With US inflation cooling for the second consecutive month, market bulls seem to be facing another rebounding tailwind amid a slowdown from the US Federal Reserve. While a Christmas rally may be still on the horizon, there are both economic risks and policy risks coming into the new year.

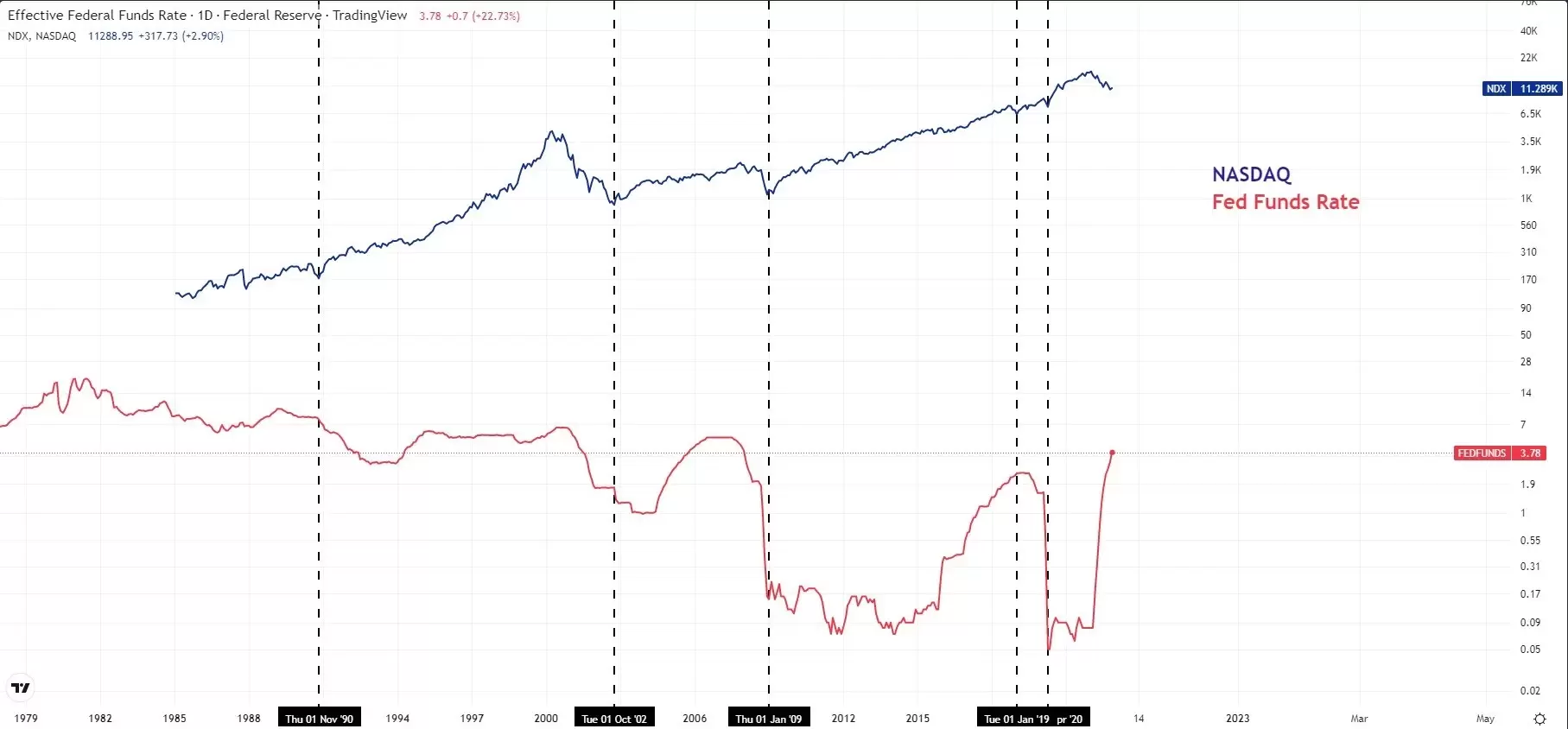

With no Fed pivot, Nasdaq may have further to fall

Though the Fed is dialling back the pace on rate hikes, the rate-hike cycle will not end until inflation goes back to its target level of 2%. November’s headline US consumer price index (CPI) printed at 7%, which is still well above target. The Fed swap rate is now projecting a terminal rate of between 4.75% to 5% by March 2023. The higher-for-longer rates may continue to pressure the tech-heavy Nasdaq index, at least in the first three months of the new year.

The above chart indicates that the Nasdaq only bottomed out during a rate-cut cycle following an economic recession. A similar equity market cycle can be seen during the dot-com bubble in 2000, the global financial crisis of 2008, and the Covid-19 pandemic in 2020, when the Nasdaq fell 80%, 50%, and 30% respectively.

Since the all-time high in November 2021, the index fell about 38% when it touched the year low in mid-October 2022. However, the Fed remains far away from a pause or rate cut, which may leave more room for the index to fall. Plus, the deeply inverted US bond yields repeatedly warn of an unavoidable upcoming economic recession.

