A trader works on the floor of the New York Stock Exchange shortly before the closing bell as the market takes a significant dip in New York, U.S., February 25, 2020. REUTERS/Lucas Jackson/File Photo Acquire Licensing Rights

A look at the day ahead in U.S. and global markets from Mike Dolan

The mercurial world of artificial intelligence continues to grab most market headlines into the U.S. Thanksgiving holiday, while a temporary ceasefire in Gaza helped subdue already subsiding volatility gauges even further.

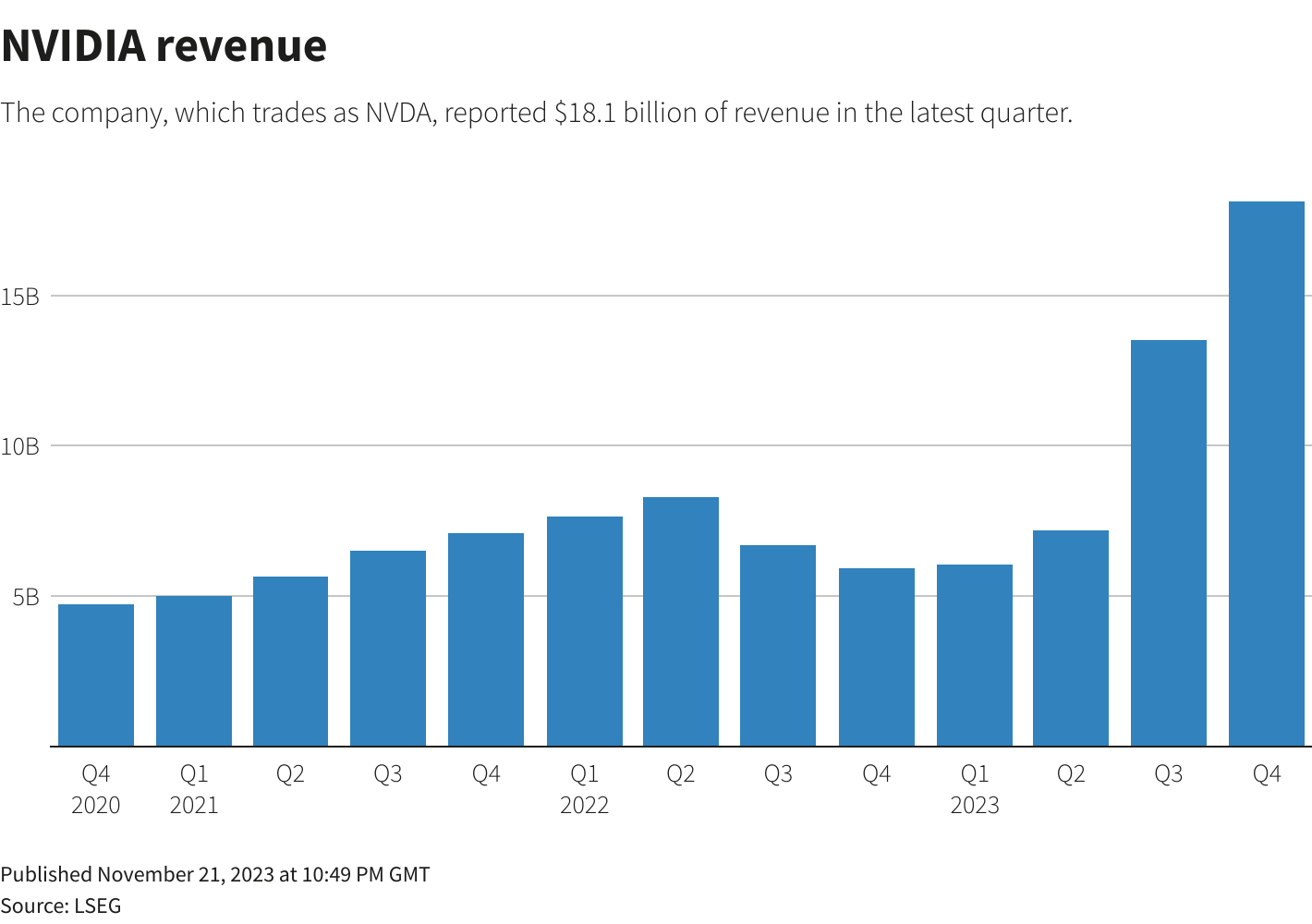

While many investors have been thrall to the AI boom all year, the 240% year-to-date surge in Nvidia (NVDA.O) has stolen the show as AI excitement sent demand for its high-end chips soaring.

Remarkably, Nvidia managed to vault the sky-high bar for quarterly earnings, revenue and projections yet again in its latest update overnight.

But the sheer scale of its share price gain this year makes this market a tough crowd to please and its stock ticked back less than half a percent lower in out-of-hours trade.

