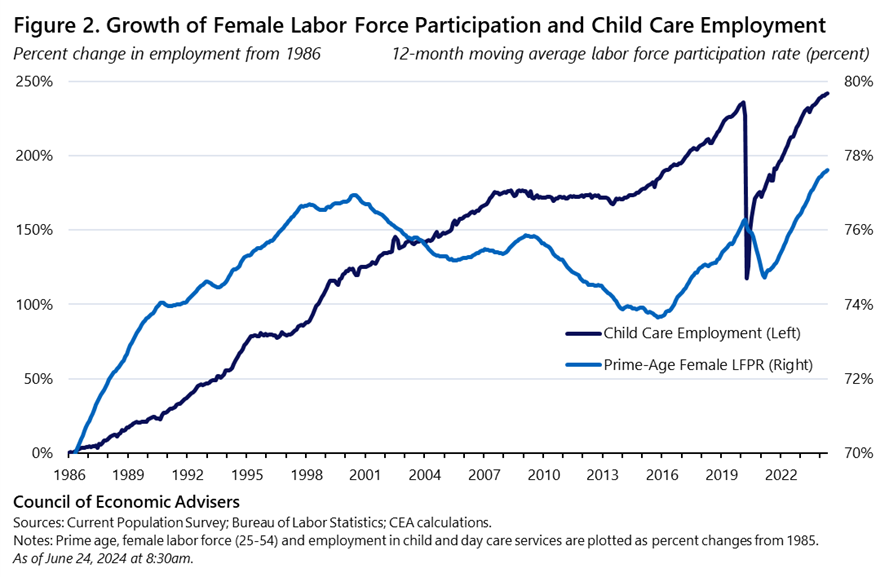

Looking at prices, Figure 3 shows the difference between predicted child care prices and actual prices faced by families during this time. To estimate the predicted versus actual prices, we use a similar bundle of service prices between 2016 and 2019 to estimate the trend of child care prices in normal times. This prediction represents our best guess of what child care prices would have been given the evolution of other prices at the same time. Even during a time characterized by price turbulence during the COVID-19 pandemic, this prediction methods succeeds in accurately predicting child care prices; Figure 3 sets the difference between actual and predicted prices equal to zero in January 2019 and the difference stays largely stable until early 2021. After the onset of ARP funds, the relative price of child care declines significantly. Despite significant changes to care arrangements over the course of 2020 and 2021, with the popularization of work from home and hybrid work, we would not expect to see such a sharp decline in prices due to depressed demand for care specifically in the months when ARP stabilization funds onset. The timing of the funds coinciding with price changes is strong evidence of a relationship between prices and the distribution of stabilization funds.[2]

With several months of follow-up data after the expiration of ARP funds, we can now see that after these funds expire, we begin to see a stagnation of price declines. In late 2023 the difference in predicted versus actual child care prices reverses course and the gap between child care prices and the similar bundle of services began to shrink. Despite a short follow-up period, this indicates stalled progress on child care pricing in the wake of ARP funding expiration. This stagnation could restrict access to child care for low-to-middle-income families.

Impact of ARP Expiration on Maternal Labor Supply

We now turn to maternal labor supply. The original CEA analysis shows that these original price declines coincided with an increase in the labor force participation rate of mothers of young children (relative to mothers of older children). The analysis, which we extend in this brief, relies on several facts to inform the empirical strategy: mainly that the child care industry primarily serves children under the age of 6, while most children 6 and older attend primary and secondary school. If parents and families are constrained in their ability to participate in the labor force by their inability to find and/or pay for child care, then the increased supply of child care enrollment slots and lower prices resulting from an influx of federal funds such as the ARP stabilization funds should have a positive impact on the labor market outcomes of mothers with young children (under the age of 6).

