The main (economic) discussion point of the week has been the 12-month rate of UK inflation, which caught many by surprise by increasing slightly from 3.9% in November to 4% in December. This also brought the average inflation rate across the last quarter of 2024 to 4.2%.

This is of course a very minor movement upwards in the grand scheme of things, but the expectation was that the rate of inflation would fall further, rather than the slight uptick that transpired.

Food and non-alcoholic beverages posted the largest contribution to falling inflation, though prices in this category still rose 8% year-on-year – just less so than the 9.2% in the previous month.

But this was more than offset by alcohol and tobacco prices (which rose at a 12-month rate of 12.9%), transport – caused by car repairs, after a significant dip in November, and car hire prices – and ticket prices for cultural events (cinema, theatre and concerts).

One can spend much time delving into the minutiae of relative price movements, but it is worth taking stock of where we are in terms of inflation in different areas of the economy and how the Bank of England might respond to this.

Goods and services have relatively similar weights (53% and 47%, respectively) in the calculation of CPI. And as the chart below shows, the fall in inflation over the past year has mostly been driven by goods. Energy prices in particular have contributed to that – they were 17% down year-on-year in December – but so has decelerating food price inflation. This is illustrated by the fact that core inflation – that is, excluding energy and food – is still running at 5.1%, higher than the headline rate.

Chart: Consumer price index, goods, services and aggregate

Source: ONS

On the services side, meanwhile, the story is one of more persistence. Services inflation is lower than it was during the course of 2023, but is still at a very similar rate to the same period the previous year.

The stickiness of services inflation shows the difficult position that the Bank of England still faces. Inflation has remained stubbornly high in the UK compared with similar economies, and it is clear that there is still a significant level of domestically generated inflation in the system in the service sector.

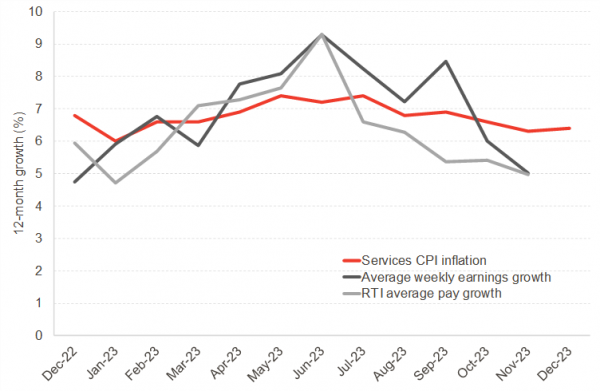

Wages are a much larger determinant of services prices due to their labour intensity. As the chart below shows, services CPI inflation has tracked earnings growth pretty well, although it is smoother – which is to be expected, as firms will not necessarily try to match changes in input costs immediately with price changes.

Chart: Services inflation and measures of pay growth

Source: ONS, HMRC

The Bank of England has recently paused its rate rises as it started to see signs of wage growth cooling, and there has been some speculation that there might be interest rate cuts on the way. Of course it’s hard to know what the Monetary Policy Committee will do for sure – but these data, together with the GDP release earlier in the month, are the main data points that the MPC will have access to when they meet on 1 February.

While average earnings are growing more slowly than earlier in the year, they are still growing quite fast relative to historical levels. This in fact is the issue that has worried the Bank for a while. In many senses, the sharp ness of the increase in inflation in the run-up to the Russian invasion of Ukraine was an external shock of the kind that might not necessitate monetary action.

But the worry about a wage-price spiral convinced MPC members to act, and while the rate hikes have had some effect, it appears they might have yet to fully filter through into labour market conditions. And with potential international trade disruptions on the horizon, further shocks might yet come soon – which could further delay any cuts to Bank Rate. In any case, the Bank seems to be trying to cool any chatter about rate cuts for the time being, despite financial market expectations.

It’s a really fascinating read, which shines a light on how the disability employment gap has evolved over time and why, replicating a study done by DWP last year using data for Scotland.

As with the rest of the UK, the disability employment gap has been closing, and the reasons are similar. Over two thirds of the increase in the employment rate for disabled people since 2014 was due to people already in work becoming disabled.

Disability prevalence has increased significantly, with a large share of this increase relating to an increase in reporting mental health-related disabilities and learning difficulties. Employment rates for disabled people have increased significantly for all types of disability, even those for which prevalence has not significantly changed.

João is Deputy Director and Senior Knowledge Exchange Fellow at the Fraser of Allander Institute. Previously, he was a Senior Fiscal Analyst at the Office for Budget Responsibility, where he led on analysis of long-term sustainability of the UK’s public finances and on the effect of economic developments and fiscal policy on the UK’s medium-term outlook.

{kind=link}