LONDON, March 10 (Reuters) – New rules in Europe to crack down on greenwashing are not making it easier to spot genuine environmentally-friendly funds as asset managers continue to apply different standards for what constitutes sustainable investing.

More than 30 fund managers, consultants, lawyers and regulators interviewed by Reuters said that despite European Union rules demanding more disclosure, funds remained hard to compare and greenwashing difficult to spot.

A surge in demand for green investments has led to a rush by investment managers to label products as sustainable, when often portfolios still include carbon-intensive businesses.

The European Commission has tried to provide more clarity with its Sustainable Finance Disclosure Regulation (SFDR), initially launched in March 2021, which aims to outlaw misleading claims.

Last year, the Commission clarified the rules to require fund managers dedicated to pursuing sustainable investments — known as Article 9 funds under the SFDR — to have 100% of their portfolio in environmentally-friendly companies.

Latest Updates

View 2 more stories

The SFDR defines sustainable investment as contributing to “an environmental or social objective”, assessed by indicators such as use of raw materials or production of waste.

The regime got tougher in January with more detailed disclosures required to resolve problems identified since the rules were introduced.

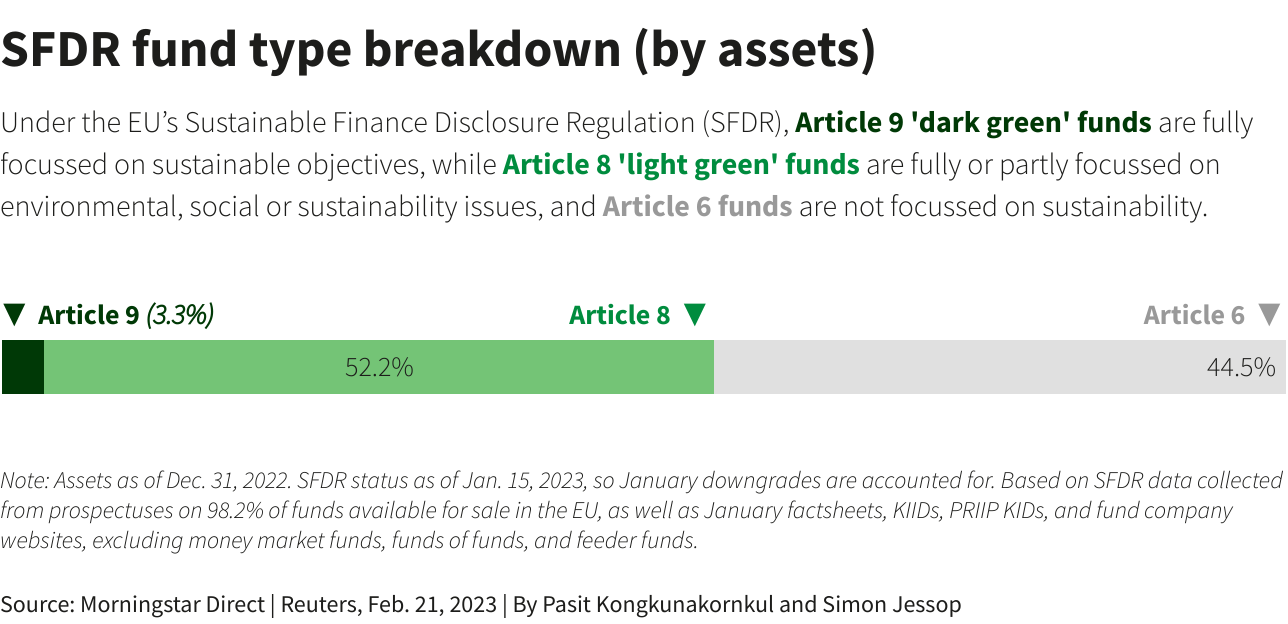

But the Commission’s latest efforts have not cleared up the greenwashing muddle for funds domiciled in the EU and governed by the SFDR, which had a face value of 8.4 trillion euros ($8.88 trillion) at end-December, according to fund management specialist Morningstar.

The people Reuters spoke to said discrepancies among fund portfolios reflected a lack of clarity from the Commission over what constitutes a sustainable investment.

“One of the objectives was to fight greenwashing and we are really at a stage now where the way the regulation is being implemented doesn’t help prevent it,” said Mathilde Dufour, head of sustainability research at French asset manager Mirova.

