Britain avoided a much-tipped recession at the end of last year. Phew.

“However, we are not out of the woods yet,” warned Chancellor Jeremy Hunt after last Friday’s GDP figures from the ONS revealed the economy stagnated at the end of 2022, meaning it narrowly avoided the technical recession definition of two consecutive quarters of contraction.

The Chancellor is right to be cautious, especially when the UK is set in contrast to its peers.

New forecasts out from the European Commission this week projected the bloc’s economy is poised to avoid a slump this year, with EU-wide growth coming in at 0.8 per cent.

The Republic of Ireland will grow just under five per cent, powering the area’s output away from a reversal.

Our friends across the pond in the US are looking increasingly likely to avoid a recession after their economy added an unexpected 517,000 jobs last month, despite the US Federal Reserve’s best efforts to choke demand.

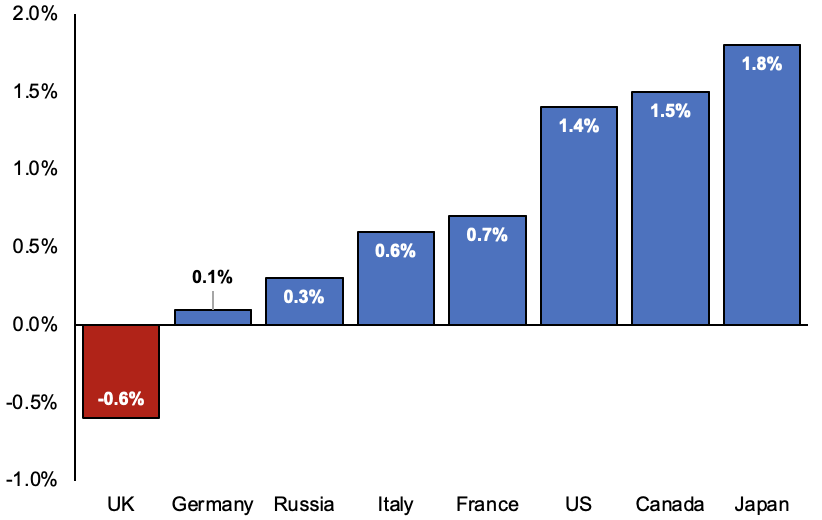

We, on the other hand, have been told to expect to shrink 0.6 per cent this year by the International Monetary Fund (IMF), making us the only rich country to finish 2023 with a smaller economy. Even Russia is forecast to grow.

It should be said the IMF routinely bungle their projections.

So just why is the UK on track to stumble behind the rich world?

Britain will be the economic sloth of 2023 (according to the IMF)

Steeper energy bills

Inflation has been the main factor kneecapping the world’s top economies.

Households and businesses are being squeezed by rising costs, forcing them to cut spending, weighing down economic growth.

This rise in inflation, especially in Europe and initially in the US, has been driven by “stratospheric increases in [gas] prices,” Philip Shaw, economist at Investec, told City A.M.

That jump has pretty much entirely unwound now, but the damage has already been done to family and corporate balance sheets in Britain and Europe (less so in America).

The UK’s dependance on gas to power homes engineered “a bigger impact on consumers and businesses here than elsewhere,” Shaw added.

The impact of rising gas prices has also hit the UK harder as Chancellor Jeremy Hunt has offered “less generous” support than his European counterparts, Dean Turner, chief eurozone and UK economist at UBS Wealth Management, told City A.M.