In the results that follow, we identify three groups for comparison. The “treated” group, or the group that should be most directly and significantly affected by the stabilization funds, are women with children under the age of six. We identify two relevant comparison groups: first, mothers of older, school-aged kids, and second, women with no children. To the extent that we think all three of these groups would be similarly affected by underlying labor market or macroeconomic shifts (such as general trends toward work from home or shifts in the macroeconomy), any divergence in outcome trends between women with young kids and women with older or no children around the time that child care stabilization funds are exhausted can plausibly be attributed to the expiration of funds.

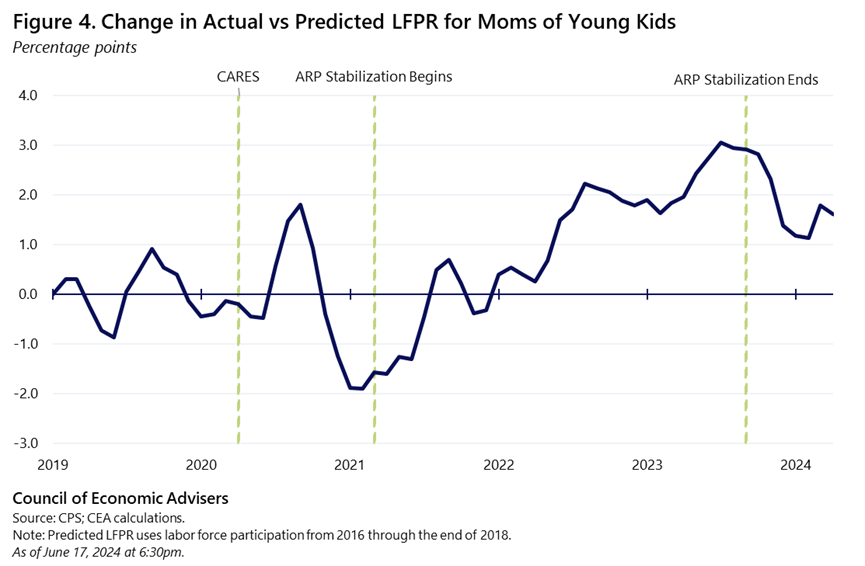

Figure 4 shows how the labor force participation rate (LFPR) among mothers with young kids (our treated group) evolved in relation to mothers of older children and other women. We use a similar, prediction approach in this analysis to show that, in comparison to the LFPR trends of our comparison groups, labor force participation among mothers of kids under 6 showed significant growth after the onset of ARP stabilization funds (the topic of our original work) and has slowed significantly compared to control group LFPR since the exhaustion of these funds. Similar to the price comparison in Figure 3, we use LFPR from 2016 through the end of 2018 to predict how LFPR would have evolved in the absence of the onset of ARP funds. Like Figure 3, the prediction does a reasonable job of predicting LFPR before the pandemic. In 2020 we see a modest increase in LFPR soon after the CARES funding is distributed, before the LFPR of mothers of young kids drops precipitously in the middle of 2020 (relative to other women). However, only after ARP funds are distributed does actual LFPR start to increase and exceed the prediction range — indicating that, at the onset of ARP stabilization, women with children under the age of 6 participated in the labor force at a higher rate than predicted (based on the behavior of mothers of older children and women without children). By late 2023, the actual LFPR of this group is well above what would have been predicted–compelling evidence that the ARP stabilization funds allowed mothers of young children to participate in the labor force at a higher rate. At the point of funds expiration (the third dashed green line), however, this overall trend changes and we see an actual decline in LFPR. While not conclusive evidence of a slowdown or reversal of progress, this is the longest sustained period of slowdown since the onset of ARP funds and may portend what is to come.

