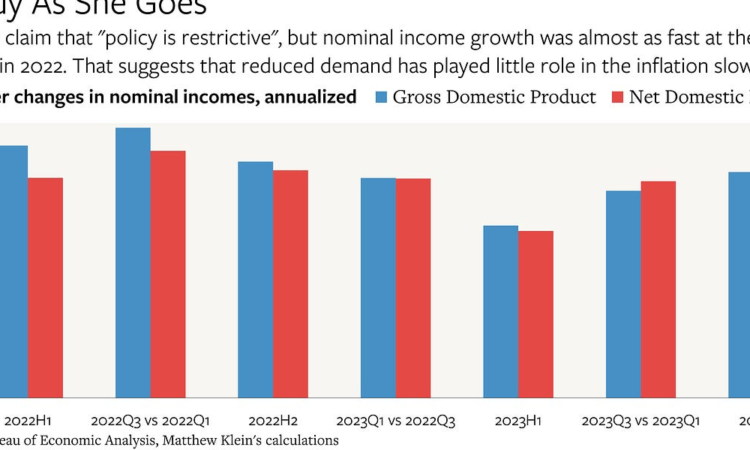

Traders are still betting that short-term interest rates will fall sharply in the next few years because they believe—along with Federal Reserve officials and many other analysts—that the post-pandemic economy will more or less resemble the world of 2019.

While that may prove correct, the data so far continue to suggest that we remain in a period of structurally faster growth more akin to the second half of the 1990s, or perhaps the second half of the 1960s. Crucially, the welcome (but temporary?) slowdown in inflation has not been matched any commensurate slowdown in nominal income growth, but instead has manifested as surging productivity and real output. The mix of interest rates necessary to generate the right balance of financial conditions under these circumstances may therefore be higher than what is currently being priced in.

I still chuckle at this Bloomberg News headline from October 17, 2022:

Forecast for US Recession Within Year Hits 100% in Blow to Biden

This was not just any forecast, but the official projection of Bloomberg’s internal economics team, which is staffed by veterans of the Federal Reserve and other respectable institutions:

A US recession is effectively certain in the next 12 months in new Bloomberg Economics model projections, a blow to President Joe Biden’s economic messaging ahead of the November midterms.

The latest recession probability models by Bloomberg economists Anna Wong and Eliza Winger forecast a higher recession probability across all timeframes, with the 12-month estimate of a downturn by October 2023 hitting 100%.

Reality turned out differently. Not only did the U.S. avoid a downturn in 2023, we now know that the inflation-adjusted value of goods and services produced in the U.S. grew more than 3%, vs. 0.7% in 2022. Growth would have looked even better if the UAW, SAG-AFTRA, and WGA strikes had not temporarily derailed production in motor vehicles and media. While it may change, the Federal Reserve Bank of Atlanta’s current guesstimate is that the U.S. economy will keep growing at a 3% yearly pace at least through 2024Q1—and that could be conservative given the recent boom in homebuilding.

Bloomberg may have been the most egregious, but it was far from alone getting the forecast wrong. At the end of 2022, Fed officials believed that the U.S. economy would only grow 0.5% in 2023 “under appropriate monetary policy”. The experts polled in the Survey of Professional Forecasters thought that output would rise about 0.9% over the course of 2023.

Why was everyone so pessimistic? By definition, the unwelcome price increases of 2021-2022 reflected mismatches between how much money and credit people were spending on goods and services relative to businesses’ ability to meet demand. There were three basic ways to resolve these mismatches:

-

Consumers could shift their spending on the mix of goods and services they bought in ways that relieved stresses on the most strained sectors

-

Consumers could spend less overall, buying fewer goods and services and increasing idle capacity throughout the economy

-

Businesses could overcome whatever problems were holding back production relative to demand and ramp up output

The mistake was believing that the middle option was the only one that would be viable. That belief led many to conclude that someone would have to force Americans to slow their spending—which would necessarily flow through to businesses’ sales, profits, investment, hiring, wages, etc.—until there was no longer any pressure to raise prices. The Fed duly tightened financial conditions throughout much of 2022, which ended up hitting consumer spending, business investment, and, especially, the housing market.

But then things reversed.

{kind=link}