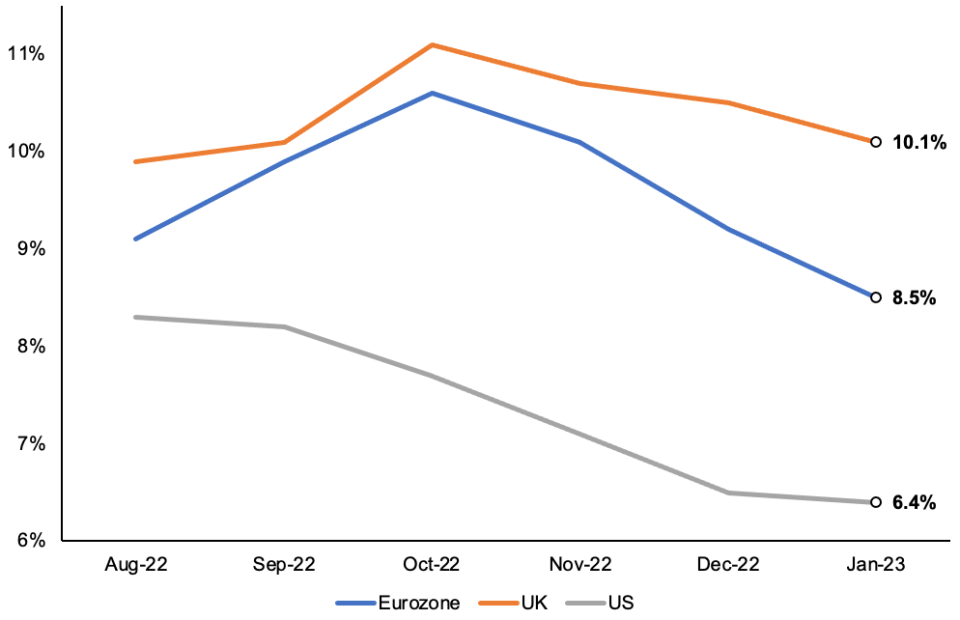

UK inflation has outpaced US and Europe

France’s state owned energy giant EDF was forced to cap price increases at four per cent for most of 2022, while the German government paid household energy bills in December and launched around £175bn of support.

While Hunt stuck to Liz Truss’s £2,500 price cap, family energy bills have still skyrocketed over the last year or so. The current price cap mechanism also means bills will not begin falling until the summer.

Inflation has definitely turned a corner in Britain, cooling for three straight months now in the UK to 10.1 per cent. But it did outstrip the rate of price increases in Europe and the US for most of 2022, meaning there is set to be a bigger spending drop in the UK as a result of a steeper living standards collapse.

American inflation never hit double digits, though it did in the eurozone, peaking at 10.6 per cent.

No such energy cap was launched in the US, mainly because their inflation surge has been driven by excess spending fuelled by president Biden dishing out cash during the pandemic.

Jobs market weakness

Probably the single biggest area where Britain’s weakness stands out is its slimming workforce.

An outflow of around 500,000 from the workforce since the start of the Covid-19 crisis is peculiar.

No other rich country has suffered this level of desertion. Most have actually seen their labour market expand.

A smaller pool of available workers has prompted firms to hike wages to attract and lure talent, which has boosted domestic inflation.

Staff shortages have also stopped companies from seeing through expansion plans, holding back output.

In the US, the jobs market is racing ahead, exactly the opposite of what Fed chief Jerome Powell wants to happen. While strong worker demand could keep inflation higher for longer, it will prop up spending by leaving incomes unscathed.

Aggressive rate hikes

The Bank of England has tightened policy much more aggressively than the European Central Bank (ECB), but less forcefully than the US Federal Reserve.

Rates have climbed 390 basis points collectively since Bank governor Andrew Bailey and co’s first rise in December 2021, sending borrowing costs to 15-year high of four per cent.

The BoE and Fed are probably going to ease off the brake soon, while the ECB is expected to back around 100 basis points of hikes this year.

A steep rate peak in the UK of, probably, 4.25 per cent is poised to be a clamp on growth this year, the IMF said in its latest forecasts.

In fact, analysts at Goldman Sachs reckon every 100 basis point increase “lowers the level of real GDP by roughly 0.5 per cent,” mainly by raising mortgage rates.

However, a wave of homeowners switching to fixed rate mortgages after the financial crisis has delayed the transmission of higher rates to the real economy.

“Britain has among the lowest percentage of mortgages on variable rates,” James Smith, developed markets economist at Dutch bank ING, told City A.M.

“The bigger issue is corporate borrowing where 70 per cent of SME lending is on floating rates, but I don’t think that’s unique to the UK,” he added.

Return of austerity

Britain’s tax and spending policy has become much more stingy after Hunt sought to shore up investor confidence following Liz Truss’s ill-fated mini budget.

Tax band freezes and levy rises launched in his November £55bn autumn statement – most notably a six percentage point corporation tax rise – are scheduled to land soon.

“The return of austerity [and] less support for the energy crisis… will also play a part” in choking production, Frédérique Carrier, head of investment strategy for RBC Wealth Management in the British Isles, told City A.M.

“Britain’s fiscal metrics look worse than other European countries. The need for the UK government to tighten policy to achieve a sustainable fiscal position in the medium-term is therefore more pressing,” Shaw said.

Hunt’s biggest single support measure has been the £2,500 energy price cap.

At the moment, the cap is on course to jump to £3,000 in April. After the recent collapse in energy costs, the policy now “isn’t smoothing prices, it’s causing the spike,” the Resolution Foundation said this week.

Coming down the line is a brief period where the price cap will be above the amount retailers would charge based on lower wholesale gas prices. To avoid that, Hunt “almost certainly will” delay the cap increase for three months “to give wholesale prices time to feed through,” the Foundation said.

The EU has urged the likes of Germany, France and Italy to roll back support for risk of re-igniting turbulence in the euro debt markets.

“It is unlikely that fiscal policy among our peers stays as easy as it is today… the UK may not look like such an outlier [soon],” Turner added.

Tax rises and spending cuts are working together with the Bank of England’s aggressive rate rises to squeeze the economy.

Hunt’s 15 March budget is unlikely to be a silver bullet to prevent a slump.

{kind=link}