MarianVejcik

Inflation on the cusp of hitting the 2% target

The December personal income and spending report contains a number of interesting stories, but the obvious headline is that the US economy has been able to return inflation towards the target in an environment of vigorous consumer spending growth. Something that is even more remarkable after a significant supply shock and during a period of ultra-low unemployment.

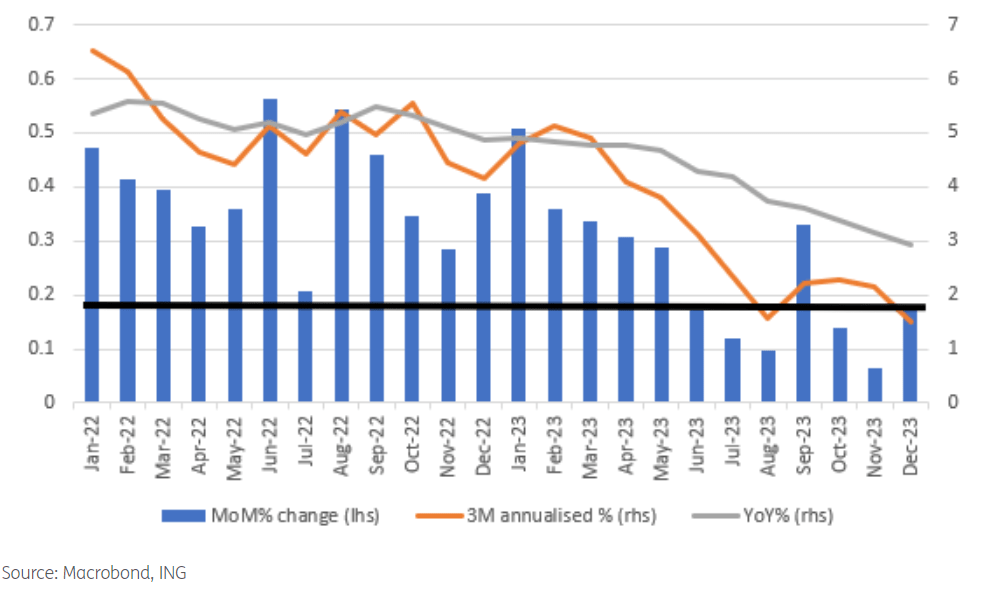

There were no real surprises on the inflation front with the core personal consumer expenditure deflator (the Fed’s favoured measure of inflation) coming in at 0.2% month-on-month, but the year-on-year rate is 2.9% rather than 3% – yesterday’s GDP report basically told us this. Importantly, the MoM change was 0.17% MoM, which is exactly what we need to consistently achieve to get inflation to 2% YoY over time. This is the sixth month in the last seven that we have been at or below this key threshold and this should give the Fed real confidence that the job is done on inflation and policy rates do not need to be so restrictive. In fact, the 3-month annualised rate is now just 1.5%, suggesting we run the risk of undershooting later this year!

Personal consumer expenditure deflator MoM, 3M annualised % YoY%

Strong spending still driven by legacy savings

For activity to be so strong in this benign inflation environment is astonishing. Consumer spending rose 0.7% MoM versus the 0.5% consensus with an upward revision to November from 0.2% to 0.4% growth. Unfortunately, it isn’t being fuelled by incomes, which rose only 0.3% MoM nominally while the true measure of spending power – real household disposable income – which is income after tax and adjusted for inflation, rose just 0.1% MoM. For real (inflation-adjusted spending) to be up 0.5% MoM, it highlights how important the run-down of savings and robust credit card spending continues to be in keeping overall consumption so strong.

Real household disposable incomes remain lacklustre

First quarter GDP growth set to remain robust, leaving May the more likely start point for rate cuts

This is not sustainable over the long term, but the consumer refuses to lie down. Given this momentum, first quarter GDP looks increasingly likely to be in the 1.5-2% range, meaning the consensus of 0.6% growth needs to be revised up – even if there is zero consumer spending growth in January, February and March, the QoQ annualised rate of consumer spending growth will be 2.1% in the first quarter! This must make a March rate cut look less likely, and we continue to favour May being the timing for the first move.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

{kind=link}