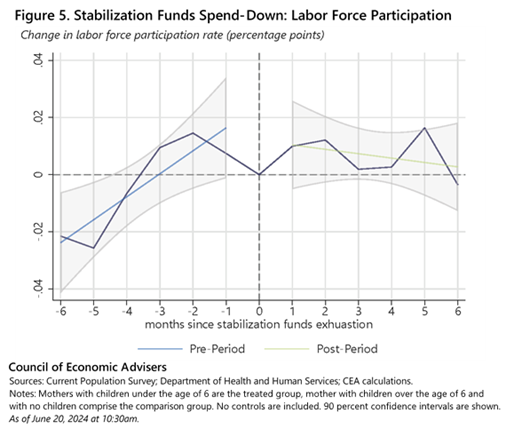

While the national trends are compelling, we also examine county-level data to see if the timing of the relative slowdown at the county level coincides with the timing of when funds ran out. We use data from the Department of Health and Human Services (HHS) to estimate LFPR impacts at the county level which allows us to identify when individual states and counties liquidated all ARP funds: some states may have spent down the funds earlier than others. The ARP stabilization funds had a liquidation date of September 30, 2023, meaning that all funds needed to be spent-down or distributed by states before the September deadline. Spending data from the HHS allows us to see when states distributed funds at the county level. Unlike the onset of funds, which was highly concentrated in the first few months of the program, the final distribution of funds at the county level varied widely. Our analysis isolates the effect of the expiration of funds by comparing the labor force participation of mothers of young children to that of women in counties that reached final spend-down before and after the point of exhaustion of funds. The resulting estimates have a causal interpretation so long as labor force participation among our treated group (mothers of children with young kids) and our comparison groups would have trended in parallel in the absence of ARP stabilization funds, and that there weren’t any coincident changes that affected mothers of children under six when ARP funds were exhausted.

Figure 5 plots the trend in relative LFPR for mothers of young children over time. The x-axis is the month relative to the last distribution of ARP funds to a given county; we use this payout date to roughly approximate when the county will have spent down all their ARP stabilization funds. Negative values indicate months before fund expiration and positive value are the months after. Figure 5 shows that the relative increase in labor force participation shown in the original analysis slows to a halt around the time of expiration of funds. While we do not see a significant decline in labor market outcomes as the result of exhaustion of funds, any significant progress for women of young children can be seen to stall as the child care market slows its expansion. As in the onset of funds analysis, these results are robust to using either the combined control group (mothers of older children and women with no children) or the comparison of mothers with younger children to mothers with older children. It should be noted that the results presented in Figure 5 show that labor market outcomes appear to stall before the final payout of funds from states to counties. This early effect could be attributed to the possibility that payments made are for services rendered and any expansion of the market stalls before the final official payment.

