Europe is home to a young and dynamic healthtech industry, which, despite the global venture capital (VC) investment contraction, has managed to continue to grow, innovate and secure funding. In the year to come, the sector is expected to see accelerated developments as adoption rises and a new generation of healthtech providers emerge, a new report by Finch Capital, a growth investor focusing on finance, health and real estate technology, says.

The inaugural State of European Healthtech 2022 report, released on December 02, looks at the state of the nascent industry, delving into funding trends, merger and acquisition (M&A) deals, business creation and hiring trends.

According to the report, Europe’s healthtech sector has grown significantly over the past two years amid the COVID-19 pandemic, with total capital invested having risen from US$1.7 billion in 2017 to close to US$10 billion in 2021. Although much of the funding activities have so far been centered around telemedicine, a new generation of healthtech entrepreneurs are starting to enter the sector and giving rise to technology businesses outside of the segment, the report says.

Many of Europe’s most valuable healthtech businesses were started by entrepreneurs with minimal background in health, the report notes. But many younger startups are now catching up, and these are being led by founders with sector experience at healthtech unicorns. One example shared in the report is Alan, a French healthcare app and insurance provider, and Vitaance, a Spanish company specializing in life and disability insurance for businesses.

Alan was founded in 2016 by Jean-Charles Samuelian-Werve, an entrepreneur with a background in engineering, and Charles Gorintin, a data scientist who has worked for names like Twitter, Instagram and Facebook.

The company, which claims 300,000 customers, is an insurtech unicorn valued at US$2.85 billion that provides a digital insurance service, offering simple and seamless insurance coverage with reimbursements, easy claim handling and gives users access to medical professionals, both through in-person appointments and by video calls.

Vitaance, which was founded just last year, is headed by co-founder and CEO Ana Zamora, and co-founder and CPO Bernard Granados. Prior to launching Vitaance, Zamora was the ops and insurance lead of Alan. She also served as an executive at asset management company Mercer, leading the firm’s Elect offering, a suite of benefits and insurance products for employees of small and medium-sized enterprises (SMEs). Bernard Granados, on the other hand, is an entrepreneur and business executive with experience in insurtech, marketing technology, edtech and e-commerce.

Other companies founded by Alan alumni include Fraction, Revyze and Logbook, the report notes. In total, these startups have secured a total US$5 million in funding.

Healthtech funding and hiring trends in Europe

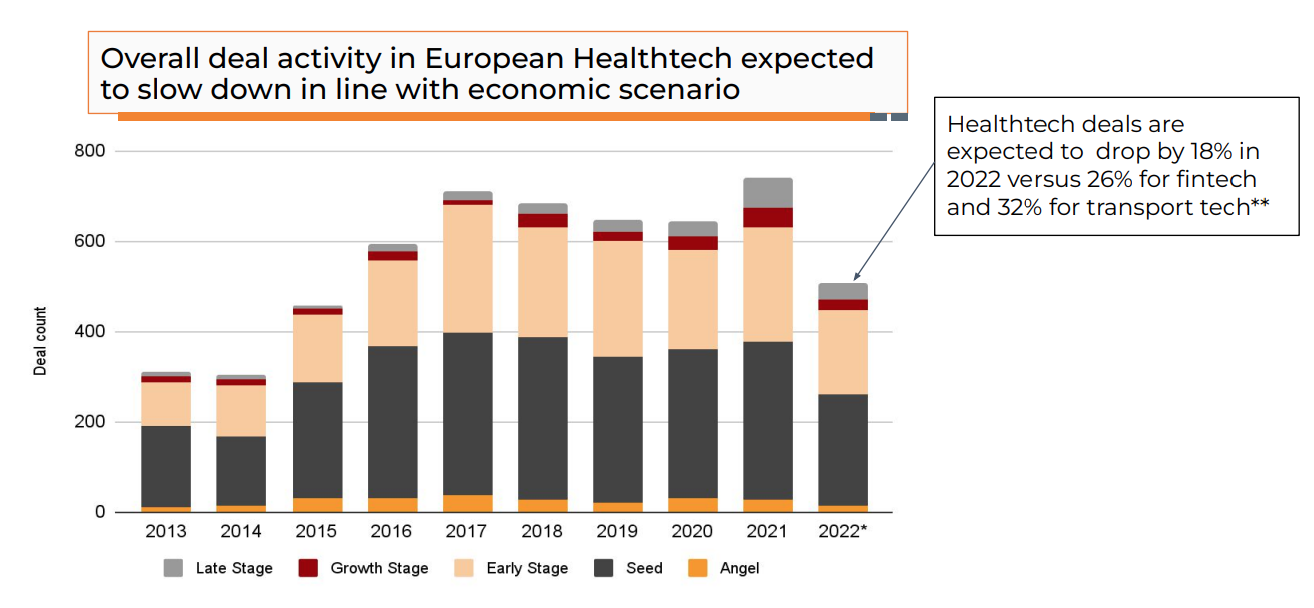

European healthtech startups are projected to secure a total of US$5 billion this year, down 50% from 2021’s record but still up by a significant 38% from 2020 levels. Healthtech deal count, meanwhile, is expected to drop by just 18% in 2022, against 26% for fintech and 32% for transport tech, indicating that funding activity in the sector is performing better than other tech verticals.

