As our latest leveraged finance report reveals, European leveraged finance markets saw significant inertia through the course of 2022 as high inflation, rising interest rates and cooling M&A activity put the brakes on leveraged loan and high yield bond issuance. Those same headwinds continue to challenge the market in 2023.

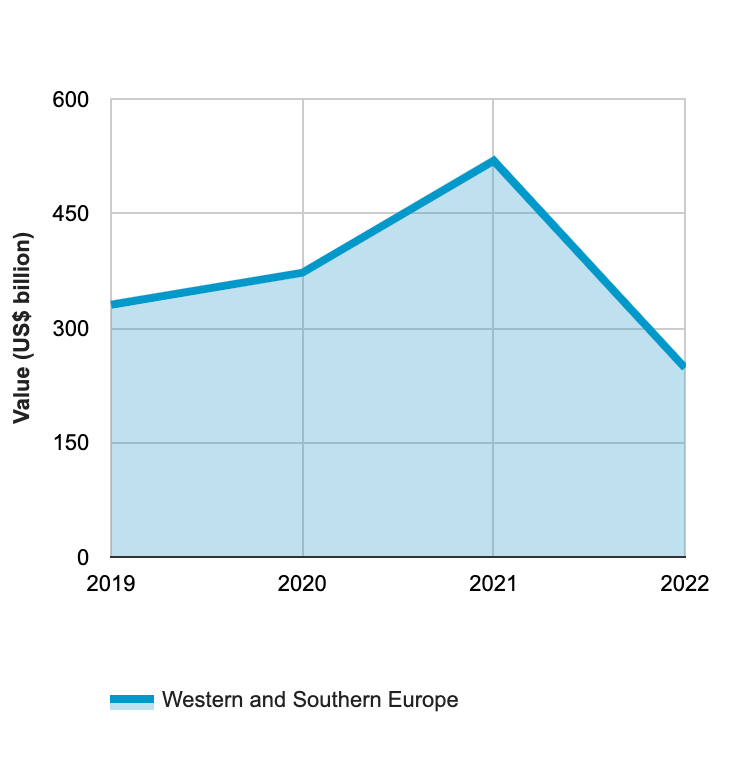

Leveraged loan issuance in Western and Southern Europe fell from US$343.3 billion in 2021 to US$193.9 billion in 2022, and high yield bond markets endured similar slowdowns, with issuance down from US$175.9 billion in 2021 to US$53.9 billion in 2022.

Overall Issuance by value 2019 – 2022

Instrument type: High yield bonds and Leveraged loans Use of proceeds: All

Location: Western and Southern Europe Sectors: All Sectors

The steep decline in activity came as the conflict in Ukraine dampened investor appetite for risk and central banks bumped up interest rates to keep a lid on surging inflation. This, coupled with political volatility (including multiple UK prime ministers in succession and the ongoing impact of Brexit) meant that markets had little positive momentum to rely on as they adjusted their risk assessment due to the changing circumstances.

The recent collapse of start-up focused lender Silicon Valley Bank and the rescue deal for Credit Suisse by UBS have put liquidity and the global banking system under additional pressure. Regulators and central banks around the world have stepped in to prevent contagion, but the markets have been on edge and worried that other banks could be vulnerable to the impact of rising rates on capital structures. As a result, lender appetite to underwrite new financings may remain limited.

Rate rises and higher borrowing costs

In the UK, inflation climbed to a four-decade high in 2022, prompting the Bank of England (BoE) to raise interest rates to 3% in November and 3.5% in December—the highest levels since 2008. This continued in 2023, with the BoE’s latest increase taking the rate up to 4.25% in March.

The European Central Bank (ECB) also raised rates to the highest level in more than a decade by the end of 2022, with a 0.5% increase announced in December to tackle inflation that was running above 9%. Even as eurozone inflation dipped to 8.6% in January 2023, the ECB announced another 50-basis point interest rate increase in February, taking its key rate to 2.5%.

As interest rates have climbed, so have borrowing costs. The average margins on first-lien institutional loans were sitting at 4.29% at the end of 2021, but spiked to 4.75% by the end of Q4 2022 according to Debtwire Par. European high yield bond borrowing costs almost doubled between the end of 2021 and Q4 2022.

Loan financing costs continued to tick higher in 2023, with average margins on first-lien institutional loans coming in at 4.92% at the end of February. The average yields to maturity on senior secured and senior unsecured bonds have declined since Q4 2022, to 7% and 6.25% respectively by the end of February 2023, but remain well above the levels observed in Q1 2022.