The Commission’s changes aim to plug gaps that allowed funds branding themselves as sustainable to invest in everything from oil to tobacco.

In response, many funds downgraded the classification of their funds at the end of last year from Article 9 to the less demanding Article 8, which requires sustainability to be only one of the factors informing investment decisions.

Alena Kosava, head of investment research at AJ Bell, one of Britain’s biggest retail investment platforms, said the current lack of clarity and transparency meant investors were vulnerable to paying higher fees for funds that may not deliver on their advertised green status or fairly reflect the underlying sustainability risks.

“Article 9 can often be offered at a premium and could be seen as a cash cow [for managers] but investors cannot often be certain that fund groups are doing what is necessary,” she said.

INCONSISTENCIES

The new regime has not resolved the inconsistencies in the portfolios claiming green credentials.

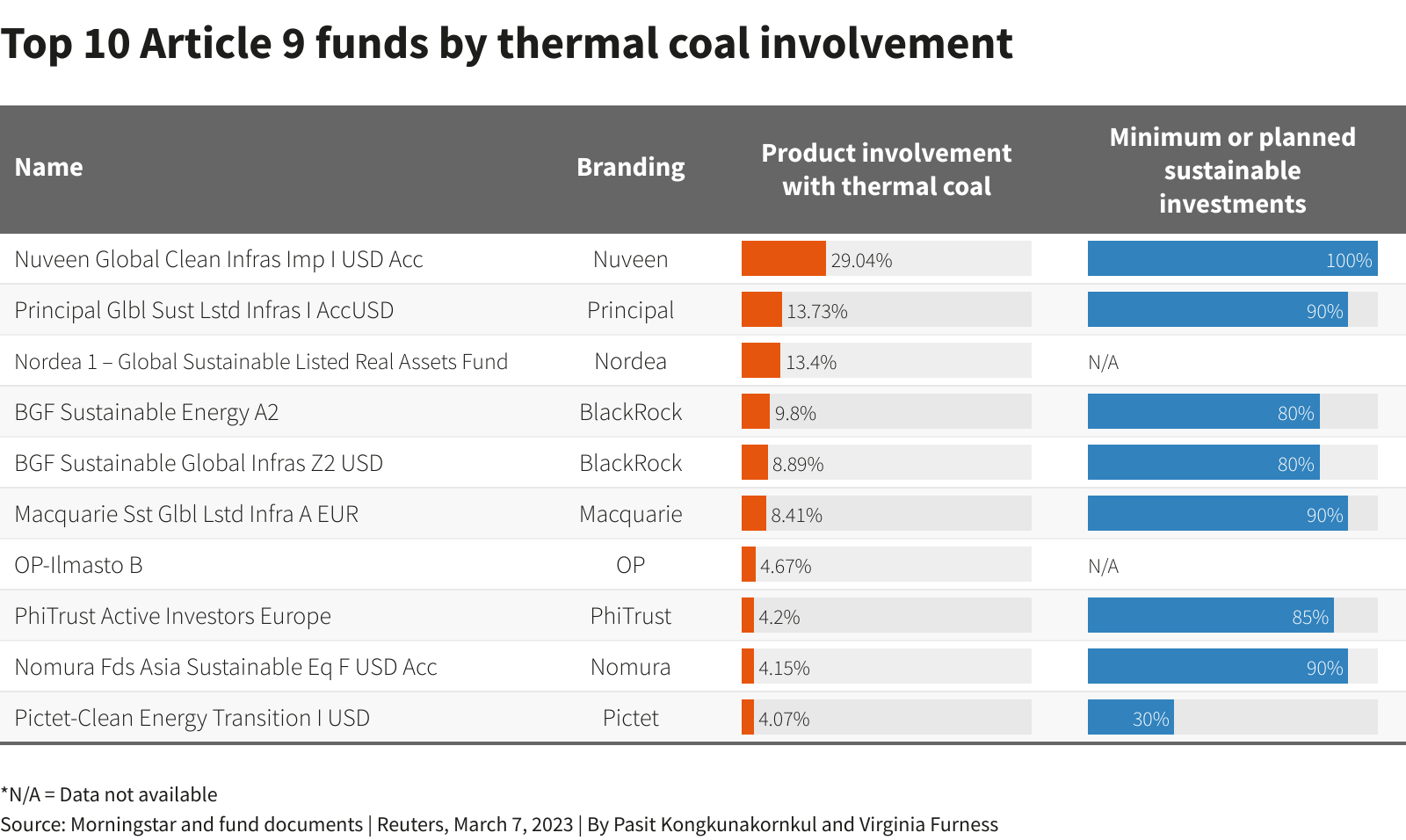

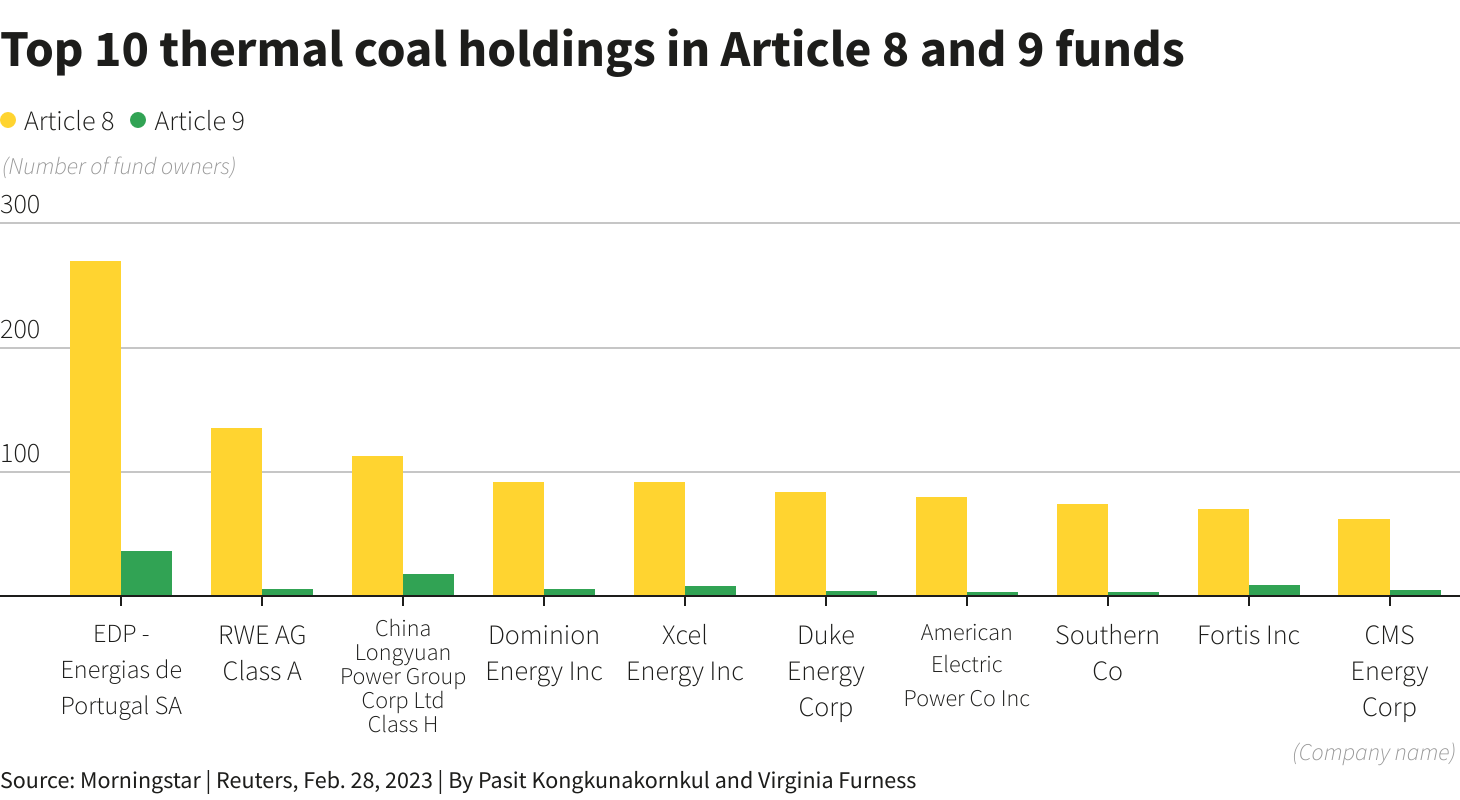

For example, data provided to Reuters by Morningstar shows that as of mid-January more than 100 out of 891 Article 9 funds in Europe were invested in some aspect of thermal coal, a big climate change contributor.

