LONDON, May 12 (Reuters) – Britain’s economy grew sluggishly in early 2023, better than the shallow recession once expected, but an unexpectedly sharp drop in output in March underscored how fragile its recovery remains.

Gross domestic product (GDP) edged up 0.1% in the first three months of the year, official data showed on Friday, the same tepid pace as in the final quarter of 2022 and in line with economists’ forecast in a Reuters poll.

Output was 0.2% higher than a year earlier, the Office for National Statistics said.

But GDP in March alone dropped 0.3%, compared with poll forecasts for it to hold steady. While industrial output and construction grew, the much larger services sector dropped 0.4%, reflecting weak car sales and retail, hurt by unusually rainy weather and high inflation.

Widespread industrial action also weighed on economic activity in the first quarter, the statistics office said.

“With the key services side of the economy continuing to slow in the face of higher borrowing costs and rising prices, it still feels like we’re walking through treacle,” said Tom Stevenson, personal investing director at fund manager Fidelity International.

Britain’s inflation rate topped 10% in March – double the level in the United States and higher than the euro zone’s too – and on Thursday the Bank of England raised its main interest rate to 4.5%, the highest since 2008.

The jump in inflation largely reflects the ongoing impact of a surge in the cost of natural gas imports and foodstuffs last year after Russia’s invasion of Ukraine, which the BoE says has made Britain poorer.

The central bank forecasts the economy will grow 0.25% in 2023 as a whole – a weak expansion though an upgrade on its prediction earlier this year of a 0.5% contraction.

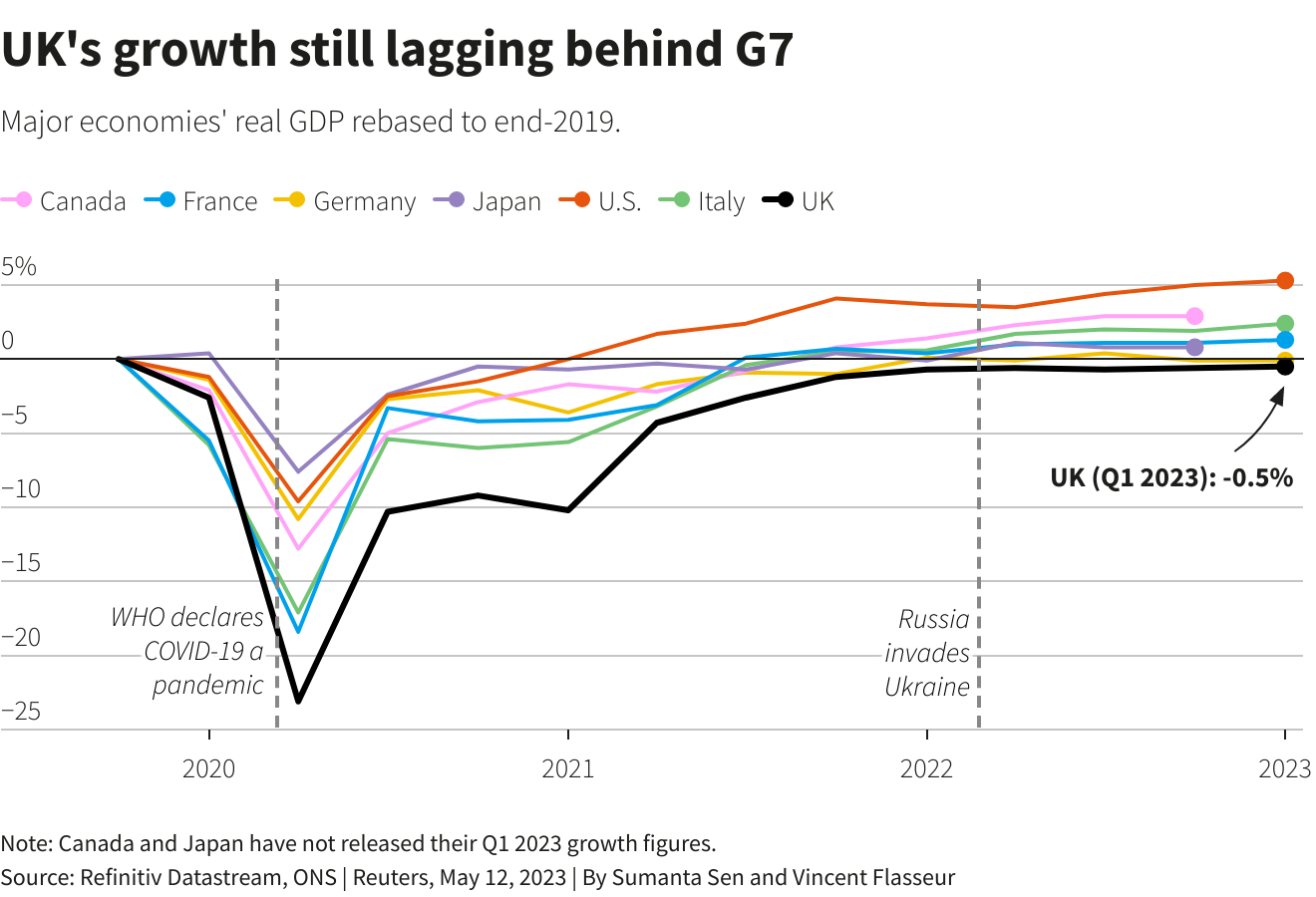

British GDP expanded at the same pace as the euro zone’s in the first quarter, but it has underperformed since the start of the COVID-19 pandemic – partly due to post-Brexit trade barriers and restrictions on hiring low-paid migrant workers.

Output in the first quarter of 2023 was 0.5% lower than in the fourth quarter of 2019, before the coronavirus pandemic – a weaker rebound than in any other big advanced economy.

“MANAGED DECLINE”?

Finance minister Jeremy Hunt said Friday’s data showed “growth is picking up much faster than anyone thought possible” but the government needed to “stay focused on competitive taxes, labour supply and productivity”.

Hunt’s counterpart in the opposition Labour Party, Rachel Reeves, said Prime Minister Rishi Sunak’s Conservative government was presiding over “managed decline”.

Sunak is likely to call a national election next year, ahead of a January 2025 deadline.

Economic output in March was only 0.1% higher than in February 2020, the last full pre-pandemic month.

“While recession is probably no longer on the cards, vulnerabilities resulting from higher borrowing costs and tighter credit are likely to dampen business and household activity this year,” KPMG economist Yael Selfin said.

Second-quarter growth is likely to be slowed by the effect of an extra public holiday in May for King Charles’ coronation.

Business investment in the first quarter of 2023 was 3.2% higher than a year earlier, its smallest annual increase since late 2021, while the 0.2% rise in household consumption was the slowest in two years.

The data showed Britain recorded a 31.5 billion-pound ($39.8 billion) trade deficit with the European Union in goods excluding precious metals in the first quarter, close to the record 33.2 billion-pound gap in the three months to January.

($1 = 0.7923 pounds)

Reporting by William James

Our Standards: The Thomson Reuters Trust Principles.

{kind=link}