Rising borrowing costs and a recalibration of risk appetite from lenders and investors had a chilling impact on refinancing activity, which was a major driver of activity at the end of 2020 and through 2021. High yield refinancing deals dropped from US$100.8 billion in 2021 to just US$21.2 billion for 2022. Loan refinancing fell from US$122.1 billion to US$77.1 billion during the same period.

As abundant liquidity and low debt costs have dried up, and with many maturities already addressed, there has been limited chances for opportunistic borrowers to refinance existing credits on better terms and extend maturities.

Bargain buys in secondary markets

For lenders and investors, the deep discounts to par that have emerged in the secondary market have blunted the appeal of backing refinancings. According to Debtwire Par, European leveraged loans were priced at an 11% discount to par in secondary markets in September and October, encouraging investors to pick up bargain secondary market trades rather than support refinancings.

New money deals, meanwhile, have also declined due to discounts in the secondary market. To gain any kind of traction for new deals, borrowers have been forced to accept significantly deeper original issue discounts (OID). This has prompted borrowers to put financings on ice until market conditions improve—and investors still seem inclined to wait for secondary market opportunities even when deep OIDs are offered.

These factors saw new money leveraged loan issuance in Western and Southern Europe fall from US$176.4 billion in 2021 to US$111 billion, while high yield new money transactions fell from US$70.8 billion to US$32.5 billion in 2022.

Falling M&A and buyout transaction flow in Western Europe—down 30% year-on-year by the end of 2022—has also knocked new money activity. In loan markets, combined M&A and buyout issuance dropped from US$143.6 billion in 2021 to US$82 billion last year, with high yield issuance for combined M&A and buyouts sliding from US$39.3 billion to US$11.6 billion during the same period.

Adjusting to the new normal

Moving into 2023, leveraged loan and high yield activity is likely to continue facing headwinds. It is uncertain when European inflation will peak and interest rates will top out. Lenders and investors will remain cautious while issuers will avoid coming to market unless strictly necessary.

Smaller deals and add-on deal financings—for example, UK online retailer THG’s £156 million add-on term loan B—will still find a way through loan markets, while high yield markets will open intermittently and facilitate some issuance, as seen with deals such as Hunkemoeller, Fedrigoni, EnQuest and Cirsa, which managed to secure financing in the final quarter of 2022.

Overall, the European market will remain challenging, although there have been some early movers in 2023 with deals successfully hitting the market in January, including Limacorporate and Verisure. Other highlights in Q1 2023 include a financing deal for Aggreko’s purchase of Resolute Industrial and deals in the pipeline include a €2.9 billion institutional loan to finance Advent International’s acquisition of DSM Engineering, according to Debtwire Par. Bond markets were also active—for example, Debtwire Par reports that Telecom Italia and ZF Friedrichshafen were both able to proceed with bond issues.

Despite this activity, some borrowers may have to scale back their expectations when coming to market. Dutch artificial turf manufacturer TenCate Grass, for example, postponed a €274.3 million add-on to its €315 million EURIBOR+ 500 bps term loan B due September 2028 because of the volatile market conditions.

Borrowers are also running dual-track financing processes more often, with direct lenders picking up an increasing volume of transactions that would otherwise have gone down the high yield bond or leveraged loan route. Italian specialty food ingredients producer Irca, for example, shifted the financing for its acquisition by Advent International from The Carlyle Group and from a proposed €430 million high yield bond note to a direct lending package provided by CVC Credit.

Maturity extensions front and center

Maturities are being dealt with in creative ways. Typically, both borrowers and lenders are working to avoid restructuring where possible. This is driving an increase in amend-and-extend deals in the loan market and exchange offers in the high yield bond space, as seen in the exchange offer undertaken by German pharmaceutical company STADA, subsequently followed by NewDay and other high yield issuers.

Borrowers are negotiating deals to extend maturity walls by offering incumbent lenders higher coupons, additional covenants and/or additional credit support. Equity injections are also on the radar, as sponsors see the need to support portfolio companies through a rough patch and to convince investors of the long-term value in a business.

The scope for maturity extensions could be limited for certain CLO investors, as their weighted average life tests restrict their ability to roll debt. But when maturity extensions are an option, it is hoped that these arrangements will help avoid large-scale insolvencies and full-blown restructurings in 2023. Lenders should be open to accepting more favorable pricing and terms in exchange for maturity extensions rather than crystallizing losses.

[View source.]

{kind=link}