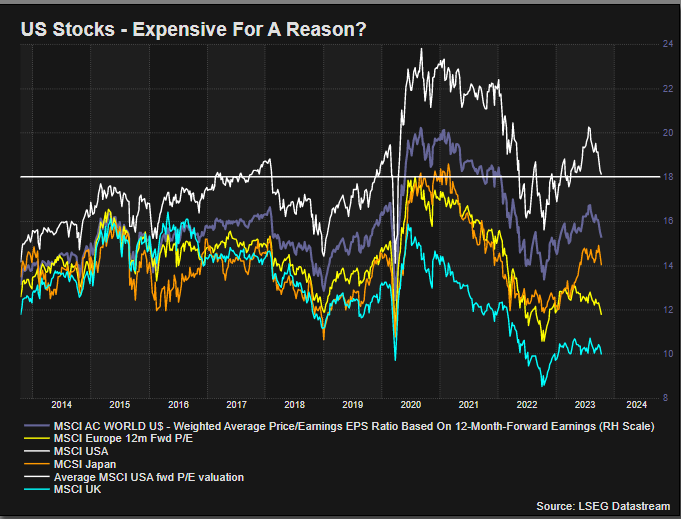

LONDON, Oct 18 (Reuters) – With the U.S. economy roaring at a faster pace than China and global politics increasingly hard to fathom, there’s a feeling the best bet in town is to stick with U.S. stocks regardless of relative valuations.

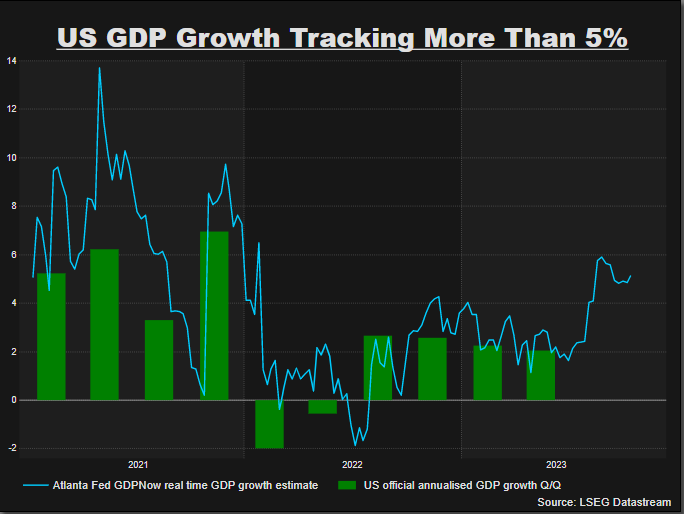

After another forecast-busting U.S. retail and industrial readings for last month, the Atlanta Federal Reserve’s real-time economic growth estimate hit an annualised 5.4%, more than a point higher than China’s equivalent.

And all against a murkier international backdrop.

The Gaza crisis throws yet another geopolitical imponderable into an already crowded and confusing picture globally.

Already, the 18-month Russia/Ukraine war smoulders amid sweeping sanctions, energy and food disruptions, and supply chain re-sets. China’s alliance with Moscow, tit-for-tat investment curbs with Washington and its claim to Taiwan all provide a polarised and unpredictable menu for cross-border savers.

The list of risks to your money in some of the world’s biggest economies has spiralled amid a withering array of gloomy scenarios, many not contemplated for over 30 years.

And so it’s fast becoming a world where relative valuations may matter less than a purring home economy, steady income and deep and liquid markets – relatively free from opaque political sideswipes, international sanctions or unmanageable exchange rate risk.

Mirroring so-called deglobalization trends of reshoring, secure energy and a host of repatriated industrial capacities from chip making to autos, ‘home bias’ in investing may be back too.

And for the United States, that’s an awful lot of money to be tempted back home to what’s already the biggest and most easily traded markets for stocks in the world – with both cash and long-term bond holdings now yielding more than 5% to boot.