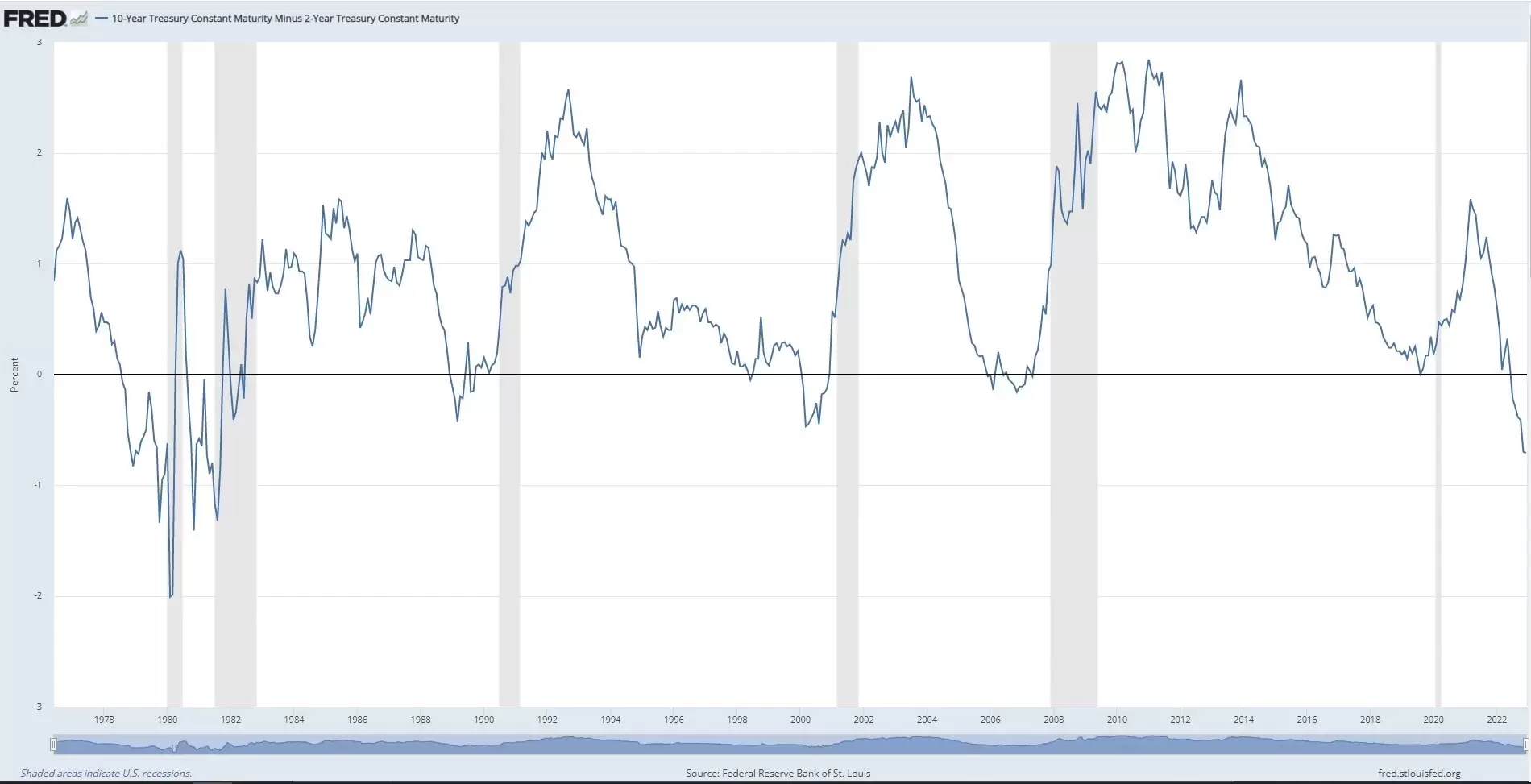

Spread yield widens

The spread between US two-year and 10-year bond yields widened to its greatest level since 1982, and there are no signs of an improvement. This indicates that the economic outlook could become gloomier, and with rates likely to stay at a high level, may lead the US economy to enter a stagflation era.

Usually, tech stocks don’t perform well during a period of stagflation. Instead, cash and defensive stocks do better during this economic cycle. It will all depend on how hard and how long the economic recession lasts. A hard recession may promote a swift Fed policy turnaround and lead the Nasdaq to reach its bottom sooner. However, a mild recession may not benefit growth stocks, as a slow Fed pivot could cause a prolonged stagflation cycle.

USD may have reached its peak

In the wake of a slowdown in US economic growth, the US dollar may have reached its peak against the other G10 currencies. An observation of the correlation between the dollar index and US bond yields is that the US dollar is positively correlated with long-dated US bond yields, but not its short-dated peers. Another interpretation is that the dollar’s trend follows the economic trajectory, but not the Fed funds rate.

The above chart illustrates that the dollar index traces the movement in 10-year bond yields and the dollar falls during an economic recession, but not necessarily during a Fed rate-cut cycle. Or, in short, USD falls when there is a GDP downturn. After two consecutive negative quarterly GDP growth readings, the US economy rebounded in the third quarter on a 2.9% annualised base. However, signs of slowing are mounting, as both US manufacturing and manufacturing PMIs contracted in November, and the data are expected to deteriorate further due to hefty inflation and rising rates.

The above chart shows that the US ISM manufacturing PMI has fallen to its lowest level in the last two recession periods, in 2008 and 2020. A downturn in GDP usually follows when PMI data declines to such a level. Hence, we can almost conclude that the US dollar may have reached a peak, as US GDP may start declining in the first quarter of 2023, if not in the final quarter of this year.

Disclaimer: CMC Markets is an execution-only service provider. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.

{kind=link}