The firm insisted a retreat in China would be made up by demand from elsewhere and the numbers continue to be eye-popping. It forecast current-quarter revenue of $20 billion, plus or minus 2% – well above analysts’ consensus estimate of $17.86 billion.

The boardroom rollercoaster at ChatGPT-developer OpenAI, meantime, continued to hog front pages – even if it was in danger of turning into high farce. Sam Altman is now set to return as CEO just days after his ouster, capping frenzied discussions about the future of the startup at the center of the AI craze.

The darker reaches of the tech world were also unnerving as Binance chief Changpeng Zhao stepped down and pleaded guilty to breaking U.S. anti-money laundering laws as part of a $4.3 billion settlement resolving a years-long probe into the world’s largest crypto exchange.

But for all the frenetic newsflow, markets appear to have settled into holiday mode. Wall St stocks (.SPX) ended marginally in the red on Tuesday and futures held steady overnight.

Most remarkable running into yearend has been the dissipation of implied volatility, with the VIX (.VIX)‘fear index’ dropping to 13 – its lowest since mid September. Bond volatility (.MOVE) has also fallen to two-month lows, while currency market ‘vol’ (.DBCVIX) is plumbing 20-month lows.

With Nvidia the last mega cap to report in the Q3 earnings season, scorecards show the aggregate annual profit growth through the quarter running at more than 6% – more than four times consensus forecasts just six weeks ago and with more than 80% of firms beating the Street. Revenue growth of 1.5% is almost twice pre-season consensus.

Treasury yields were also on the backfoot, with the Federal Reserve’s latest meeting minutes offering little new and with the committee blaming October’s bond squeeze largely on a jump in the ‘term premium’ demand by investors anxious about rising debt supply.

However, even the term premia has evaporated again and the New York Fed’s gauge has slipped back into negative territory after resurfacing for just two months.

CONCERN OVER HOME SALES, HOLIDAY SEASON SALES

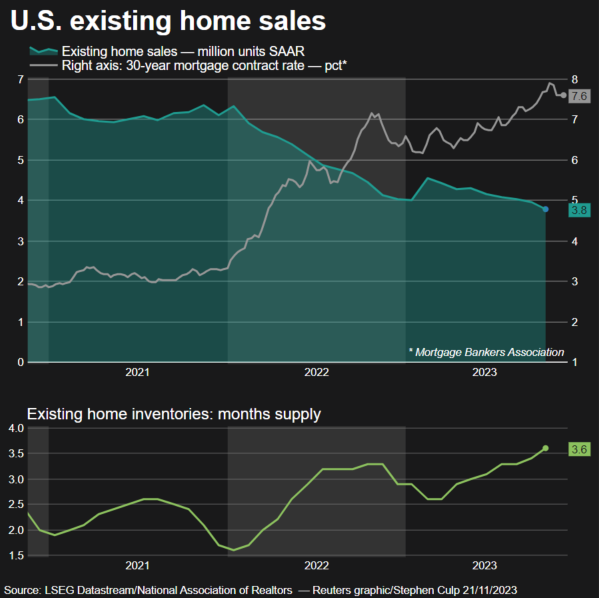

News of a drop in U.S. existing home sales last month to a 13-year low was perhaps as important as the Fed minutes – as was warnings from more major U.S. retailers, this time Best Buy and Nordstrom, about sticky holiday season sales and the need for discounting.

Even though crude oil prices have backed up lately ahead of the weekend OPEC meeting, there was continued good news for U.S. consumers at the pump – with average retail gasoline prices falling to their lowest level since January.

The dollar (.DXY) was a touch higher on Wednesday, meantime, with most overseas stock markets firmer too.

British stocks were higher ahead of UK finance minister Jeremy Hunt’s latest Autumn budget, where speculation of household and business tax cuts is rife.

Chinese stocks (.CSI300) underperformed again despite signs of more economic stimulus locally. Chinese government advisers will recommend economic growth targets for 2024 ranging from 4.5% to 5.5% to an annual policymakers’ meeting as Beijing seeks to create jobs and keep long-term development goals on track.

Key developments that should provide more direction to U.S. markets later on Wednesday:

* U.S. Oct durable goods, weekly jobless claims, University of Michigan final Nov sentiment survey. Eurozone Nov consumer confidence

* Bank of Canada Governor Tiff Macklem speaks

* British finance minister Jeremy Hunt makes his Autumn Statement budget speech

* Dutch parliamentary elections

* U.S. Treasury auctions 4-week bills

* U.S. corporate earnings: Deere, Tremor, Diocal, Jiayin, EHang, GDS, Baozun, Lexinfintech

By Mike Dolan, Editing by Bernadette Baum

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

{kind=link}