Impact of ARP Expiration on Access to Care

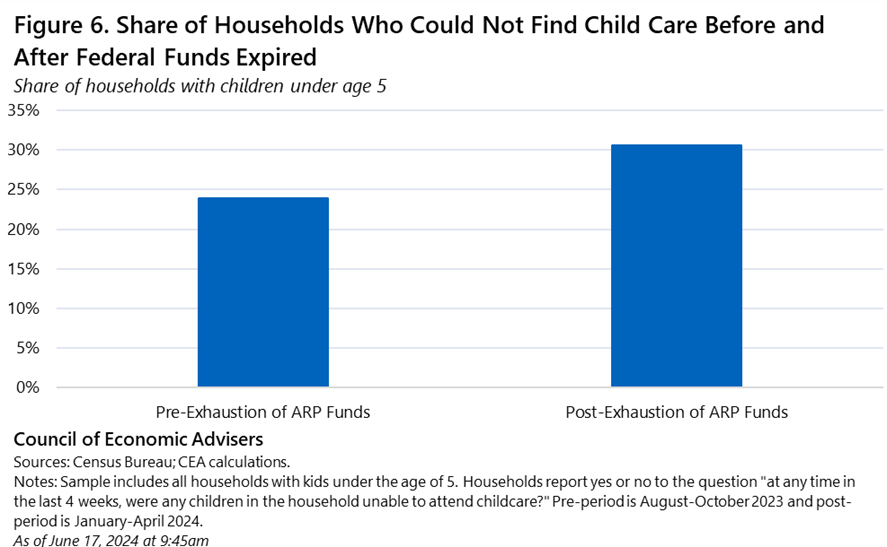

As a final piece of corroborating evidence that the expiration of funds affected the supply of child care, we use data from the 2023 and 2024 Census Household Pulse survey (referred to as “the pulse survey”) to understand the extent to which demand for child care is being met across the country. Albeit suggestive, insofar as the expiration of funds led to a contraction or slowing of the growth of the child care sector, one would see more families reporting difficulty finding child care after October 2023 than before. The survey data, summarized in Figure 6, show exactly this. Figure 6 represent the share of respondents (households with children under the age of 5) who report being unable to find child care in the last four months due to issues with cost, distance, safety, or supply. Figure 6 shows that across the country, the share of households who could not access care increased from 24% to 31% after the expiration of ARP funds (between Q3:2023 and Q1:2024).[3]

Results Part 2: Difference By Stopgap Funding

State-Level Funding Initiatives

Anticipating these potential, negative effects, many states have implemented some form of what we refer to as “stopgap” funding: state-level funding that fills the role of the expired federal funding. Eleven states plus the District of Columbia have made significant state investments in child care programs and providers. In this section of the brief, we focus on states that have, through their state legislature, dedicated funding specifically for “stabilization” purposes, meaning that these are direct grants or solutions for providers similar to the structure of ARP funds.[4]

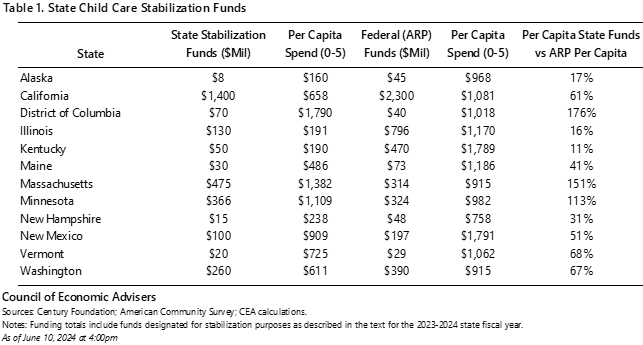

Table 1 outlines the level of spending across states that implemented stopgap funding. The second and third columns show the level of per-capita spending where per capita is limited to the under age 5 population—i.e., the group that the funds will most likely be spent on. The District of Columbia, Massachusetts, and Minnesota allocate the most, per-capita. All three spend upwards of $1,000 per child under five, with DC topping the list at nearly $1,800 per child.[5] These are also the three states in which the state-level funding exceeds that allocated by the federal ARP funding scheme. DC spends nearly twice as much, per capita, as the ARP funding whereas other states, such as Alaska, Illinois, and Kentucky have implemented lower levels of funding that amount to less than 20% of ARP funding. These funding discrepancies across states mean that stopgap funding will likely have varying effects based on how much of the budget holes left by the ARP funds expiration these state funds account for. Indeed, we find that states that provided at least a one-to-one match of federal ARP funds saw limited disruption to progress made following the original inflow of federal funds to providers.

As mentioned above, eleven states plus the District of Columbia have taken legislative action to introduce comparable, state-level funding in place of federal ARP dollars. These funds are meant to be similarly utilized as “stabilization” funding, i.e., directly supporting child care providers in meeting demand for care.[6]

