In the blink of an eye, the global economy’s most pressing problems have surprisingly gone away.

X

In October, as the S&P 500 was plumbing bear-market lows, rapid-fire Fed rate hikes and a soaring dollar stoked fears the sickly global economy would crash. Then the unexpected happened — again and again.

Now the all-but-certain 2023 global recession has been called off, and the rest of the world should help cushion the landing for the U.S. economy.

So what does this revamped outlook for the global economy mean for investors? A soft U.S. landing should limit the downside for corporate earnings and the S&P 500. The Federal Reserve shows no inclination yet to relax its inflation fight, but cooling wage growth suggests they may not have to inflict as much pain.

Investors need to stay flexible and likely cast a wider net. If there’s no recession, inflation may not subside as quickly. Long-term Treasury yields, instead of collapsing in an economic downturn, might act as a headwind to growth stock valuations. Yet international stocks, long out of favor, might extend their recent run as growth recovers overseas.

China Makes ‘Mother Of All U-Turns’

China’s economy, until recently locked down, is now off to the races. President Xi Jinping took the “mother of all U-turns,” as Jefferies strategist Christopher Wood put it, ditching his zero-Covid policy late last year and hitting the fiscal accelerator. Europe’s economy, at risk of going into a deep freeze this winter without Russian fuel, is instead heating up after natural gas prices unexpectedly plunged.

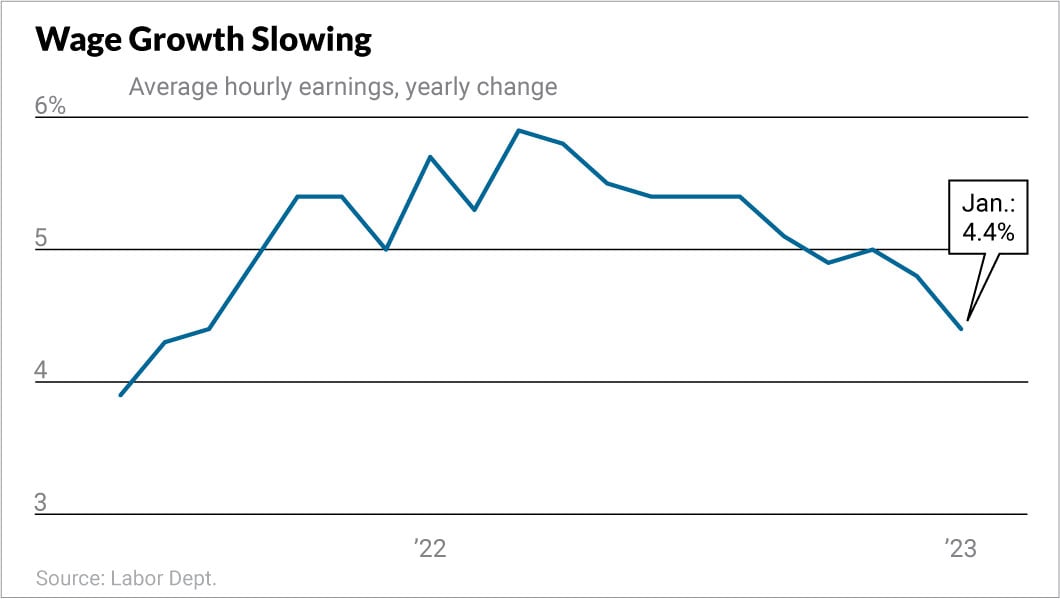

In the U.S., Fed officials had been dead-set on driving up unemployment, risking recession, to cool off the hot wage growth they feared could make high inflation the new normal. Despite their best efforts — and 425 basis points in rate hikes — unemployment has kept sliding to the lowest point since 1969. But despite strong job gains, wage growth has cooled to a level close to the Fed’s comfort zone.

The U.S. economy still faces a slog in 2023 as the Fed hikes rates further to depress growth. But the jobless rate shouldn’t have to rise as much as feared before the Fed pivots.

Moderating wage growth means that Fed policymakers “don’t need to kill the economy,” wrote Ian Shepherdson, chief economist at Pantheon Macroeconomics.

How Long Will Fed Rate Hikes Continue?

After January’s surprisingly strong jobs report and retail sales data, Fed officials are on alert for a reacceleration in growth that could keep inflation elevated. That sealed the deal for quarter-point rate hikes at the next two Fed meetings in March and May and put the recent S&P 500 rally on pause.

