In 2022, almost half of American households had no savings in retirement accounts, according to the Survey of Consumer Finances (SCF). These accounts include individual retirement accounts; Keogh accounts; certain employer-sponsored accounts, such as 401(k), 403(b), thrift savings accounts; and pensions.

Personal saving has grown more important as employers have shifted away from defined benefit plans, or pensions, putting more of the responsibility on workers to plan for retirement. In 1989, half of working households ages 50 to 60 had a defined benefit plan. In 2022, only a quarter did.

How much do people save for retirement?

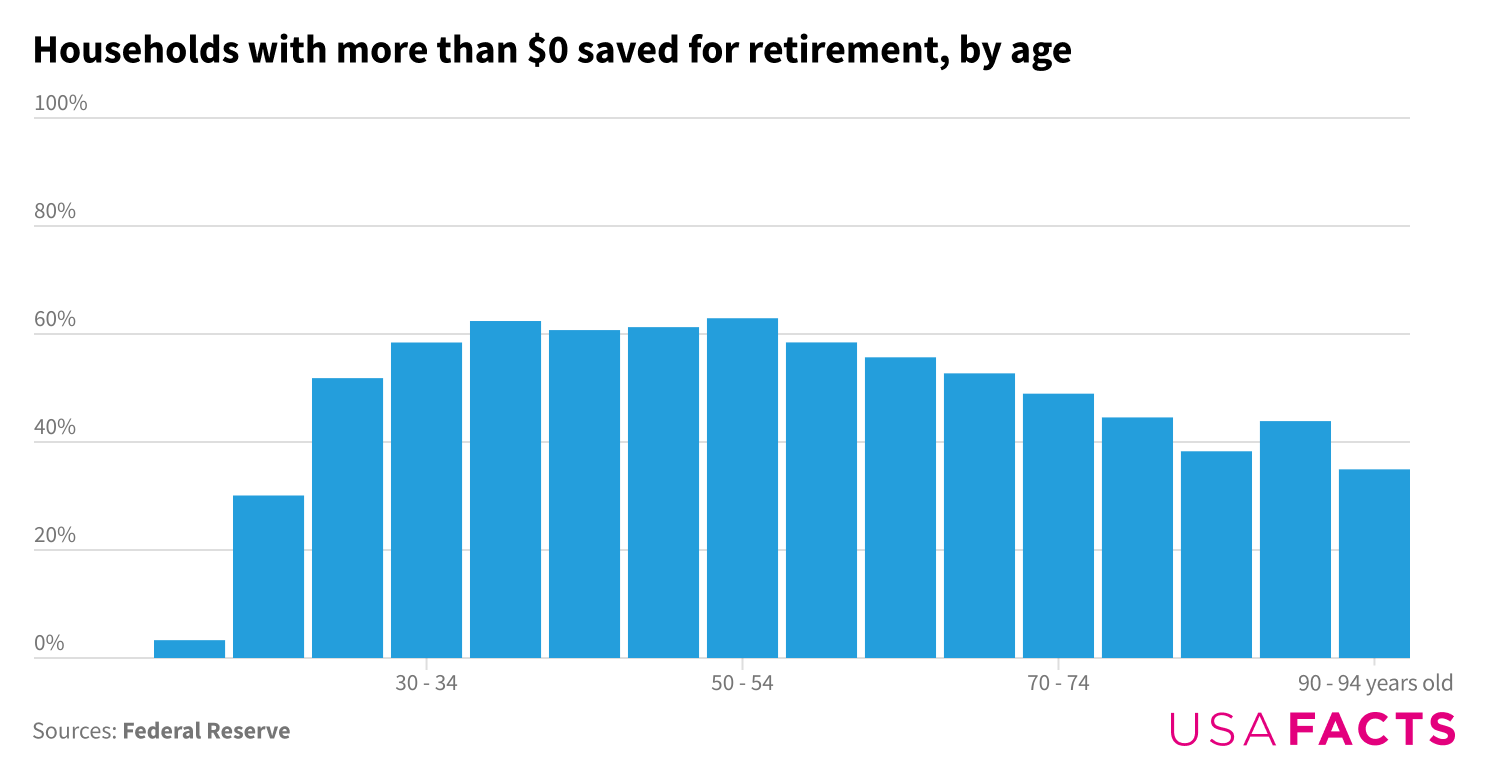

In 2022, about 46% of households reported any savings in retirement accounts. Twenty-six percent had saved more than $100,000, and 9% had more than $500,000.

These percentages were only somewhat higher for older people. Those ages 50 to 54 were the most likely to have a retirement account. About 63% in this age group had any savings, and 35% had saved more than $100,000.