Impact of State Stopgap Funding on Access to Care

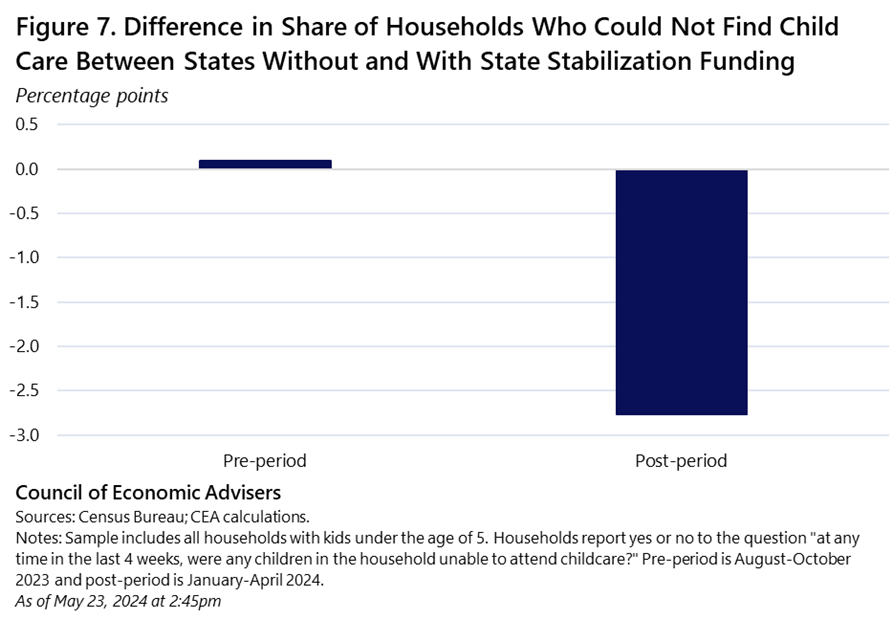

To shed light on whether the stop gap funding made states more resilient, we first examine change in the reposes to the pulse survey for stopgap and non-stopgap states. That is, Figure 7 shows the difference in access to care before and after the expiration of funds between states that implemented stopgap stabilization funding and those did not. In the pre-period (when federal ARP funds were being distributed), states with and without state-level stabilization funds, nearly identical shares of households reported that they were unable to access child care. After federal funds ran out, families in states that failed to implement stopgap funding were nearly 3 percentage points more likely to report having trouble accessing care. If we believe that, in the absence of stopgap funding, states that introduced funding would have trended similarly to those that did not, we can conclude that the stopgap funding aided in mitigating the loss of access to care. While this relationship is not dispositive, it shows that stopgap funding has likely helped maintain access to affordable care.

Impact of State Stopgap Funding on Maternal Labor Supply

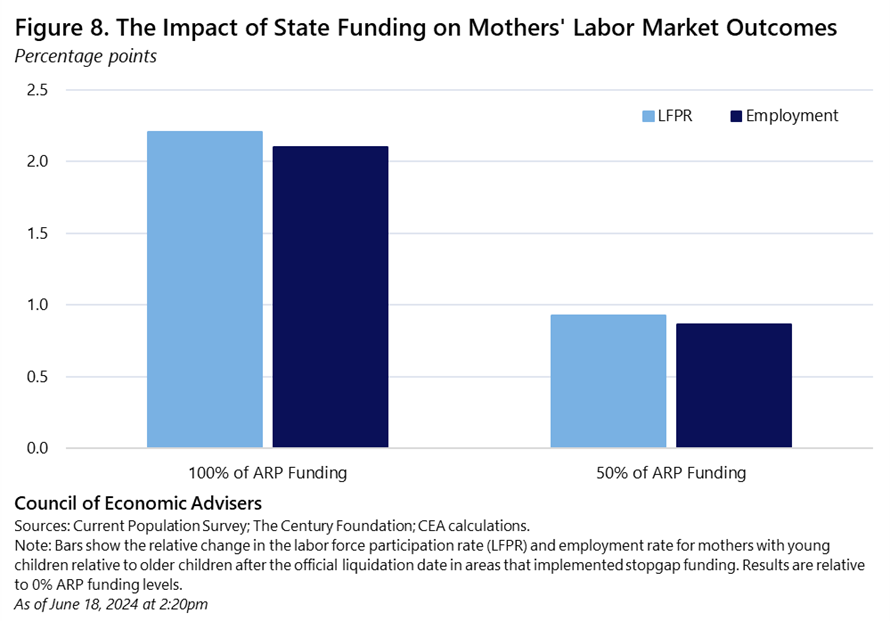

Now we turn to labor supply. We provide early suggestive evidence that these differences in access to child care between stopgap and non-stopgap states may be leading to differences in maternal labor supply. To assess this, as before, we rely on the difference in outcomes between mothers of young children (treated) and mothers of older children. If the stopgap funding led to increased ability to access care, which in turn increased the labor supply of mother of young children, one should observe that the LFPR of mothers of younger children (the treated group) relative to that of mothers of older children (the comparison group) would increase in stopgap states relative to non-stop-gap states at the expiration of ARP funds. Moreover, this relationship should be more pronounced in state that had larger stop gap amounts. We test this notion using a regression model and find evidence of this.

