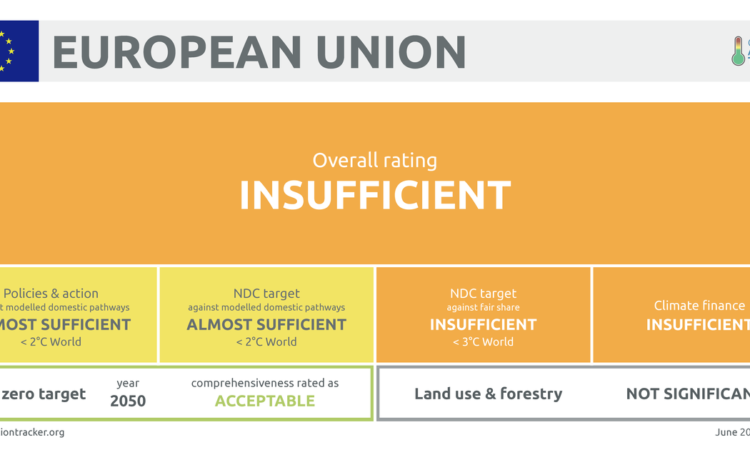

We rate the EU’s policies and action as “Almost sufficient”. The upper bound of our policies and action emissions projection range is based on policies reported by member states as of March 2022, which would result in an emissions reduction of around 35% (excl. LULUCF) below 1990 by 2030. The bottom end of the range is based on policies adopted at the EU level, including the stronger binding renewable energy (42.5%) and energy efficiency targets, which would result in reducing emissions by 55% (excl. LULUCF). If the enhanced LULUCF sink is taken into consideration, net emissions in the EU would decrease by 60%, taking the EU beyond its emissions reduction target of “at least 55%”. Consideration of the indicative renewable energy target (of a further 2.5%) for 2030 reduces emissions even further to 57% (excl. LULUCF) and 61% (incl. LULUCF).

In late 2022 and early 2023, the EU amended its key climate regulations, adopting stronger targets including:

- Increasing the EU Emissions Trading Scheme (EU ETS) emissions reduction target from 43% to 62% below 2005 levels by 2030.

- Increasing the emissions reduction target in the Effort Sharing Regulation from 30% to 40% below 2005 levels by 2030.

- Strengthening its renewable energy target from a 32% share [of total energy] to 42.5% by 2030, with an additional 2.5% “indicative” target.

- Cutting its final energy demand from 846 Mtoe to 763 Mtoe in 2030.

- Expanding the size of its land sector sink target from 225 MtCO2e to 310 MtCO2e.

From 2027 onwards, a parallel scheme will be established under the EU ETS to cover buildings and transport.

Member states still need to adopt policies implementing these targets. In their National Energy and Climate Plans (NECPs), they have to propose their national targets for the share of renewable energy and energy consumption that would result in at least the targets agreed in the respective directive for the EU as a whole. Drafts of these plans are to be submitted by the end of June 2023.

Along with the major policy changes, the EU has also simplified permitting procedures for investments in renewable energy, batteries, and electricity grid development. While the impact of these measures will only be visible in the coming years, already in 2022 investment in renewables increased significantly, especially for solar energy and heat pumps. However, while the installed capacity in wind energy – both offshore and onshore – has also increased, a significant drop in new investments indicates a temporary slowdown in the sector. As a result of the accelerated deployment of renewable energy and energy savings, driven to a large degree by high energy prices, the expected return to coal, especially during the winter 2022/2023, did not materialise.

In the case of the majority of low-carbon technologies, especially solar panels, wind turbines, and batteries, the EU is to a large degree dependent on imports from other countries. This has the potential to exacerbate bottlenecks if trade flows are interrupted. To mitigate this challenge, the Commission proposed the Net Zero Industry Act in March 2023, which sets the goal of covering at least 40% of selected low carbon technologies with domestic manufacturing. This is a step in the right direction as it will increase the supply of products necessary to meet EU’s emissions reduction goals and decrease their costs due to economies of scale.

NOTE: We have modified our data projections for the EU to reflect policy developments, essentially incorporating what our November 2022 update showed as planned policies, which have since been adopted. We have not updated our historical emissions to reflect the latest inventory data. We will update our projections for the EU fully later this year after the publication of the “Trends and Projections” by the European Environment Agency in Q4 of 2023.

The full policies and action analysis can be found here.

{kind=link}