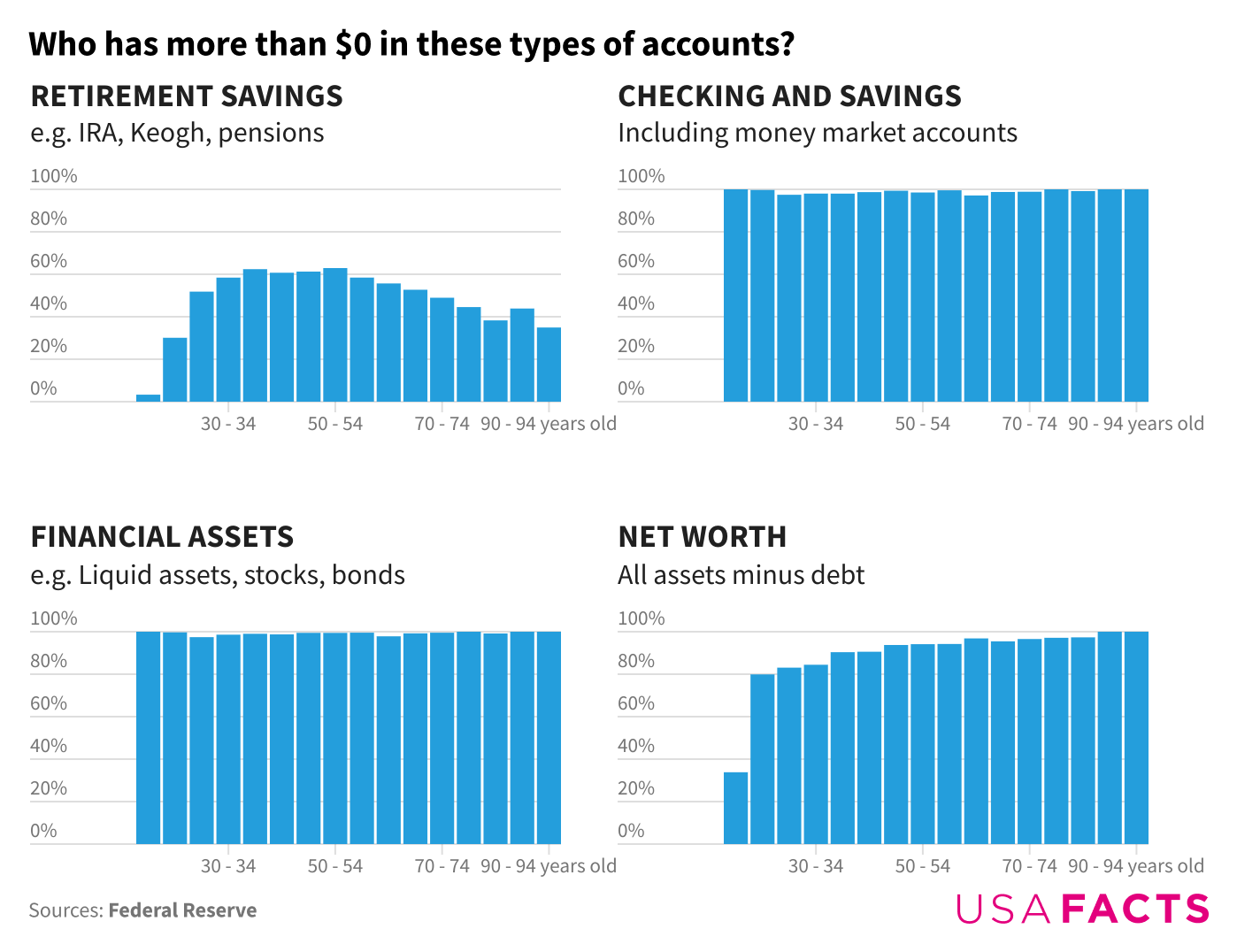

Retirement savings accounts are not the only place that people could store money for retirement. Is it possible that people are primarily saving their money elsewhere?

e.g. IRA, Keogh, pensions

Including money market accounts

e.g. Liquid assets, stocks, bonds

Most American households have at least $1,000 in checking or savings accounts. But only about 12% have more than $100,000 in checking and savings. About 45 percent of the households nearing retirement age have that amount of financial assets, including checking and savings accounts,retirement accounts, stocks, bonds, and certificates of deposit.

Higher percentages of households have a net worth of at least $100,000, especially as they grow older. Net worth includes non-liquid assets, such as a vehicle or house, that would have to be sold to provide income.

Even including these assets, many Americans appear to be set up to depend heavily on Social Security benefits after they stop working. Workers currently younger than 63 are eligible for full Social Security retirement benefits at 67. The average yearly Social Security benefit is currently about $22,000.