Markets are now pricing in better-than-even odds of one additional rate hike in June or July. But the apparent burst of economic momentum to start 2023 isn’t likely to last.

The nation’s savings rate, after falling to a rock-bottom 2.4% of income, began rising at the end of last year, taking some of the wind out of household spending. Despite January’s 3% retail sales jump, which was helped by an 8.7% Social Security cost-of-living increase, sales over the three months through January slipped vs. the prior three months.

Global Economy Vs. U.S. Economy

Historically warm weather likely boosted activity last month, including an estimated 125,000 lift to payrolls, says the San Francisco Fed. A University of California strike resolution added back 48,000 postgrad teaching assistants and researchers. Soft seasonal retail and temp hiring in Q4 reduced the need for post-holiday layoffs, which gave the appearance of stronger hiring on a seasonally adjusted basis.

Comparisons also were probably skewed because the two biggest Covid waves peaked at the start of the prior two years. In January 2022, 6 million people said they were sidelined or had hours cut amid the omicron surge, doubling from the prior month.

The clearest indication that the labor market isn’t as overheated as it appears is the continued moderation in wage growth. The past two employment reports show the 12-month rate of average hourly wage growth slowed to 4.4% from 5%, even as the unemployment rate fell to 3.4% from 3.6%. That combination “is even better than Goldilocks,” wrote Jefferies Chief Financial Economist Aneta Markowska. Taken at face value, it suggests “a utopian scenario” in which stronger growth produces lower inflation, she wrote.

While that’s far-fetched, the reality is still pretty great: Wage growth has been cooling without significant labor market weakness. Average hourly earnings growth has fallen 1.5 percentage points since peaking at 5.9% last March. The Employment Cost Index, the Fed’s favorite read on wage trends, shows compensation for private-sector workers rose just 0.9% in Q4, excluding incentive-paid occupations with volatile sales commissions. That 3.6% annual rate is just a hair above the 3.5% wage growth that Fed chief Jerome Powell says is consistent with the Fed’s 2% inflation target.

Changing Tones On Fed Policy

Tamer wage growth, despite solid hiring, explains Fed chief Powell’s optimistic tone during his Feb. 1 news conference, which sent the S&P 500 surging to a five-month high. Powell notably declined to rule out the possibility of rate cuts later this year if inflation falls faster than expected.

Fed talk quickly turned less-hopeful after January’s jobs report. A parade of officials have raised the possibility of additional rate hikes to cool the labor market.

Tuesday’s CPI report, which hit pause on the S&P 500’s latest push higher, won’t help. Services inflation shows no letup, while three months of core-goods price deflation came to an end as prices firmed in categories like apparel and household furnishings.

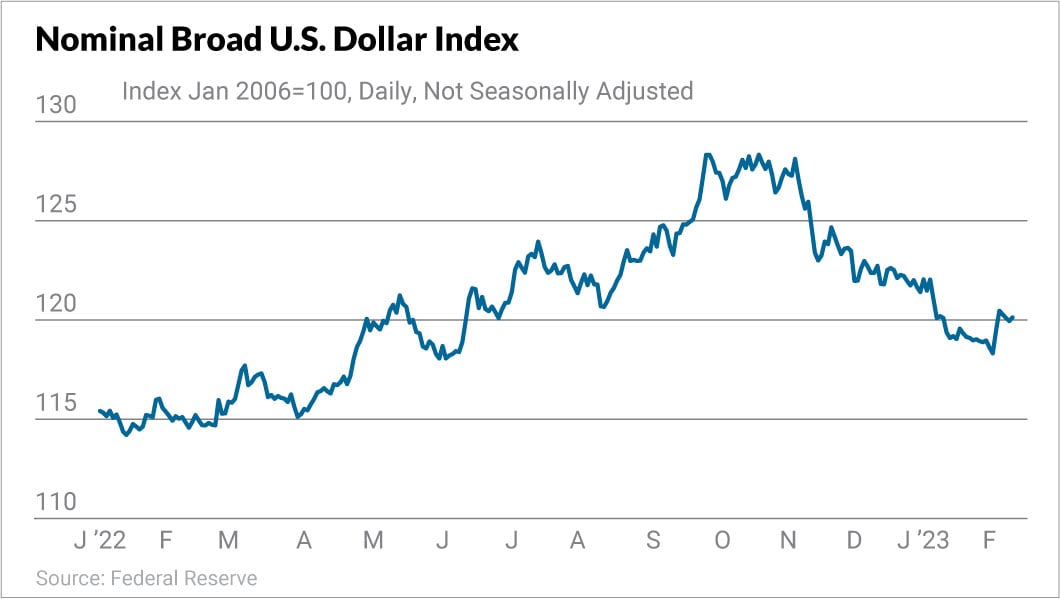

It’s no coincidence that the current stock market rally peaked Feb. 2, a day after the latest Fed meeting and Powell’s soothing words and just before the January jobs report. The dollar and Treasury yields also have rebounded from early February. However, the S&P 500 and other major stock indexes haven’t given up much ground.