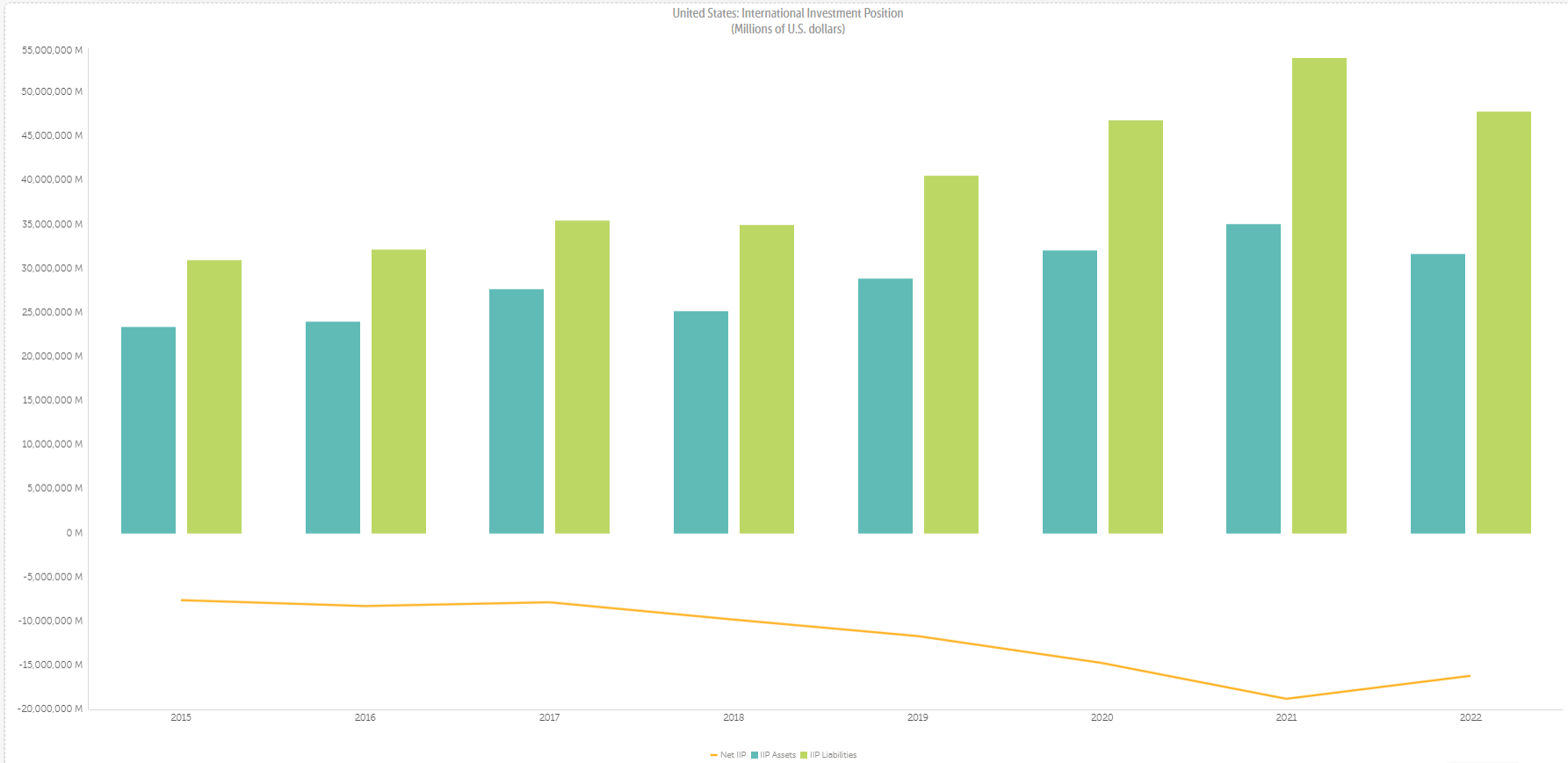

Based on International Monetary Fund data on comparative international investment positions through the early part of this year, U.S. portfolio investment overseas – equity, fund shares and debt securities – stood at more than $14.5 trillion.

While that’s still more than a trillion dollars higher than pre-pandemic levels in 2019, it’s retreated by almost $2 trillion from the peaks of 2021, just before the Russian invasion of Ukraine in March of last year.

