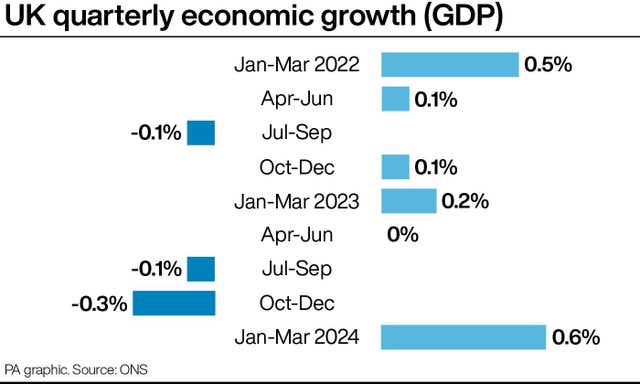

The UK economy rebounded out of recession with faster-than-expected growth over the first quarter of 2024, according to official figures.

The Office for National Statistics said gross domestic product (GDP) is estimated to have risen by 0.6% between January and March.

It comes after two quarters of decline – which represents a technical recession – in the back half of 2023.

A consensus of economists had predicted a 0.4% improvement for the latest quarter.

ONS director of economic statistics Liz McKeown said: “After two quarters of contraction, the UK economy returned to positive growth in the first three months of this year.

“There was broad-based strength across the service industries with retail, public transport and haulage, and health all performing well.

“Car manufacturers also had a good quarter. These were only a little offset by another weak quarter for construction.”

It represented the strongest quarterly growth since the fourth quarter of 2021.

The performance was particularly driven by improvements in the services and production sectors, which grew by 0.7% and 0.8% respectively.

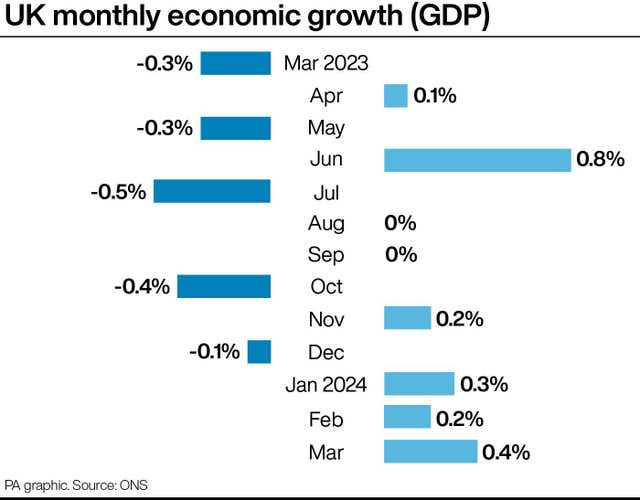

On Friday, the ONS confirmed the quarterly performance after 0.4% economic growth in March, again boosted by the UK’s service industry.

There was notable growth for the human health and social services sector, administrative and support services, as well as for wholesale and retail firms.

Construction output, however, fell during the month, but its 0.4% drop represented a significant reduction in decline after a 2% fall in February.

Ben Jones, lead economist at the CBI (Confederation of British Industry), said the data suggests the UK is “now on the road to recovery”.

He added: “With falling inflation boosting households’ spending power, as well as opening the way for a reduction in interest rates in the months ahead, the economy should be able to sustain some momentum through the year.

“But a consumer-led recovery could prove short-lived without more determined action to tackle the long-standing problem of weak productivity growth, which ultimately sets the UK’s economic speed limit.”

Meanwhile, George Dibb, head of IPPR’s centre for economic justice, stressed it is “too early to say that the British economy has turned a corner” despite the rise in GDP.

“Today’s stats are broadly good news, with positive GDP growth above expectations,” he said.

“But we’ll need to repeat the trick and get many quarters of growth like this for this to feel like a sustained recovery for many people.

“The data show salaries growing but real wages are coming up on a two-decade squeeze, while higher prices for housing and on the weekly shop remain a concern for many households, and we still had the second-lowest growth in the G7 in 2023.”

It came a day after the Bank of England’s monetary policy committee held interest rates at 5.25% and slightly upgraded its forecast for UK economic growth.

In its latest Monetary Policy Report, it said GDP will increase 0.5% this year and 1% in 2025, both 0.25 percentage points higher than the last estimates published in February.

Chancellor Jeremy Hunt said: “There is no doubt it has been a difficult few years, but today’s growth figures are proof that the economy is returning to full health for the first time since the pandemic.

“We’re growing this year and have the best outlook among European G7 countries over the next six years, with wages growing faster than inflation.”

The economy has turned a corner. Today’s news proves that.

We know things are still tough for many people, but the plan is working, and we must stick to it.

— Rishi Sunak (@RishiSunak) May 10, 2024

Labour’s shadow chancellor Rachel Reeves said: “This is no time for Conservative ministers to be doing a victory lap and telling the British people that they have never had it so good.

“The economy is still £300 smaller per person than when Rishi Sunak became Prime Minister.”

{kind=link}