Consistent with stopgap funding continuing the relative gains from ARP funding, our regression model indicates that in states that replaced about 50 percent of ARP funding, the change in LFPR for mothers of young kids was 1 percentage point higher than that is areas with no stopgap funding, and in areas that replace the ARP funding level fully, the change in LFPR for mothers of young kids was nearly 2.5 percentage point higher than that in areas with no state funding (Figure 8). These results are nearly identical for the employment rate. Coincidentally, the effect of fully replacing the ARP funding level is very similar to the effect of the onset of these funds. Although these results are only marginally statistically significant, they are suggestive that the access issues highlighted in the Household Pulse survey are bearing out in the labor market, putting mothers and families with young children at elevated risk compared to other women. It is important to note that these results should be taken as simply suggestive evidence of slowing progress in the post-federal funding period. We use only states that implemented state-level stopgap funding that accounts for at least 50% of federal ARP funding. There are also states that could be implementing other family-friendly policies to aid families in accessing affordable child care.

Discussion and Conclusions

The American Rescue Plan made a historic investment in the child care industry. The funds were allocated to stabilize a critical industry during unprecedented times. This investment, however, was always meant to be temporary, and there was broad-based concern about the impact of the expiration of funds on child care providers, parents, and children. This brief highlights the stalled progress as a result of expiring ARP funds, which evidence suggests is leading to higher prices and depressed access to child care for families who need it most. The Biden-Harris Administration has called on Congress to provide $16 billion in supplemental funding to extend the ARP funding and provide relief to child care workers and the families that depend on them.

The findings underscore the need for sustained, transformative federal investments to ensure affordable child care is available to all families that need it. The Biden Administration has proposed such a program in the President’s most recent budget, which would create a historic program offering guaranteed, affordable, high-quality care from birth to kindergarten for families making up to $200,000 per year: most families would pay no more than $10 per day and the lowest income families would pay nothing. The Administration stands ready to work with Congress on a long-term solution that ensures all families can access affordable, high-quality care and education.

In the absence of action from Congress towards this proposal, several states have stepped up funding to providers at the state-level, which—as this brief shows—has had significant, positive effects on families and parents. Despite positive effects of these state efforts, it is not sufficient. As such, federal investment is necessary to aid a market that has long been plagued by staffing, cost, and access issues for providers and families. This brief shows that the ill-effects of expiring ARP funds will stall progress without further action, and underscores the importance of child care providers, not only for children and families, but for the economy at-large.

[1] Other factors contributing to low participation include limited funding for subsidies and high family copayment rates.

[2] It should be noted that, although the national expiration date occurs between September and October 2023, our later analysis highlights that counties and states spent down their funds in various months before the deadline. The expiration of funds date should be seen as fuzzy in Figures 3 and 4, which may contribute some noise to the estimates provided.

[3] Ideally, we would test that this relationship only holds in the pre- and post-ARP stabilization funds period. As the question of access to child care was only posed to households over the given dates, however, we are unable to run this falsification test.

[4] This definition is consistent with recent research from the National Women’s Law Center.

[5] It should be noted that DC represents a unique case in that not all children participating in child care in DC may represent DC residents. Considering the considerable labor spillover into the District from surrounding states such as Maryland and Virginia, this may be an overestimation of per capita dollars.

[6] It should be noted that, similar to the ARP stabilization funds, not all state funding is ongoing. Some states will see a significant shift away from state funding in the next fiscal year.

{kind=link}