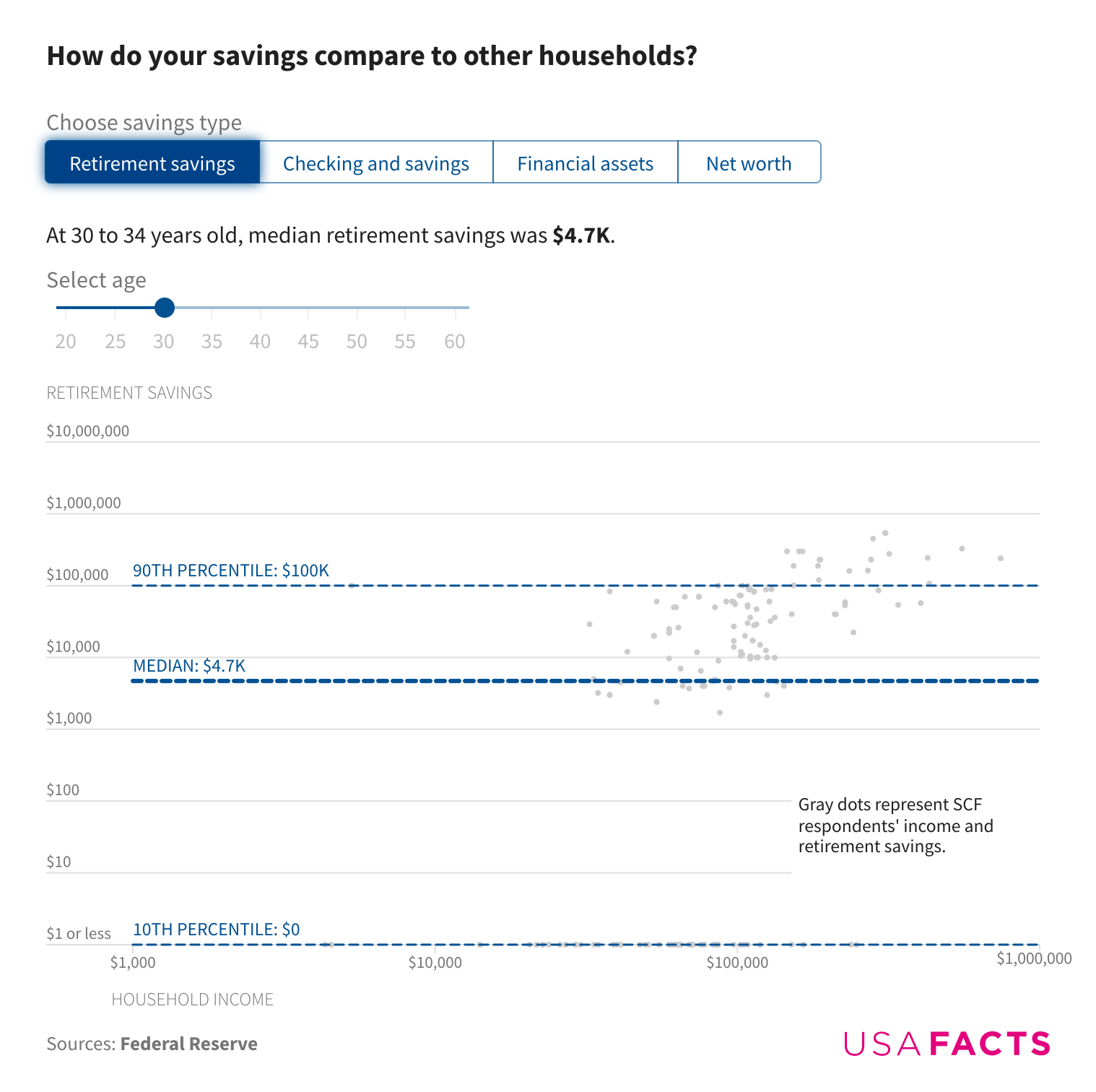

How do your retirement savings compare to others?

Households with higher incomes have more saved no matter what is counted as retirement savings.

At 30 to 34 years old, median retirement savings was

$4.7K.

The median household between the ages of 30 and 34 had $4,700 in dedicated retirement accounts, $7,000 in checking and savings accounts, $20,100 in financial assets, and a net worth of $89,800. (In the surveys, the age of the household reflects the male’s age in mixed sex couples and the older individual in same-sex couples.)

At ages 55 to 59, the median household had $24,500 in retirement accounts, $7,900 in checking and savings accounts, $76,000 in financial assets, and a net worth of $320,700.

Read more about the net worth for different types of families, the wait time for Social Security disability benefits, and get the facts every week by signing up for our newsletter.

{kind=link}