In the Nuveen Global Clean Infrastructure Impact Fund, for example, 29% of companies were directly or indirectly exposed to thermal coal, which Morningstar said could be through activities such as mining, coal-power generation or providing services to the sector.

Nordea, BlackRock and Macquarie also run funds which had over 8% exposure to the fuel, the Morningstar data showed.

A Nuveen spokesperson told Reuters it applied revenue threshold limits to investing in coal-based power generation, but declined to specify what they were. They also said the investments were justified to facilitate “an orderly and effective energy transition”.

Eric Pedersen, head of responsible investments at Nordea Asset Management, also said the investments were in line with its energy transition planning.

A Macquarie spokesperson said its fund’s coal exposure was linked to power generation investments where the companies had agreed to phase out its use.

A BlackRock spokesperson said its fund’s exposure “was linked to legacy power generation investments where the companies are investing heavily into renewable energy, which is helping decarbonise electricity generation for the economies they serve.”

There is no explicit rule against thermal coal in Article 9 and the market is seeking clarity from the Commission on whether any fossil fuel investments have a place in an Article 9 fund, Hortense Bioy, global director of sustainability research at Morningstar, said.

The French financial regulator proposed in February that Article 9 should exclude fossil fuel activities that are not aligned with the EU’s taxonomy, a list of environmentally friendly activities.

TEMPERATURE GAUGE

MSCI, the finance industry data provider, has developed a way of checking on investment funds’ green credentials with its ESG Implied Temperature Rise tool.

This is used by the funds industry, while some fund managers also have their own versions to keep track at the portfolio level.

When analysed using MSCI’s tool, 16 of the 20 biggest Article 9 funds, as ranked by Morningstar, are not currently aligned with a goal agreed by governments in 2015 to limit global warming to 1.5 degrees Celsius.

The MSCI tool assesses the funds’ portfolio emissions relative to the maximum amount of carbon that can be emitted globally and still hit the world’s climate target.

Among them, for example, are BlackRock’s Sustainable Energy Fund, Nordea’s Global Climate and Environment Fund and Pictet’s Global Environmental Opportunities Fund.

Pictet Asset Management’s head of ESG Eric Borremans and Nordea’s Pedersen said implied temperature rise estimates in general are methodologies in their infancy and should not be used on their own to assess the sustainability of a fund’s portfolio.

BlackRock declined to comment.

SUSTAINABLE OR NOT SUSTAINABLE

Mirova’s Dufour said Article 8 funds now accounted for more than half the European market and deployed a wide range of strategies that were particularly hard to compare.

Stuart Ballard, head of product strategy and development at asset manager Federated Hermes, said the SFDR’s loose definition can result “in one asset manager considering a particular stock to be a sustainable investment and another asset manager not considering that to be a sustainable investment.”

The Commission said in December it would answer some of the questions posed by investors “early next year” and would begin a “comprehensive assessment” of SFDR.

When asked for comment by Reuters, a Commission spokesperson made reference to the December speech by Commissioner Mairead McGuinness. The Commission did not respond to a further request for comment.

LACK OF ENFORCEMENT

National regulators in EU member states, responsible for monitoring the SFDR enforcement, have only sanctioned a handful of funds for breaches.

Denmark’s market watchdog in February ordered eight funds to take remedial action after finding they had violated SFDR because of insufficient disclosures.

Henrik Brarup Damgaard, Director, Head of ESG supervision at the Danish market regulator, said: “There are some areas where there has been a need for dialogue with the industry and where the Commission has or will be providing further guidance.”

A spokesperson for the financial regulator in Ireland, home to a substantial number of funds, told Reuters it was reviewing local fund disclosures, as are regulators in Luxembourg, the EU’s largest fund hub.

A spokesperson for Luxembourg regulator the CSSF said the development of the regulatory framework had triggered an increase in demand for products with sustainability features, but there was generally no binding definition of greenwashing available in the EU regime.

“The characterisation of what constitutes a sustainable investment under the SFDR is also a concept that needs further clarifications at European level.”

($1 = 0.9463 euros)

Reporting by Virginia Furness and Simon Jessop in London; Graphics by Pasit Kongkunakornkul;

Editing by Greg Roumeliotis and Jane Merriman

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}