Join IBD experts as they analyze actionable stocks in the market rally on IBD Live

No Need For Unemployment Spike?

Yet despite the reversion to a hawkish tone, softer wage growth has changed the Fed’s destination in its battle against inflation.

The latest Fed projections from December showed that policymakers thought the unemployment rate would have to hit at least 4.6% before they approached an exit ramp from tight monetary policy. And the exit ramp was expected to be long, with unemployment holding near that level for two full years as inflation only gradually receded toward the 2% target.

Behind those projections was a view that the labor market had fundamentally changed. Before Covid, the Fed struggled to boost inflation even to 2%, despite unemployment falling as low as 3.5%.

Then the pandemic and its side effects dealt a shock to the labor market. While government stimulus and inflated unemployment benefits went away in 2021 and Covid disruptions faded, the shock seemed to persist. In November, Powell highlighted 2 million excess retirements during the pandemic, helped along by the wealth effect from the rise in the S&P 500 and soaring home prices. Meanwhile, the housing shortage only complicated the challenge of finding scarce workers in hot real estate markets.

Those factors, economists figured, had raised the noninflationary rate of unemployment to around 5%. That meant that inflation couldn’t be whipped without a recession.

Current Job Market

But recent wage data and corporate earnings calls suggest that the labor market has begun to function more smoothly.

Waste Management (WM) CEO James Fish noted he sees “improvements in our labor cost as inflationary wage pressures are easing (and) turnover trends are improving.” Chipotle (CMG) CEO Brian Niccol said December was “one of our best months in the past two years for both hourly and salary turnover rates.”

The labor situation began improving in Q3, Northrop Grumman (NOC) CEO Kathy Warden told analysts. “Our hiring had improved. Our retention had dramatically improved, and we saw that trend continue in the fourth quarter.”

By December, the share of private-sector workers quitting their jobs had reversed more than half its rise vs. pre-Covid levels. Julia Coronado, president of MacroPolicy Perspectives, noted on Twitter that the household survey component of January’s jobs report revealed a nearly 1 million population boost, mostly due to net international migration.

The newly discovered population, she wrote, “comes in with a hot (labor force) participation rate of 91.3%,” vs. 62.4% for the nation as a whole. Coronado expects more of the same in 2023, which should contribute to noninflationary growth.

Evidence that the noninflationary rate of unemployment is “still only 3.5%-4% is becoming quite compelling,” said Pantheon’s Shepherdson.

The upshot: Instead of a Fed pivot after unemployment rises to 4.6%, it could happen when the jobless rate reaches 4%.

But until the job market is clearly weakening and disinflation broadens out to services such as health care, haircuts and hospitality, the Fed will err on the side of keeping monetary policy too tight.

Global Economy Boost To Inflation?

Meanwhile, the sudden upturn in global economic growth is supporting commodities prices, adding to the risk that high inflation may stick around.

In a Feb. 7 Q&A, Powell highlighted the “risky world out there” as among his concerns, noting that the war in Ukraine and reopening of China “can affect our economy and the path of inflation.”

One wild card will be whether the end of three years of rolling Covid lockdowns and the slowest growth in a half-century revives the confidence of China’s middle class and reinflates the property bubble, wrote Jefferies’ Wood. The risks in China “are massively to the upside,” he said.

Many economists, however, expect China’s recovery to be underwhelming. As in the U.S., Chinese households have stored up extra savings during the pandemic. But whereas U.S. consumption benefited from stimulus checks and a boost in housing and stock market wealth, Chinese households spent less and saw housing wealth deflate.

Pent-up demand in China will primarily lift spending on services like health care, education and transportation that are depressed vs. pre-Covid levels, wrote UniCredit economist Edoardo Campanella. These categories of spending “are intrinsically domestic and are therefore unlikely to benefit the global economy in a substantial way.”

China, Emerging Markets To Drive Global Economic Growth

Yet even the IMF’s base case has China combining with India to drive half of global GDP growth. The U.S. and Europe will only account for one-tenth of global growth combined, the IMF says. The European Central Bank, like the Fed, is still aggressively tightening to rein in inflation.