Overall deal activity in European healthtech startups, Source: State of European Healthtech 2022, Finch Capital, Dec 2022

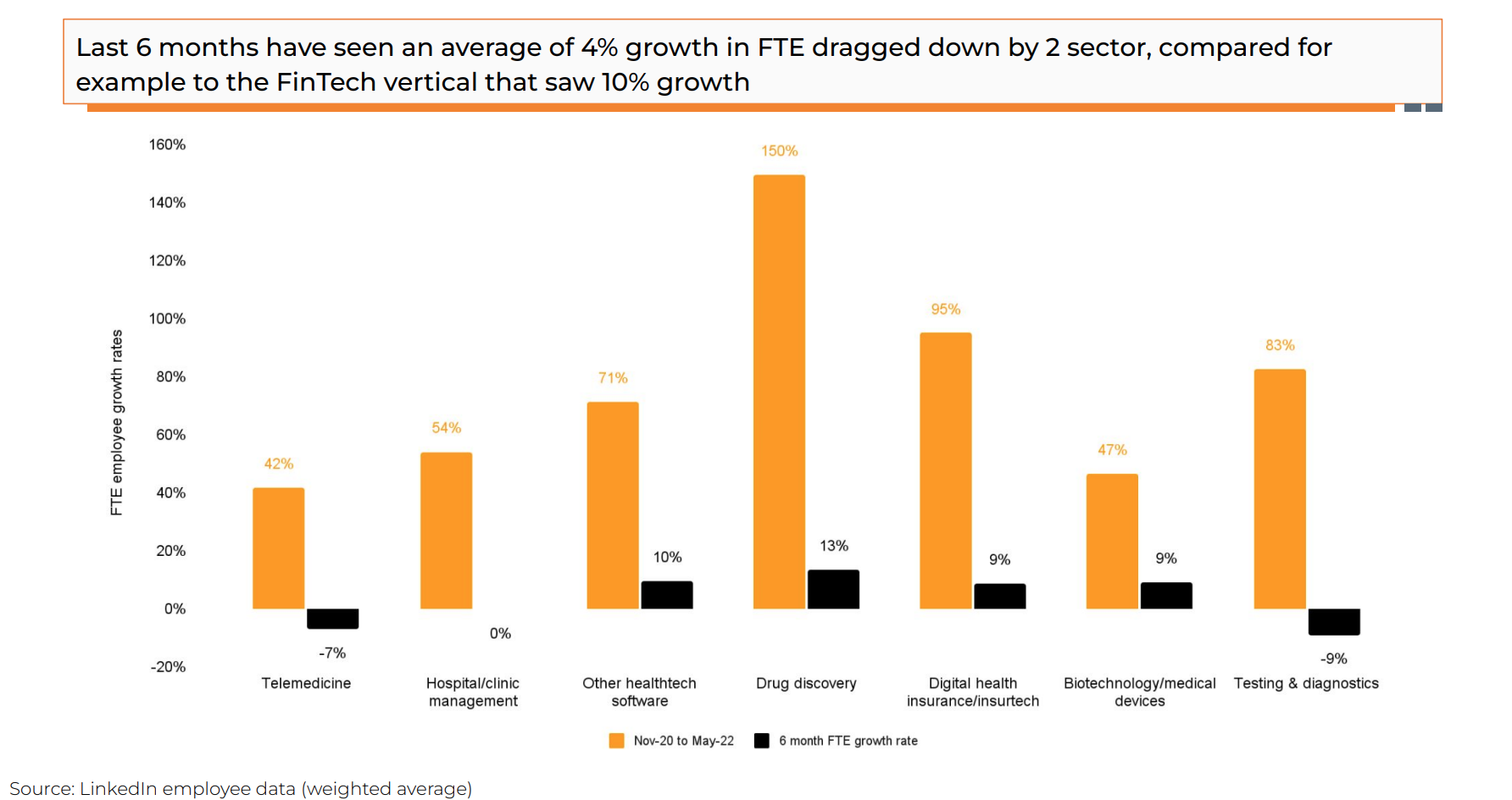

In 2022, telemedicine continued to be the largest healthtech segment, securing about EUR 1.5 billion in funding, as of October 30. Biotechnology/drug development took the second position, followed by hospital/clinical management and testing and diagnostics.

Despite retaining the top spot in healthtech funding, investment in telemedicine startups is starting to contract, the report notes, a retreat that’s further evidenced by a significant slowdown in hiring in the sector.

While companies in software and biotechnology/drug development have continued to actively hire this year, recording a 10% and 13% growth rate in full-time equivalent (FTE) roles over the past six months, telemedicine startups, on the other hand, have seen a 7% decrease, an indication that the segment is being affected by layoffs this year.

Full-time equivalent employee growth rates across healthtech segments in Europe, Source: State of European Healthtech 2022, Finch Capital, Dec 2022

This retreat from telemedicine has started to give rise to software, as evidenced by the momentum the segment is seeing and continued hiring trends observed among business-to-business (B2B) companies within segments including hospital/clinic management and insurtech.

Moving forward, growth in the software segment will be further driven by rising demand from insurers and other healthcare IT providers for technology solutions, Finch Capital predicts, a growth that’s expected to help the overall European healthtech funding market to bounce back next year.

Featured image credit: Freepik

{kind=link}