[1/2] An eagle tops the U.S. Federal Reserve building’s facade in Washington, July 31, 2013. REUTERS/Jonathan Ernst

NEW YORK, May 15 (Reuters) – A default on U.S. Treasury debt would be a leap into the unknown for the Federal Reserve’s ability to conduct monetary policy to achieve its job and inflation goals.

That’s because U.S. government bonds are the key to how the central bank sets its short-term interest rate target. Anything that gums up the Treasuries market could scramble those mechanics.

The Fed uses Treasuries for many key operations. Setting a baseline for short-term interest rates via its reverse repo facility in effect borrows cash from money market funds in transactions collateralized with government bonds. The Fed can also borrow or buy Treasuries to keep its federal funds rate at the targeted level.

Treasury Secretary Janet Yellen has said the government could run short of the funds needed to pay all its bills as soon as early June if the debt ceiling is not raised. The White House and Republican lawmakers in Congress are locked in tense negotiations with little sign they were close to a deal that would avoid a default that could unleash chaos in the global financial system.

For the Fed, the prospect of default means uncertainty not just over the debilitating effects it would likely have on the economy, but also for how it handles the nuts and bolts of daily policy implementation: Would money market funds accept an impaired Treasury security as collateral? Would the Fed be willing to borrow or buy a troubled Treasury security?

For their parts, central bank officials from Fed Chair Jerome Powell on down have insisted the only resolution is for the $31.4 trillion debt ceiling to be raised and have demurred on offering specifics for what the Fed might do.

“I’m not going to speculate on what could or possibly can happen … I don’t think that’s useful,” New York Fed President John Williams said last week.

PAST AS PRECEDENT

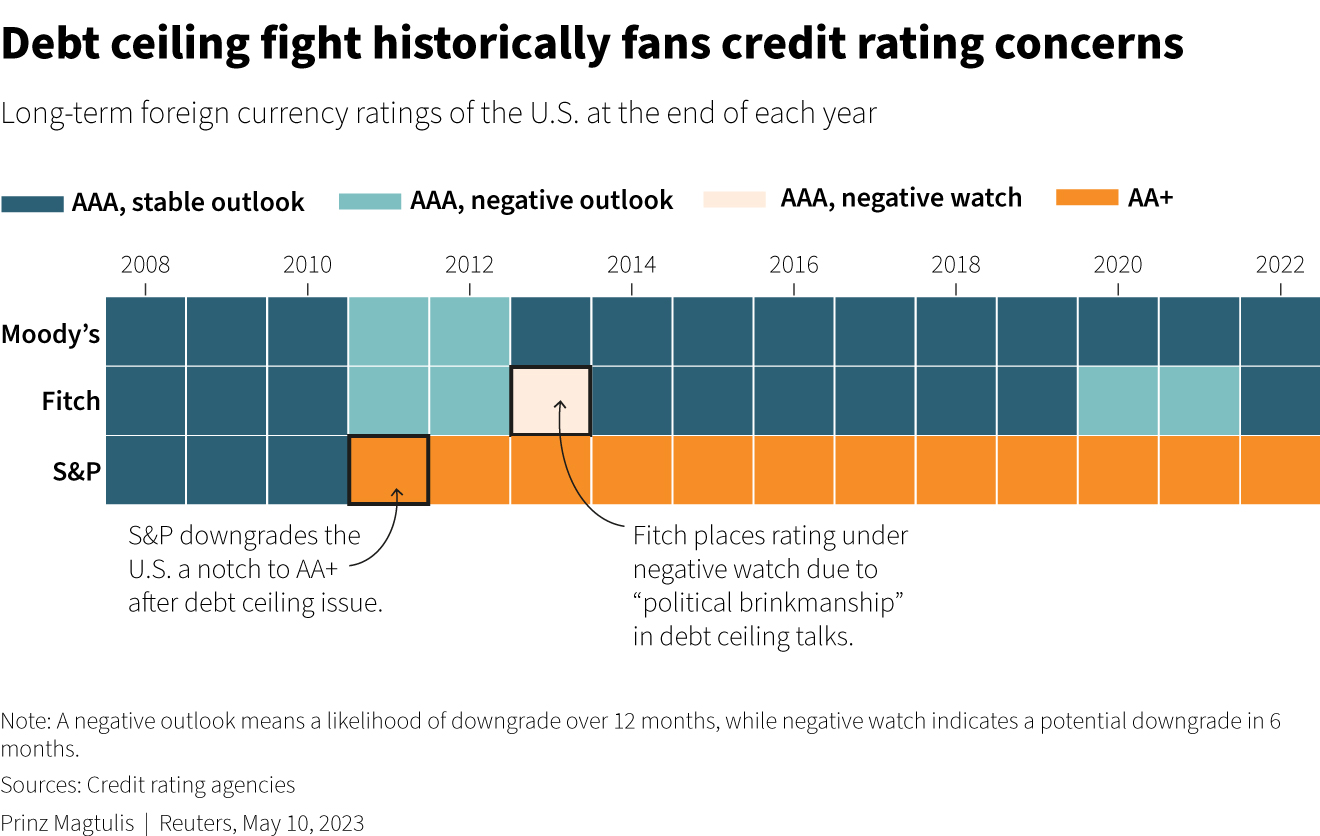

This is not the Fed’s first experience with debt-ceiling brinkmanship. It developed a playbook in previous stand-offs in 2011 and 2013 that would likely form the basis for responding should this episode end in default as opposed to a deal to avert it, as in the past.

The minutes from the Fed’s October 2013 meeting said officials expected they needed no change in procedures and would deal with securities at market prices, while leaving some space to intervene to stabilize markets if needed.

There are also some differences now that give the Fed some space, at least in terms of how its market operations might function, in no small part due to its massive balance sheet. The Fed currently owns about $5.2 trillion in Treasury debt, and the bulk of it would be fine at the start of a default.

“Even if there are defaults, let’s say in July or June or something like that, there’s more than enough collateral that is not defaulted upon” that the Fed would still be able to transact with money market funds to keep its overnight reverse repo facility functioning, said Joseph Wang, chief investment officer at Monetary Macro.

He added that he would expect money market funds to accept impaired Treasuries if needed because ultimately these firms are lending to the Fed anyway, and there’s little chance they won’t get their money back.

Wang also expects that the U.S. central bank would accept impaired Treasuries as part of its Standing Repo Facility as well as any discretionary operations it might undertake because not doing so might be a bigger problem. “It would seem strange for the Fed to want to cause problems itself, as they have financial stability as part of their mandate,” he said.

Still, pricing securities could be a major issue and one that could grow bigger the longer any default persists.

Derek Tang, an analyst at forecasting firm LH Meyer, said the Fed has likely been vague on contingencies because it wants elected leaders to resolve the problem and not see the central bank as a safety valve.

And that’s where pricing an impaired Treasury for Fed operations gets tricky. Determining a market price may be hard, but if the central bank decided to take in such a bond at a higher price than what the market offers, it could be seen as the Fed becoming “an enabler of this drama,” Tang said.

Beyond how to keep the wheels of monetary policy spinning, other issues the central bank might have to contend with are whether to intervene with bond purchases to stabilize markets, as it did in March 2020 when the COVID-19 pandemic struck. Some Fed officials have spoken in recent months about having this power standing separate from asset buying aimed at stimulating the economy.

Reporting by Michael S. Derby; Editing by Paul Simao

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}