Meanwhile, other emerging market economies are expected to pick up speed, the IMF says. A weaker dollar lowers the cost of dollar-priced commodities such as oil and reduces the cost of servicing dollar-based debt. The dollar has tumbled in recent months, though it’s bounced a little in February.

What Outlook For Global Economy Means For Investors

The juxtaposition of better economic growth overseas and a Fed determined to step on growth at home presents an unusual backdrop for investors.

Ed Yardeni, chief investment strategist at Yardeni Research, who has long advised investors to “stay home,” has tilted to a “go global” stance through the first half of 2023.

“The valuation multiples are significantly lower overseas,” he told IBD, highlighting “opportunities in banks and energy in Europe.”

Still, he expects the U.S. to avoid recession, and sees some opportunities at home. “A lot of money is pouring into infrastructure and onshoring, and that benefits industrials,” Yardeni said. “Energy still looks fine and financials are in great shape.”

While Wood sees upside risk in China, he sees U.S. risks as being “clearly to the downside” as the Fed keeps tightening.

“Slowing inflation into a slowing economy also means declining nominal GDP growth,” Wood wrote. That means U.S. stocks face a risk of earnings downgrades, he says.

Last month, Wood’s Greed & Fear newsletter unveiled a global long-only portfolio of 23 stocks that reflects global economic trends. The portfolio is overweight China, including e-commerce plays Alibaba (BABA) and JD.com (JD), as well as India and European banks. It also makes plays on rising commodities prices, including U.S.-based copper giant Freeport-McMoRan (FCX) and oilfield services leader SLB (SLB). Dutch chip-equipment maker ASML (ASML) is a play on the chipmaking expansion as the U.S. decouples from China.

Going global has worked pretty well. London’s FTSE 100 index and the CAC 40 in Paris have hit record highs in the past week. Hong Kong’s Hang Seng Index, after crashing to a 13-year-low in October, has rebounded more than 40%.

Time The Market With IBD’s ETF Market Strategy

Global Economy And Growth Stocks

Plays on global economic growth have a big presence in the flagship IBD 50 list of top growth stocks and the IBD Leaderboard portfolio. The latter includes travel-related stock Airbnb (ABNB) and the U.S. Global Jets ETF (JETS), as well as MercadoLibre (MELI), Latin America’s largest e-commerce company. The KraneWeb CSI China Internet ETF (KWEB) is on the Leaderboard Watchlist.

Yet U.S. growth stocks also began the year on a tear. The S&P 500 information technology sector’s 15.6% gain year to date has nearly doubled the 8% rise for the blue chip index. Lately, more speculative plays are catching fire, including Bitcoin and Ethereum.

Federal Reserve Has Upper Hand

Strong jobs data, firming inflation and surging stock prices may make it seem like the Fed is losing control.

In reality, the Fed has just gained the upper hand. Bond traders had been pricing in fewer hikes and a quick pivot to rate-cutting. Now they are suddenly betting that the Fed may raise rates even higher than its own projections show. That’s sent the 2-year Treasury yield surging about 60 basis points over the past two weeks to 4.63%. The six-month T-bill has topped 5% for the first time since 2007. Meanwhile, the 10-year yield, key for pricing auto loans, has jumped a half point. The 30-year mortgage rate, after falling to near 6%, surged 70 basis points over the past month.

Higher borrowing costs for consumers and the small businesses key to job growth will deliver the slowdown policymakers want. Yet stock investors are still fighting the Fed and that might continue for a little while. Financial conditions remain easy, partly because the Treasury has stopped issuing new debt ahead of a debt-ceiling showdown with the GOP.

But the economy and S&P 500 are likely approaching an inflection point. After a strong start to 2023, the near-term outlook for stocks could be difficult. However, a significant economic slowdown now should smooth the downward path for inflation and a soft landing that creates the conditions for a sustainable stock market rally.

Be sure to read IBD’s The Big Picture column every day to stay in sync with the market direction and what it means for your trading decisions.

YOU MAY ALSO LIKE:

Why This IBD Tool Simplifies The Search For Top Stocks

Want To Get Quick Profits And Avoid Big Losses? Try SwingTrader

Find The Best Growth Stocks To Buy And Watch

IBD Digital: Unlock IBD’s Premium Stock Lists, Tools And Analysis Today

Rally Still Healthy, But Be Patient; Lithium Play Soars On Tesla Buzz

{kind=link}