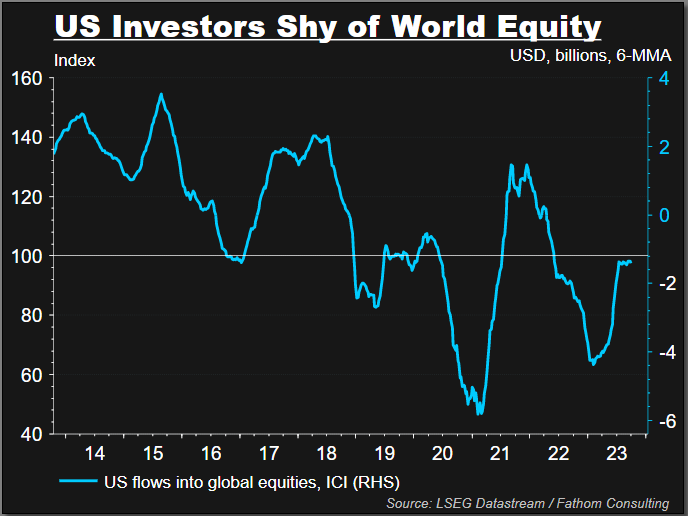

A more granular look at U.S. long-term investors’ purchases of overseas equities by ICI shows funds have been sellers of global equities since May 2022 on a rolling six-month basis.

While the scale of those sales has lessened since February this year, a reluctance to return outright seems clear as geopolitics deteriorates, the U.S. economy dodges recession and re-accelerates, and a buoyant dollar both feeds and feeds off U.S. investors temptation to stay home.

But it’s not just that scared U.S. money is going home.

SHRINKING UNIVERSE

For Swiss asset manager Julius Baer’s chief investment officer Yves Bonzon, the pool of investable markets outside the U.S. is simply getting smaller due to seismic and structural shifts in global relations.

“The investment universe for western capital has shrunk with the Ukraine invasion and return of cross-border political risk in a multipolar world,” said Bonzon. “The only option to deploy capital in size is the United States.”

“If you reduce your playground to democracies, money will flow to the U.S. – not the UK, or Switzerland or Germany – and you can see the outperformance of U.S. assets is evidence of this,” he added. “Short U.S. assets or short the dollar is not a good trade in this scenario.”

What’s more, Bonzon reckons inflation is likely to settle as close to 3% as to 2% once the world’s central banks are finished their severe tightening cycle, meaning the secular bull market in bonds is over even if more attractive income allows them to be a good portfolio hedge again.

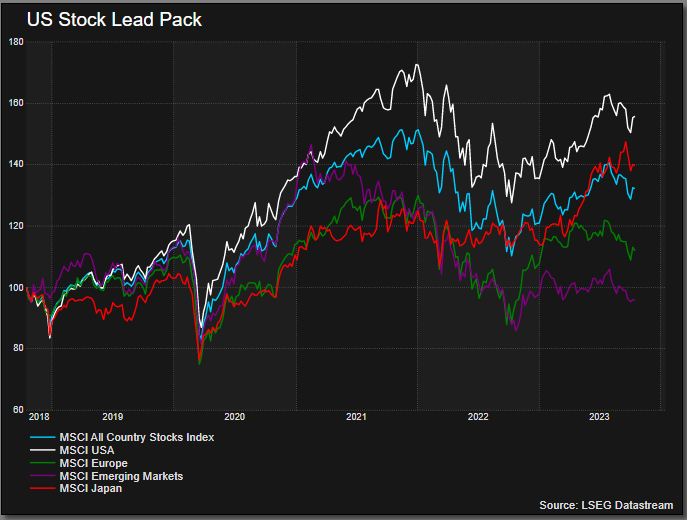

That overview is a world where investors should favour real assets over nominal claims and focus on ‘store of value’ equity markets, he thinks. And the latter means Wall St big caps and the S&P 500 continue to be the strategic market of choice – underscored by their proven ‘cash returning’ properties and aggregate insulation from higher interest rates this year.

If other overseas asset managers or sovereign wealth funds were to think likewise, then the some $25 trillion of foreign holdings of U.S. portfolio assets – some $10 trillion higher than U.S. asset holdings overseas – may only get bigger.

But there are questions and problems as always.

The upshot could be an ever wider U.S. deficit on its net international investment position – potentially lifting the dollar as that inflates, but leaving it vulnerable to the yawning gap and foreign investor sentiment down the road.

And while international politics looks fractious right now, the next 12 months will once again test the resilience of the U.S. democratic system and may challenge attractiveness of U.S. assets in the process.

Even the haven of home seems far from straightforward.

The opinions expressed here are those of the author, a columnist for Reuters

Our Standards: The Thomson Reuters Trust Principles.

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.